A framework for Credit Portfolio Management - The secret sauce for investing in corporate bonds

A framework for Credit Portfolio Management - The secret sauce for investing in corporate bonds

Part 1 "The framework" and "The Strategic Asset Allocation"

Good morning to all. As promised to someone I’ll start to share some tools that I use for investing in corporate bonds and credits. I’ll focus on european corporate bonds market because it was my core business for years and I have a better knowledge on it.

Before to start remember to share this piece if you like it and to subcribe to the newsletter (scheduled mail are on Friday with the usual recap of what happened on the week but I write some bonus-tracks regarding investment process too). So let’s go!

The investable universe is very large. We have:

a lot of sectors (banks, insurance, TMT, Energy, etc)

different subordination classes (AT1, hybrids, T2, senior, etc)

different rating classes (IG vs HY, AAA vs BBB, BBB vs BB, etc)

different issuers for each sector

and at the end of the day we have also the problem of term curve (for each name we have a curve of bonds with different sensitivity to duration

This creates a sort of “Rubik Cube” that could which can scare a lot of us so it’s important to have a framework to deal with this. The approaches could be different and can be divided into:

Top-Down: start from the macro picture and go down;

Bottom-Up: start from the single sectors and names and combine all it in a single portfolio

Your choice depends on how many peoples are dedicated to the process. Starting to work in a small investing boutique I dedicated myself to top-down approach (being in charge of idea generation, portfolio management and execution) but also the other method is valid.

Before starting I reccomend you the book I read a long time ago and that I used as a base for constructing my framework, with the add of other piece of research coming from investment banks: “Investing in Corporate Bonds and Credit Risk - Frank Hagenstein, Alexander Mertz and Jan Seifert”

The Framework: The investment process

As said before the choise to manage a credit portfolio can be differents (there are different fusion between the two styles we talked above). I choosed (I was force being alone and being focused also on government bonds and macro products) to use a pure top-down approach (from this my name “Credit from Macro to Micro”) consisting of three basic steps:

The Strategic Asset Allocation: in this part (usually I did it every 3/4 months) there is the determination of the beta in your portfolio, basically how much risk you want to have. Can be thinked about the weight of corporate bonds vs a benchmark (or vs cash) or the credit duration too.

The Tactial Asset Allocation: in this part of the process (usually each month) there is the selection of the different spread classes (senior vs subordinated, rating based HY vs IG, or sector choice). This is function always of the past point (if you are bearish on credit usually you prefer senior to subordinated debt, IG to HY and defensive sectors to cyclical one). Always here there is the choise of credit curve positioning.

The Stock/Bond Picking: it’s done continuously day by day. It’s about the choice of the issuer (doing a macro to micro approach once you chooce the sectors, you have to investigate inside that) and of the issues (wich bond exactly). This part require to get dirty your hands about fundamental analysis and credit research but also on relative value.

I’ll go inside each point better. In this piece I’ll talk about Strategic Asset allocation while the others two point will go in other two different pieces.

The Strategic Asset Allocation

Most of the tool I use are based on scorecard. I love scorecard, they give me a sense of satisfaction but the most important think to say before going deep is that it’s always and only a tool. I don’t use it systematically. There is not a “secret sauce” on it. A scorecard is usefull to have a starting point always similar and to force you to analyze regularly some points but the driver could change every time (and they did).

Here we go. There is a part of fundamentals (macroeconomic and micro-fundamentals), a technicals one, a sentiment part and a valuation one (where I assign a higher weight than other part given the mean-reverting nature of spreads usually, trying to capture the theory of “selling when you can and not when you need”, but also the “buy when the is blood in the street”). For a lot of indicator that I use I calculate a 5Y z-score to normalize the input in one indicator that goes from -2 (very negative) to +2 (very postive).

Now we will analyze each point better.

1 Macro

In this part I track some macro indicators that I think could be important to look and that could drive the spreads in the future. I don’t go too much in the details but there is a part of growth indicators (ZEW, IFO, etc) and a part of policy (here I use ECB and FED expectations of rates, but also the China Credit impulse that it’s a great leading indicator of global growth). There is also a proxy for global M1. You can see there was a spike in the data in 2020 after the covid stimulus and now is returning back. As I said it’s only a starting point but you can see (in the blue column called Trend 5Y) that indicators are almost negative, it’s not a surprise that growth is weakening, and central bank are in hawkish environment. Here the red flag of the average score for this part that is -1.

As I said it’s only a starting poin, you need to go deeper in each indicator and maybe looking at others ones. I am fan of looking liquidity (a sum of central banks and banks credit creation). It’s liquidity the most important fundamental that drives all. Macro fundamentals and liquidity are well related.

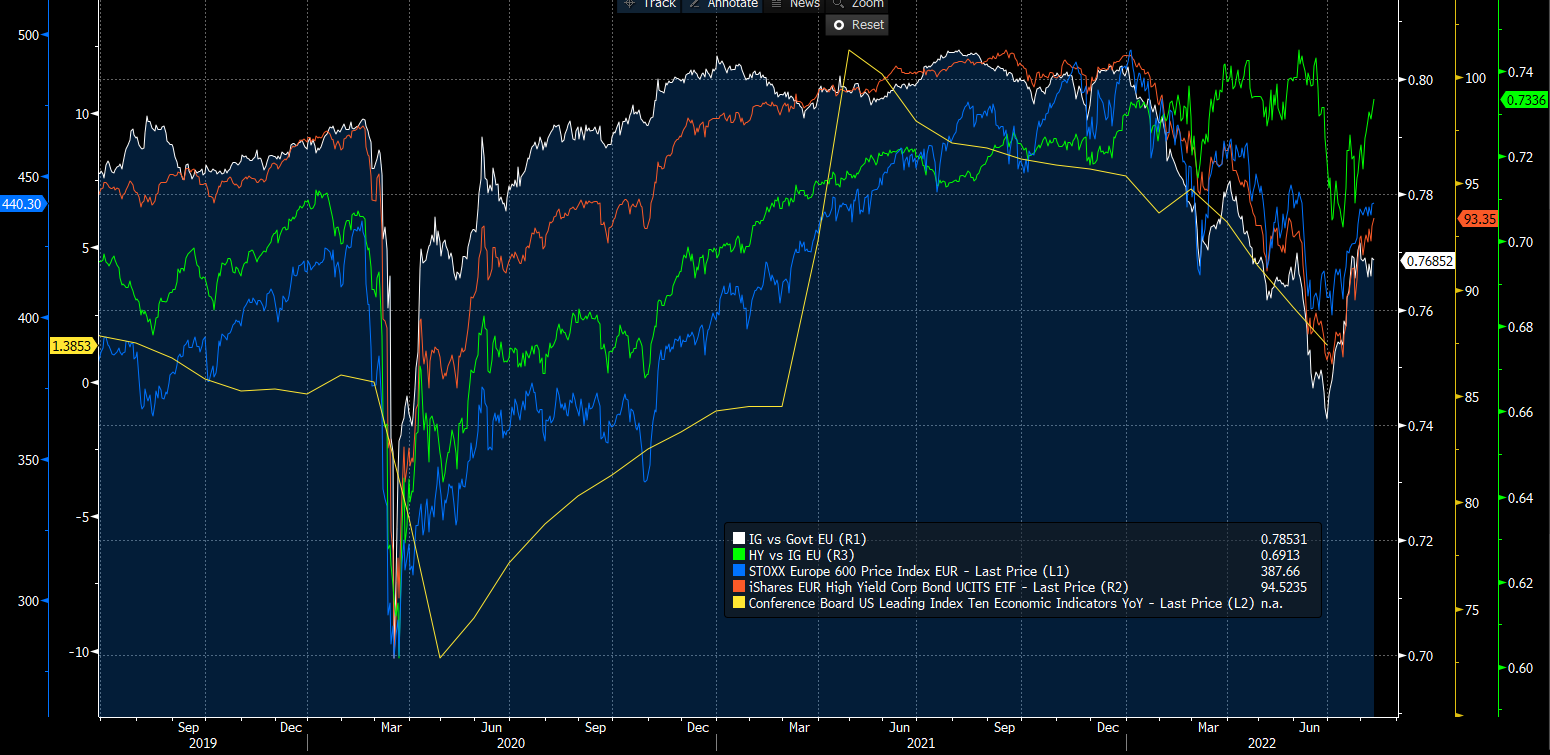

Below one of the chart that I use usually showing the LEI indicator but also the HY ETF (a good proxy of liquidity). IG to Govt ratio, the HY to IG ratio but also the stock market are driven by the same driver: “Liquidity”.

2 Micro

Micro part focuses on companies fundamentals (aggregated at index level). I look here at profits and leverage (but other metric to look are also FCF or Interest coverage. As I said it’s only a first step. Profits and Leverage remain benign in this part of the cycle. Below I show you the BF12m EPS for SXXP. A lot of words were written about this and the fact that with PMI/ISM going down EPS remained too high and need to go down. So take it with “Cum grano salis”.

Other two indicators that I monitor are the distress ratio (this started to rise) but remain below the high of the past years and the rating drift (the upgrade to downgrade ratio). For this I talked about the good link between the PMI and EPS revision with rating drift (as showed in the chart below).

My expectation is that a wave of downgrade is coming, but for the moment real data (below the RATT function on bloomberg) is denying me.

The cumulated score for micro is “1” positive for the moment.

3 Valuation

I’ll not spend a lot of words on this. It’s basically easy as it sounds. I look at spread vs history, at spread vs yield ratio and versus other alternatives. Some focus on this one. It’s a a rank of an yield to risk ratio. For stocks it takes into account the growth part of the story and not only the carry. At the moment IG is offering the juicy risk-return based on my simple calculation and amid the recent rally in spread the aggregate score is “only” 0.7.

4 Technicals

In this part I try to investigate better the demand/supply balance. For demand I use the flow in IG and HY ETF (good flow inside, good demand of bonds in the future) while supply is basically new issuance. We know there is a lack of supply this year, and below I showed the data for IG. For this reason there is a 1.9 supportive score on it.

I added other two indicator, one is the BNP positioning indicator. It was very negative in the past week and now rebounded a bit. I reversed the score in my scorecard, given it’s supportive. They calculate it using cash balance, CDS index data, etc.

I have also a positioning indicator calculated by myself, regressing the main mutual fund of the asset class vs their benchmark, trying to calculate a beta/positioning stance of the average fund. It seems funds derisked a bit (but not so much) and after that returned to buy. So mixing this signal with that above they hedged their positioning using derivatives.

5 Sentiment

It’s the last point. Here I use Swap Spread (as a proxy for financial risk and P/E of equity as proxy of risk aversion. While I used the Vstoxx volatility as a contrarian indicator (low volatility - more risk ahead). The score here is very negative.

The Final score

Looking at all indicators together we have an environment for credit investment very difficult to trade. Fundamentals from a macro point of view remain negative and central banks are not supportive anymore (they are increasing rates and removing QE).

Companies fundamentals are in a good shape (they remained defensive in this cycle) helping them to reduce debt and not invested a lot (but someone preferred to return cash to shareholders). Going forward there is the risk of a EPS bloodbath, and a wave of downgrade.

Valuation are interesting, despite less generous than in the past and I continue to see value only in IG at the moment, less impacted by growth risk.

Technicals are mixed (with low demand but also low supply) and positioning is not extreme.

Sentiment is not good given despite this market rebound.

To sum-up my reading for credit is almost neutral and I prefer to trade the market in a defensive way preferring:

Investment grade to high yield;

Senior to subordinated bonds;

Defensive sectors vs cyclicals;

It’s all for this cliff in the first piece about credit portfolio management and strategic asset allocation. If you don’t want to skip the next parts (on tactical allocation and bonds picking) subcribe now and be free to share it to friends and colleagues.

I hope you find it usefull as it’s for me.

Enjoy and trying to add variables or parts you think are usefull for you, but remember that simple is better!

“Everything should be made as simple as possible, but not simpler” Albert Einstein

It's a pleasure to know you liked it.

Stay tuned for the other parts.

I was waiting for this piece & thank you for keeping promises! Superb piece & great methodology. I particularly like your EUR focus to which I can relate. I‘m glad and thankful to be able to build on that. Danke!