A framework for RV in duration

A cross country approach

Good morning to all. As promosided all write about my framework to spot idea of RV on duration across countries. This is the first piece of this type and it doesn’t want to be an educational. It’s only the starting point of my analysis.

So let’s start but first some words about this:

1) Instruments traded: here I look only at the most liquid and traded instruments of the bonds future market. We have the 10y futures of US, Germany, Japan, Uk, Australia, Canada and Sweden;

2) This version is static, it’s an image of the current situation, but I have also a backtested one. For simplicity I’ll use the static one here;

3) I use only as a starting point, and I don’t trade it systematically.

The model:

Here I use a scorecard approach (giving a score from 1 to 7 - 1 the best, 7 the worst) at each variable. I know could be better using other appoach, and in other job I did it. At the end the average score is calculated as a fixed weight (with more weight on value). In other job I tried to apply a variable weight (giving the better strategy a high weight, and it’s work) but as said this is a static one in this case. Do your homeworks and enjoy!

The variables:

I tried to use the most used and factors applied usually at the equity market (momentum, mean-reversion, value) adding something more of macro:

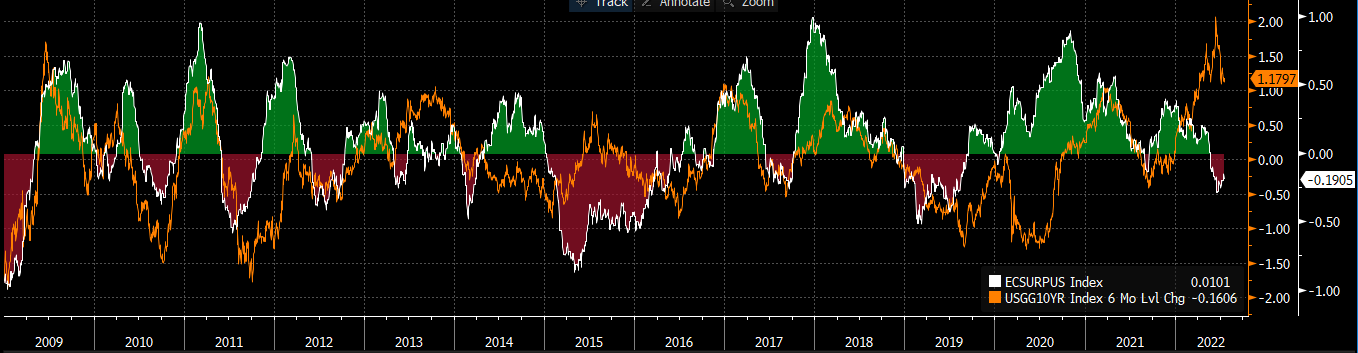

Macro surprise. I use Citi surprise index. The reason is easy. Usually weak surprise index drive interest rates lower (below the surprise index in US vs the 6 months change in index level). This indicator is mean reverting and despite not be so usefull recently has a good track record.

I look at the 3M change of the surprise index and below it’s visible the divergence between Europe/US vs Autralia (that explain the high score for the last one and a gree score for Europe and US);

Bond momentum: it’s easy, the trend is your friend. I take the 1M change in 10y yield, going long the best performers and shorting the worst;

Equity momentum: this variable is not so usefull YTD given that correlation between equity and bonds flipped from negative to positive but the ratio is easy. A strong equity market means a stronger economy and a possible switch from bond to equity. I take the 1 month % return of the most important equity index and assign a high (negative for bonds) score to the best performing market. In the last month SPX had a 4.25%, while Canada is negative -1.77%

Value: it’s the same idea of value in equity or credit. Buying something cheap and selling something rich. How to measure it? There are a lot of way to do it. My approach is to make thing easier, I prefer a easy and fast thing to a more complex and too long one. We know that rates are driven by growth, inflation and central bank actions. It’s why I used a simple FV calculated as FV=GDP + INFLATION. I use bloomberg consensus. To compare better the different countries and to remove the swap spread effect (especially europe) I used the 10y swap rate as market value and not the government yield.

For who doesn’t know what is swap spread is the delta between a governement bond yield and the swap rate. For example the germany 10y bond yield is 80bp tighter than swap. The explanation could come from the risk free premium to the tighteness in repo market (high demand of risk free collateral).

Carry: it’s the bread and butter of any fixed income investor. I calculated it as steepness of the curve (3M vs 10Y)

TO SUM up:

I know that it’s not perfect but it’s impossible to build a perfect one. There is always a new variable to consider but at least it’s a starting point to think, knowing that you have checked the most important one.

From other jobs on it (where I backtested) the strategy it’s possible to have a positive return sistematically trade long/shorts the futures, but this go away from the purpose of this piece. What matters is that the different strategies balance themself and help to navigate the movements of the market.

How I used recently?

Some weeks ago I entered a short position on Japan 10y (like most of us made) fr

om a global macro approach.

Recently the situation changed (the sentiment pendulum shifted from inflation to recession) and I started to fear that an outright short position on bond it’s not a great idea.

So, I decided to take a long position on bund futures to balance it.

That’s all.

If you liked this type of piece let me know and share it.

I'd be interested in a post on your credit research approach. You shared here how you partially analyze the macro. How about the micro?!?!

awesome, appreciate