Bond Basis Trade

Everything you always wanted to know about this esoteric trade, with a more practical approach

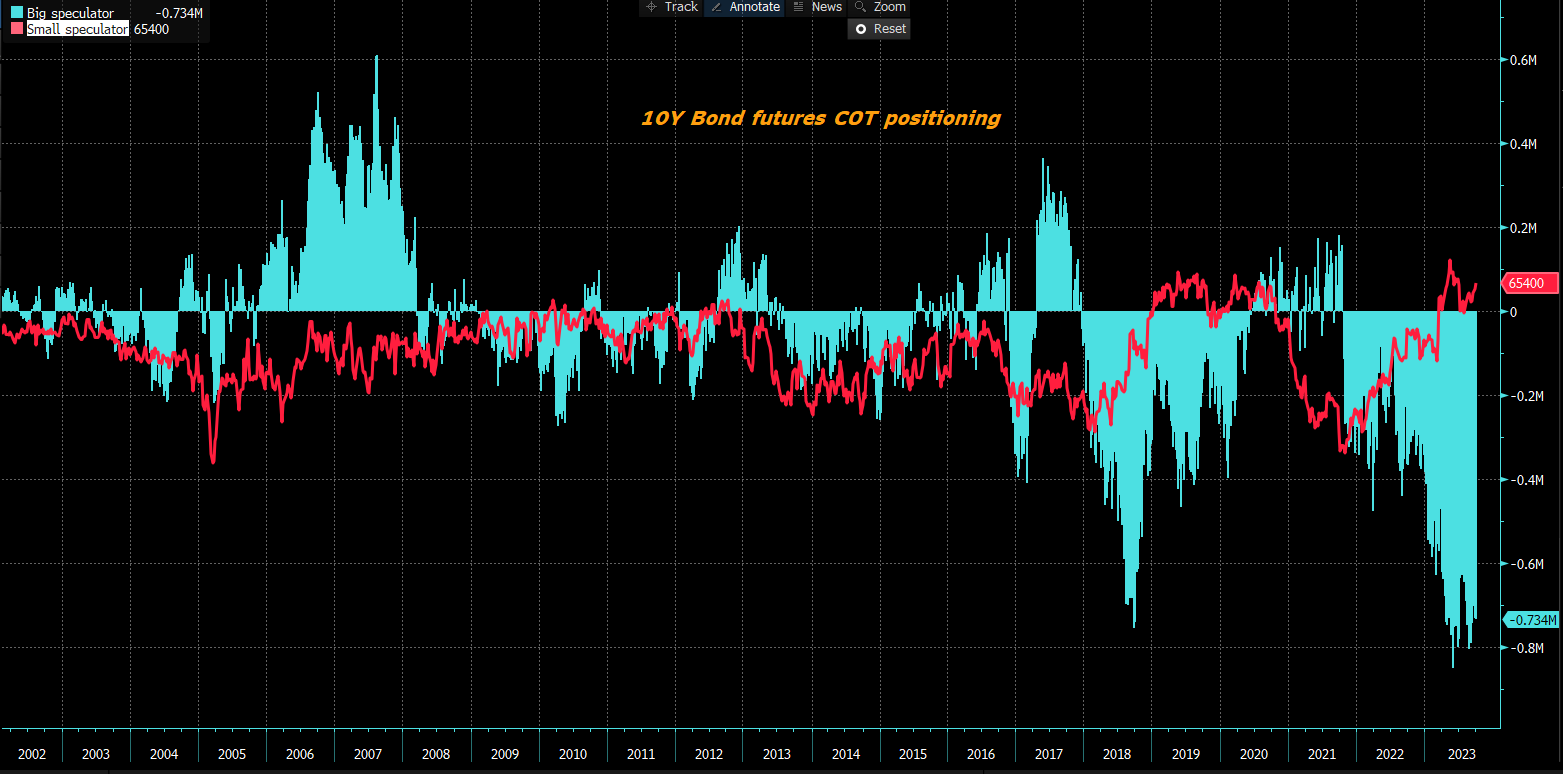

Positioning on treasury futures is decidedly short, if you look at the large speculators. If at the beginning the consensus was that the market was short of bonds and that it could therefore be interesting to buy bonds from a contrarian perspective, subsequently the belief became increasingly widespread that behind this positioning an esoteric trade was hidden for most people: the basis trade.

Precisely for this reason, for a better idea on positioning it is currently more correct to look only at small speculators in the COT report.

But what is the basis trade on bonds? It is an arbitrage that involves the simultaneous purchase/sale on a cash security and the opposite purchase/sale on a futures (to hedge the interest rate risk). Nothing more and nothing less.

Dividing the two types we will have:

“Cash & Carry arbitrage” where the trader buy the cash bond (and financing it on the repo market) and sell the future;

“Reverse Cash & Carry arbitrage” where the trade buy the bond future and sell the cash bond.

Now, with the caveat that this is not a technical post with the aim of explaining in detail all the mathematical part behind it, let's see a practical example.

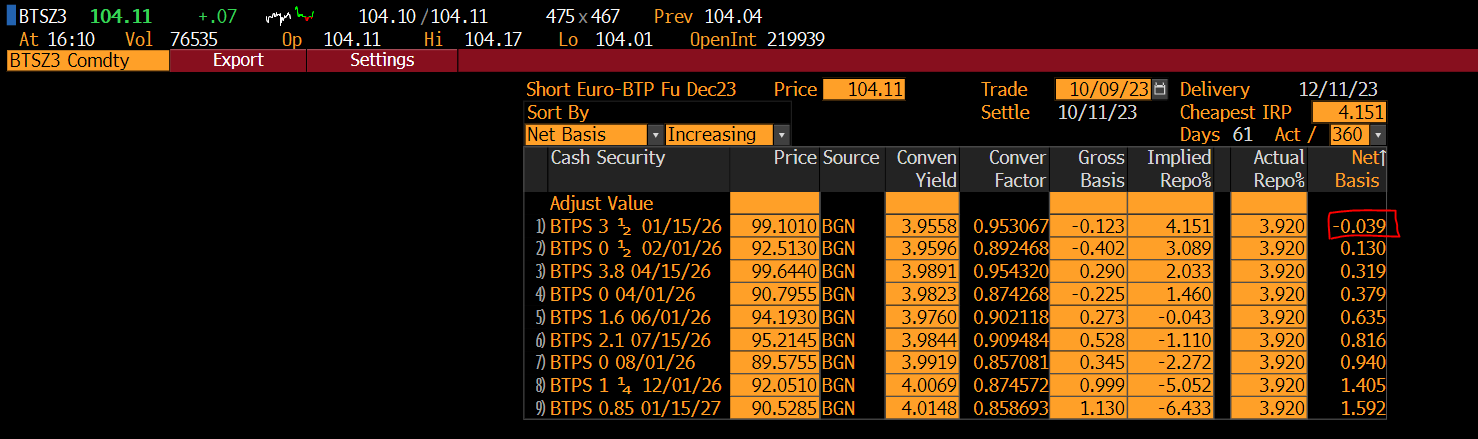

Below it’s the DLV function on Bloomberg (Cheapest to Deliver) using the BTSZ3 future (Short term BTP maturity december 2023). The first bond is the CTD (cheapest to deliver). In this case the implied repo of the bond is higher than the actual repo on the market, so the net basis, that it’s equal to:

Net Basis = Gross Basis - financing cost where

Gross Basis = Cash Bond prices - Futures prices * Conversition Factor

is negative (-0.039). That’s is equal to 39 euro of profit for each futures sold.

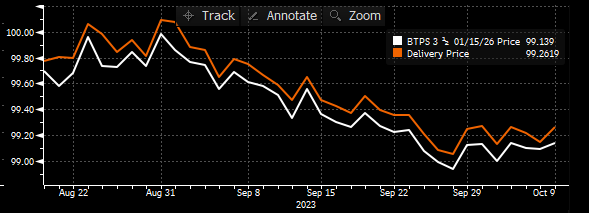

In this chart below you can see in orange the delivery price of the futures (futures prices x Conversion factor) while in white the bond cash price. The spread between the two is the gross basis.

Due to the fact that the contract size of the future is 100.000 euro, for every bond futures sold, you have to buy 100.000 of nominal of cheapest to deliver. Shorting 10 bond futures and buying 1M of the bond the profit will be 390 euro.

Below you can see the net basis on the CTD for the generic ticker of the futures to have a better point of view of the history of the trade.

This is exactly what hedge funds (big speculators) are doing at the moment. Buying the cash bonds and hedging it with futures. As you can see from the potential profit and loss, to make “big money” they need to leverage themself and this is clearly a risk for the system and the bond/futures market.

If the net basis is positive (the implied repo on the cheapest to deliver is less than that one on the market) the trade will be the opposite (buying the future and sell the bond).

Clearly there are a lot of risk on this type of trade despite are called “arbitrage” like the cheapest to deliver change or risk of a blowout of repo market forcing traders to close positions.

For now I think that's all. If you liked reading it and want to support my job, please share this piece to friends and colleague and subscribe to the newsletter using the link below.

I appreciate a lot your comments but I don't want to make my piece behind a payment wall, so if you want to support me I created a page on "Pay me a coffee' https://www.buymeacoffee.com/CreditMacroMicro