Hedging credit risk

CDS "Credit default swap" - Everything you always wanted to know, with a more practical approach

It's been a few weeks since I wrote my last piece (which was about trading the interest rate curve). This time I want to spend sime time talking about credit risk and how to hedge it, in particular using CDS (Credit default swap).

I think it's a crucial time to talk about it, precisely because credit spreads are at very low levels and often not offering enough premium versus fundamentals. In the first chart below I plotted the EUR IG spread vs the ECB lending standard, while in the second chart vs the Eurocoin growth indicator (inverted - the standard relation is high growth = low spread and viceversa).

Let’s take the case we are the portfolio manager of a big mutual fund specialized in european investment grade corporate bonds and after a good year and good performance (maybe through some good sectoral or name specific choices or maybe through an aggressive allocation to beta parts), and after taking some considerations regarding business cycle (or speads valuation), we want to reduce the directionality of our portfolio (aka beta reduction). How to do it?

One simple choice it’s to sell some bonds in our portfolio! But maybe I am convinced of the validity of the analysis underlying my single name picks or I want to do it quickly and not through the sale of 10/15 positions. The solution is to buy protection via a CDS. Using Investopedia definition:

“A credit default swap (CDS) is a financial derivative that allows an investor to swap or offset their credit risk with that of another investor. In a credit default swap contract, the buyer pays an ongoing premium similar to the payments on an insurance policy. In exchange, the seller agrees to pay the security's value and interest payments if a default occurs.”

Using CDX <go> on Bloomberg you can see the different and most liquid/traded CDS. I am Europe based and I will talk of EMEA products. We have an index for every needs:

Itraxx Europe (Euro Investment grade)

Itraxx Crossover (Euro High Yield)

Itraxx Sr Financial (Senior Financials)

ITraxx Sub Financial (Sub Financials)

Using the description of Bloomberg for the Iraxx Europe, the index is composed of 125 names (equally weighted). The most important maturity is the tenor 5Y (mostly in line with most of funds and ETFs duration. The various CDS index roll every 6 and the actual “on the run” product is called ITRAX EUR S39 with a maturity date of 06/2028.

Let’s pass now to a practical example. Below I will use CDSW (Credit default swap valuation) function. Our portfolio is 200M of notional and for simplicity we have a credit beta (how our portfolio moves when the spread of the index moves) of 1. We want to cut our exposure in half (because we expect a great recession with spread spiking from 84bp (actual level) to 160bp (80bp of widening). We will buy protection for 100M.

You are surely wondering what is coupon (bp) (that in this case is 100bp) while the CDS Itrax Main Eur is at the moment 71bp. Well it hasn't always been like this, but to simplify cash flow payment flows, years ago it was decided to divide the products into buckets. So in this case, despite the product spread is actually lower (71bp), every year we will pay a coupon of 100bp (on a quarterly basis).

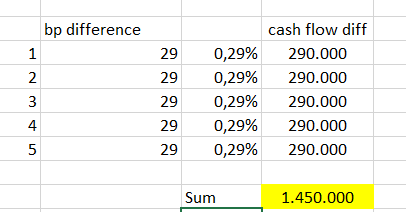

At the same time (as we pay a higher premium every quarter) we will receive an upfront payment (in this case of 1,486,055 euro) that is equal to the discount value of a stream of cash flow equal to (100-71 bp) * 100M for all the maturity of the CDS. Below I want to show you rapidly (not discounting and with only annual payment) that the sum of this stream is a similar number.

Let’s go now directly at what happen at our portfolio. We said we have a 200M portfolio:

If our portfolio average yield is 3,5% we assume we could collect annualy 7M of coupon (for simplicity we assume that the prices of the bonds are all at 100 and that the yield is similar to the coupon)

We will pay annually 710.000 of CDS payment (our trade spread of 71bp x 100M of CDS contract

So our net cash flow will be 6.29M (equal to cpn less the CDS premium)

Now “fortunately” our assumption of recession and spread widening it’s finally happening (and “fortunately” in just 1month after we bough protection) and cash spread pass from 80bp to 160bp and the spread of CDS Itrax Eur Main from 70bp to 150bp (a similar 80bp widening). What will be our profile?

Let’s see again the CDSW function, now the trade spread is 150bp while the cash amout passed from -1,486,000 to + 1,867,000 (equal to a profit on the hedge of 3,353,000 if we close immediately the CDS. Always in this function is helpfull to see the voice “price”, in this case is helpfull to imagine the CDS like a bond that we shorted and the passed from 101.24 above to 97.89 now (after the spread widening), a fall of 3.35% exactly (100M * 3.35% = 3.35M).

Ok we will face a fall also in the value of cash portfolio (200M x 3.35% = -6,7M), but our hedge will help to mitigate partially this, closing the year with only a loss of 3.3M and not like a lot of our competitors or our benchmark.

For now I think that's all. If you liked reading it and want to support my job, please share this piece to friends and colleague and subscribe to the newsletter using the link below.

I appreciate a lot your comments but I don't want to make my piece behind a payment wall, so if you want to support me I created a page on "Pay me a coffee' https://www.buymeacoffee.com/CreditMacroMicro

Credit_Junk

Great actionable insights!!

great coverage, thank you!