THE CALENDAR TRAP

Why your "June" SOFR is still alive in August

Good morning to all, today I want to write a brief piece regarding difference between SOFR/Sonia and EURIBOR futures.

If you are coming from the old-school Eurodollar or Euribor world, the SOFR (or SONIA) futures screen looks like a glitch. You see a contract named “JUN 26” and you expect it to be dead and buried by mid-June. Instead, you find it alive, kicking, and actively trading in the middle of a late August heatwave. No, it’s not a brokerage error. You’re just looking at a different species of derivative.

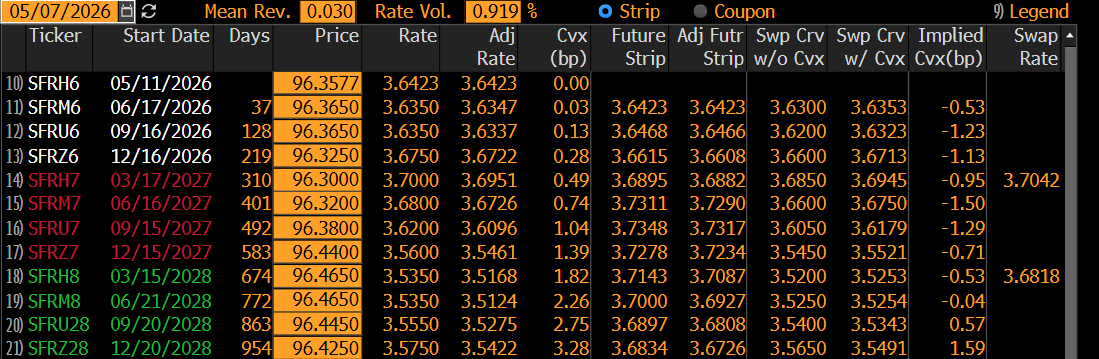

In the example below we can see that March contract for SOFR (SFRH6) is trading yet.

1. The Philosophical Shift

The global transition from IBOR (Interbank Offered Rates) to RFRs (Risk-Free Rates) is not just a change in index; it is a change in temporality.

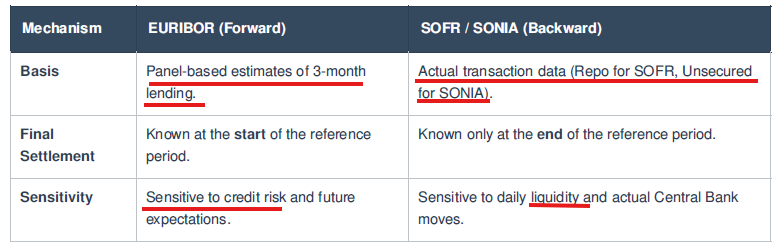

The Euribor world is simple, almost lazy. When the fixing happens in June, the market decides today what the next 90 days are worth. It’s a Forward-Looking term rate. Once that number hits the screen, the uncertainty is gone. The future has been “priced in” at the start. That’s why Euribor futures stop trading the moment the period begins. There’s nothing left to bet on.

SOFR (and its UK cousin, SONIA) is a Backward-Looking beast. It doesn’t care about what the panel thinks today; it cares about what actually happens in the repo market tonight. And tomorrow night. And the night after that for 90 days straight.

When you trade a JUN 26 SOFR Future, you aren’t trading a “point” in time. You are trading the Arithmetic Average of every single overnight rate from the third Wednesday of June to the third Wednesday of September. You are essentially trading a “thermometer” that stays in the mouth of the market for three months.

Technical Note: Compounding vs. Arithmetic Average

While both are RFRs, there is a technical nuance:

SONIA Futures: Usually use compounded daily rates. This reflects the “interest-on-interest” nature of cash accounts.

SOFR Futures: Use a simple arithmetic average of daily rates (though the cash market often uses compounding).

2. Why this matters (The “August Hike” Scenario)

Imagine the Fed wakes up on August 15th and decides to hike 25bps. If you hold a June Euribor position, you don’t care. Your rate was locked two months ago. But if you are in the June SOFR, your P&L just took a hit. Since you still have 30 days of “prints” left in the accrual period, those higher daily rates will pull the final average up, and the future price down.

This is the fundamental shift: In the RFR world, you are exposed to monetary policy real-time during the life of the contract. You can’t just “set it and forget it” at the start of the quarter.

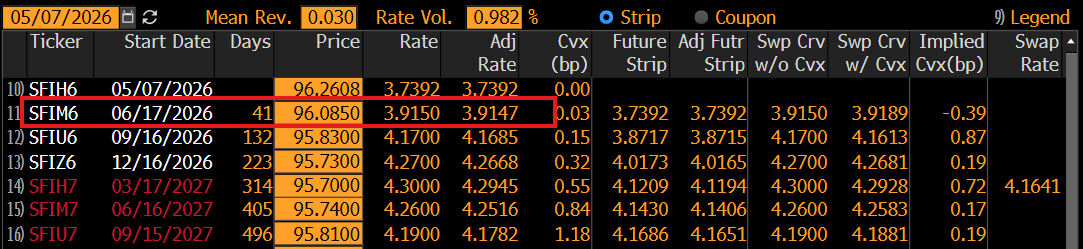

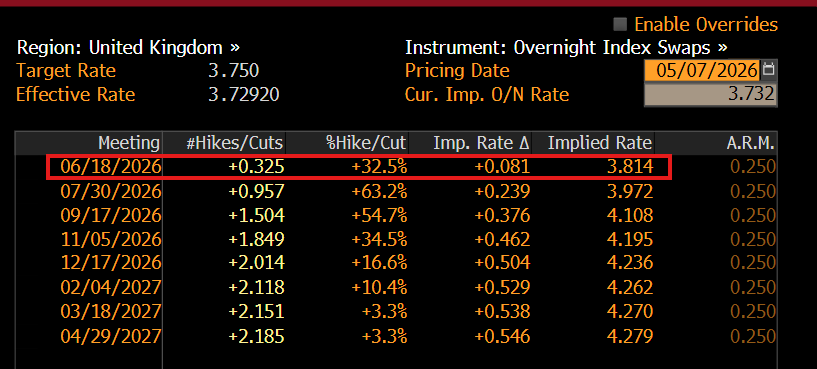

Let’s do a practical example, taking the June Sonia future (SFIM6), trading at 3.9147% yield. Comparing this yield with the BOE target rate (3.75%) it would appear that the market is pricing in a 16bp increase for the month of June, versus the 8bp priced in by the WIRP function, which prices increases on the precise dates of central bank meetings.

This is because, as we have seen, the reference period starts in June and ends in mid-September, exactly a few days before the September 17th meeting. During this period, there are two meetings June and July,with a cumulative increase of 23 basis points).

Doing some quick calculations (we saw that the Sonia is a compounded average), with the reference period starting on June 15th and an 8bp increase priced starting on June 18th. At the July meeting, there was almost a full increase with a cumulative 23bp.

So until July 30th (45 days), we have an increase of 8bp, while for the following 45 days or so (from July 30th to September 15th), we have a priced increase of 24bp. The average is approximately 16bp, which is exactly what the Sonia Jun 26 futures price is.

3. An alternative solution

Only recently (last 2/3 years) ICE started the trading of a new type of future, the MPC Dated SONIA Futures (there is also a dated Euribor version) that cover exactly the period between one meeting and the next one. The problem is that these are not contracts that have the necessary liquidity to be traded (it has 13k contracts of open interest against the 3 million of Sonia 3M).

Next time you see the JUN 26 SOFR moving in August, remember: it’s not a bug, it’s a feature. You’re trading the path, not just the destination. Don’t be the one caught expecting a settlement that isn’t coming for another month.

It’s all for today. If you liked reading it and want to support my job, please share this piece to friends and colleague and subscribe to the newsletter using the link below.