Weekly Credit Market Review 28 jan

Weekly Credit Market Review 28 jan

A thread from macro to micro

Welcome back to a deep dive in the fantastic world of bonds, always analyzing what happened this week from the very high point of view of macro/narrative to arriving on what happened to single name bonds.

MACRO/NARRATIVE:

The focus this week was without doubts on FOMC. FED was confirmed hawkish but not surprised too much market. The main points were:

Net asset purchases will end in March;

Committee is likely to hike at the next meeting (also in each meeting if needed always remaining data dependent on his decision).

At the moment market is pricing 5 hikes this year.

Geopolitical risks remains with Russian troops amassed on the Ukrainian border. Diplomatics talks continue between Moskow and Washington but uncertainty will remains high.

In Italy monday started the process to elect the new Republic’s president. While the powers are limited the risk are in the new government. The current Prime Minister, Mario Draghi, is seen as the frontrunner so who will replace him?

MARKETS:

After FED rates market looks like a bloodbath. Short term rates drove the movement and curve flattened aggressively with fears of CB behind the curve that will end to tighten too much and kill the economy.

Equity was impacted by high real rates and high valuations but also a decreasing momentum in growth. In this environment growth stocks (Nasdaq and others high durations sectors) suffered the most.

In FX dollar returned king with high spread in yield (vs other DM) overweighting the low performance in equity versus the rest of the world. On the subject of “speculative” flow in FX I reccomend you to read this piece of @macroops talking about the framework of Soros to looking at FX.

https://macro-ops.com/george-soros-currency-framework-for-markets/

In commodities gold were sold due to the negative link with real rates, while the energy sector closed the week very strong with oil (below the brent CO1 future) above 90$ per barrel.

Demand is strong:

timespread curve is in backwardation;

oil stocks/inventories continues to going lower

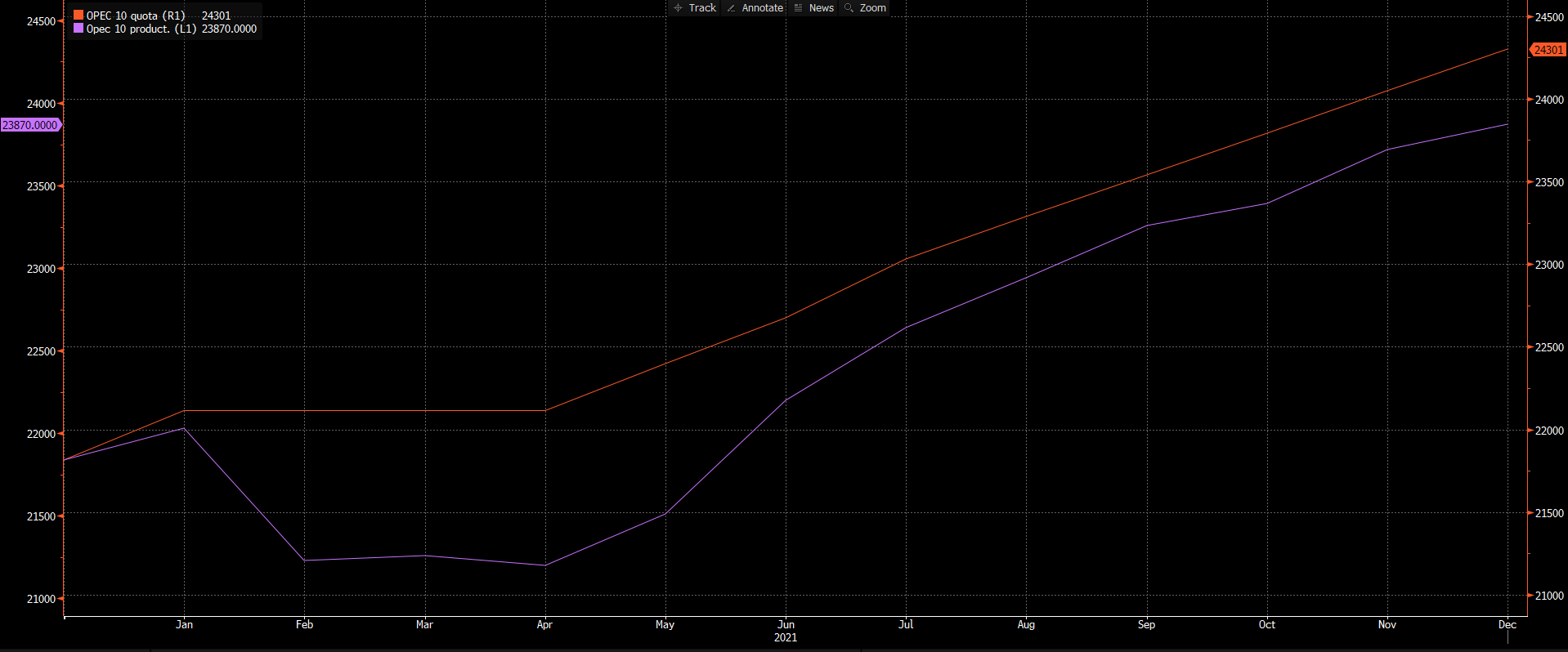

while supply is impacted by low capex/ESG forces at the same time spare capacity in OPEC countries is low or below expected. To be sure look at productions vs quotas.

Closing with the credit market spread remained under pressure. High rates and volatility are not friends of carry trade.

HY cash widened 15bp, together with implicit spread of HY (more driven by asset allocators) but the positive news is that flow remained muted in dedicated funds while some outflows appearead in ETF.

MICRO:

Reporting season started also for HY issuers. This could be a driver of dispersions in the next weeks but the end of blackout period could also give a green light to a new wave supply.

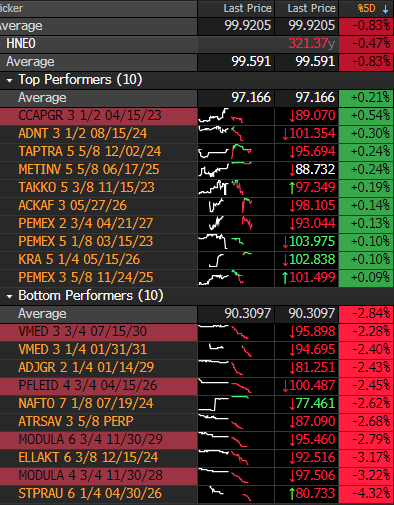

Not so much winners/green name this week. Just to name one or two:

ADNT (Adient) and KRA (Kraton) launched corporate actions (tender offer and call on their bonds)

On losers the list is longer:

STPRAU (Standar Profile), MODULA (Modulaire) and ELLAKTR (Ellakort) given the high beta of the names or dethe strong rebound the week before;

ORPFP (Orpea) while not in my HY list being not rated the move was huge and with a story out (allegation in a new book talking of mistreatment of elderly residents to save money). Reputational risk is live here!

I hope you enjoed this weekly. Have a great weekend.