Weekly Credit Market Review - Apr 1

Weekly Credit Market Review - Apr 1

A thread from macro to micro

Welcome back! Before entering in the details of this new weekly recap, I want to thank all subscribers. We are now at 100!

So, let’s go.

MACRO/NARRATIVE:

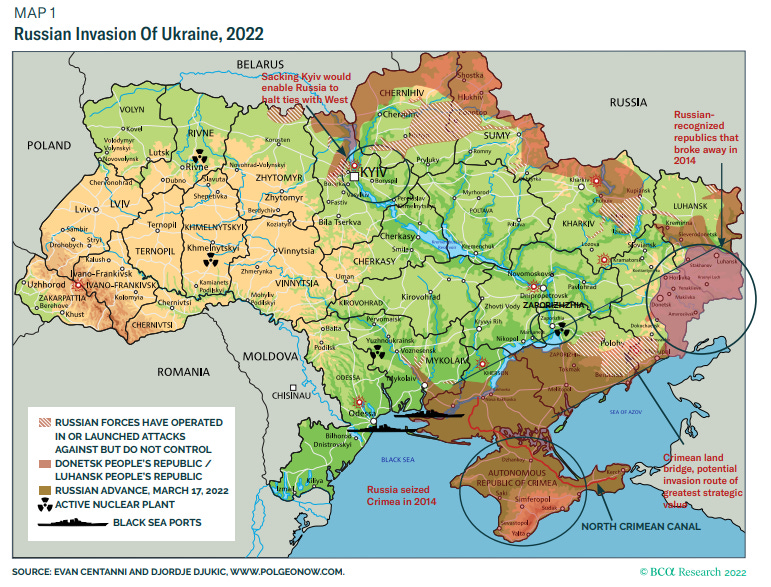

Market continued to focus on geopolitical risk around Russia/Ukraine conflict. There was an other tranche on talk in Turkey between the two parts and some hope of ceasefire helped the sentiment. Russia troops said to focus only on south operations of Donbass but the bombings continued also in the west of the countries.

Also related on the conflict during the week Putin entered in a new phase of confrontation with EU asking from april payment only in ruble for gas:

*KREMLIN: RUSSIA MAY CHANGE GAS PAYMENT CURRENCY IN FUTURE

*KREMLIN: GAS WILL CONTINUE TO FLOW WHILE RUBLE PAYMENTS

PENDING *KREMLIN: RUBLE PAYMENTS FOR APRIL GAS DUE IN LATE APR-EARLY MAY

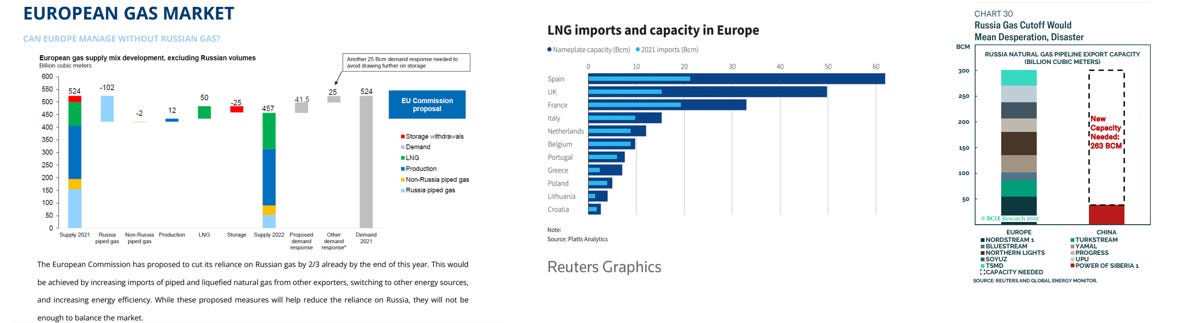

Despite gas continue to flowing today, these are related to old and payed yet contracts. While this is a problem for sure for Europe that import 30% of his gas consumption from Russia (see in the first graph on the left above) and has only a limite capacity of regasification (US promised to increase of other 15BCM of LNG the export to Europe for 2022 and to arrive at 50BCM in the future), also Russia has a problem with export of gas with a lack of pipeline to sell it in China for the moment.

From a macro point of view the focus on the market continued to be on inflation with strong print in Spain and Germany. The CPI estimate for march for Eurozone was at 7.5% vs expectation at 6.7% (core at 3%). At the same time the leading indicator knowed as PMI started to show some weakening effect related to war and the impact of high price on consumers:

Spain PMI manufacturing 54.2 from 56.9

Germany PMI manufacturing 56.9 from 57.6

Italy PMI manufacturing 55.8 from 58.3

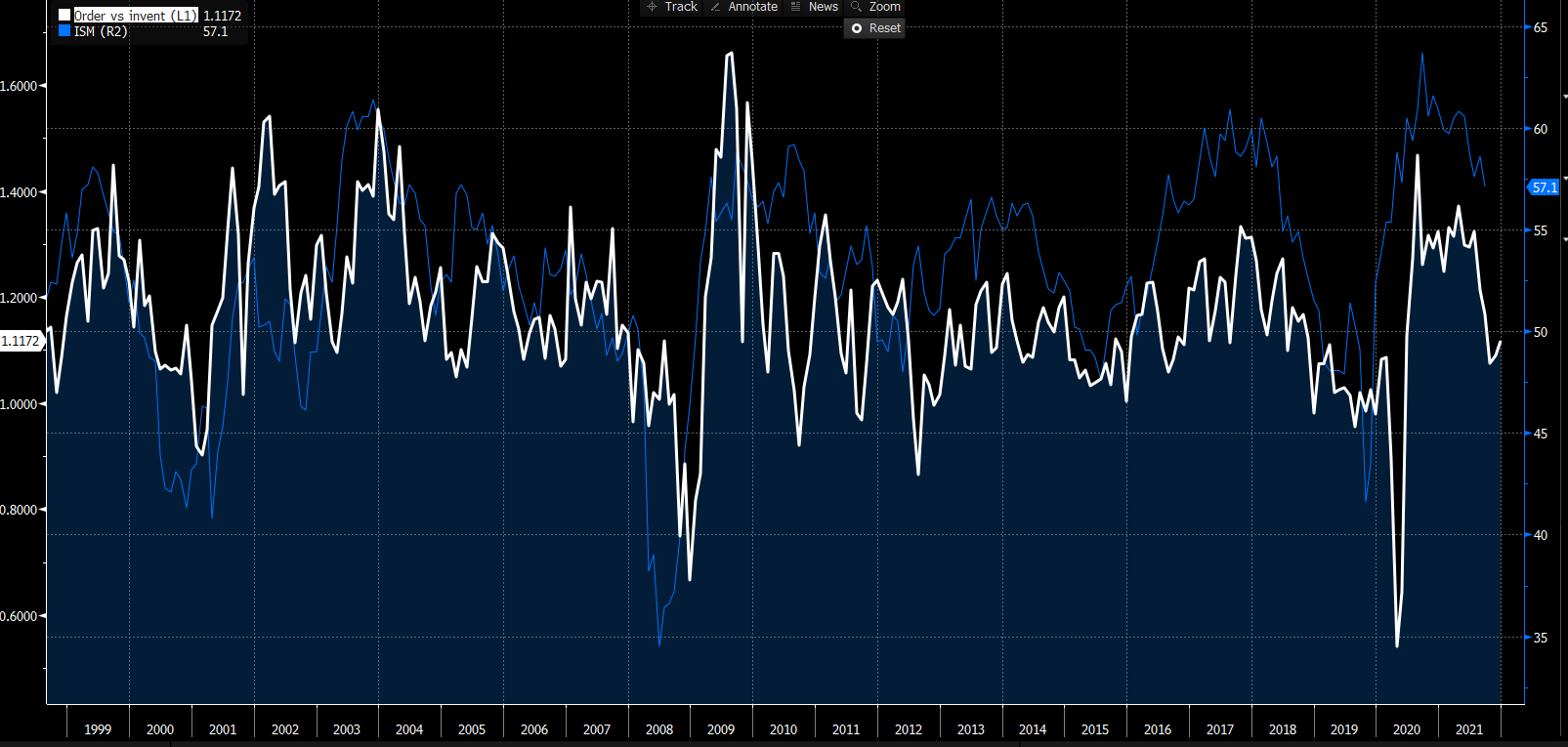

But also in US it’s the same story (slower growth), with ISM manufacturing PMI to 57.1 from 58.6 (below the drivers and the possibile effect of a declining orders to inventories ratio on future path of PMI or ISM.

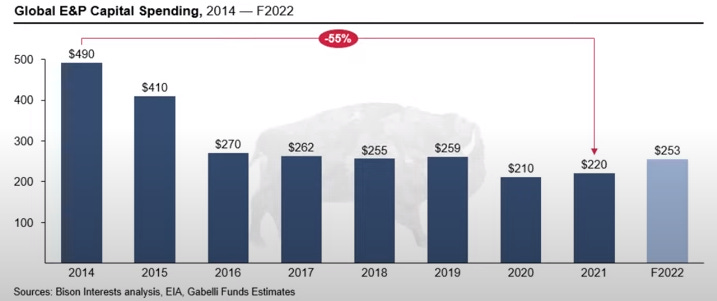

And finally some words on oil and Biden. The president (to defend consumers) promised to supply market with an additional 1M barrel per day of oil (directly from strategic reserve) for 180 days. Just some considerations on this:

Oil market appeared undersupplied for the moment of 1/2M barrel per day, so some pressure are removed for 2022 true;

But this will bring down SPR (Strategic petrolum reserve) below 400Mbarrel, a very low level but bringing down prices it doesn’t not incentivize new investment by shale oil operator, so limiting new supply next year;

This arrive after severals years of low capex of oil operators, lack of incentives, high pressure from ESG, etc, etc. Why not to finance directly capex of operators? There is a lack of investment equal to 2bln at least.

And finally there is the problem of the supply destruction of russian oil production that could be in area of 1/3M barrel per day (lack of demand and less techicals support of occidental engineering)

MARKETS:

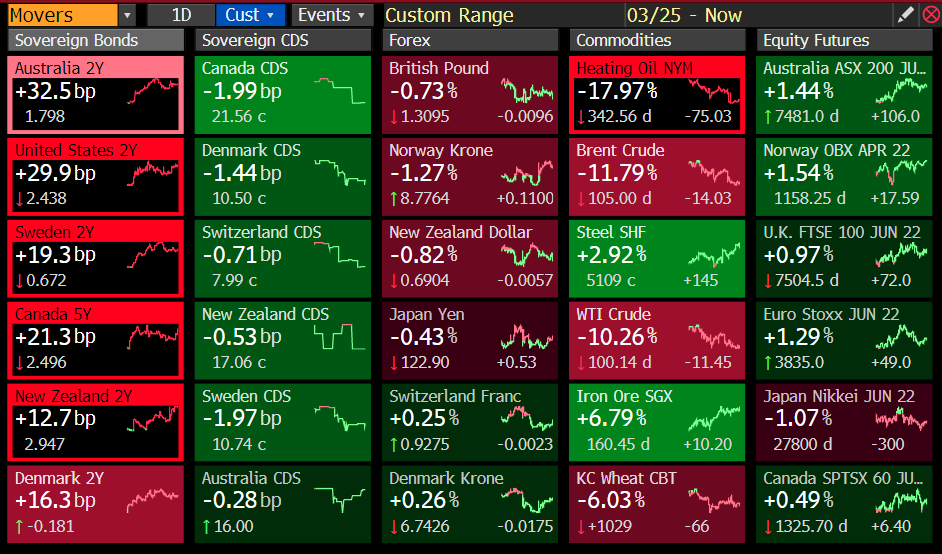

Due to high print of inflation and hawkishness by central banks (that need to defend their mandate to mantain stable inflation) rates continued to drift higher driven essentialy by short term part of the curve (tipically of a hike cycle).

A lot of talks were written on the flattening of yield curve. Despite less releable due to central banks actions but Dr Curve is always usefull as recession tool. Below tracking the delta between Michigan and Conference board (more late cycle) consumer optimism.

Risky assets were positive this weeks with equity in Europe (Euro Stoxx) up +1.29% and in US (SPX) +0.5% but below the surface some problem continue to appear using the len of intermarket analysis. The ratio of banks to Sxxp doesn’t follow the incrase in rates, but is following the flattening of the yield curve (first chart below) and despite SPX recovering all the losses related to invasion, there is a strong divergence on the ratio of cyclicals vs defensives (second chart below).

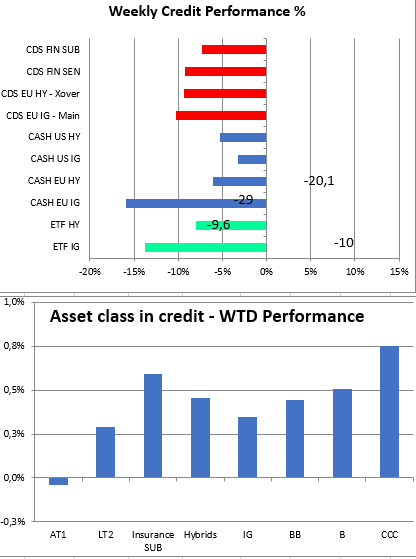

In credit market spread tightened near the level prevaling before the invasion too, thanks to hope of a near cease fire. This week both IG and HY tightened 20bp at least but given the different spread the tightening was stronger in IG in % term. All the asset class performed well with a positive total return.

But risks on growth remain, so in this context I prefer:

defensive to cyclicals;

investment grade to high yield (hybrids to BB, AT1 to B). I prefer subordination to growth risk.

In commodities, clearly, the energy subsector underperformed the index with oil losing 11% given the news on SPR release, while Natural gas was strong due to the request of Putin we talked above.

MICRO:

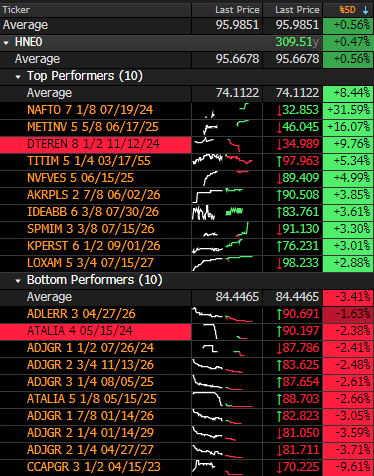

And finally we close as usual as winners and losers on single name.

Again the big winners are related to newsflow from Ukraine (NAFTO, METINV, DTEREN) so I don’t comment again.

Regarding true winners we have:

NVFVES (Fives): reported Q4 21 results slightly above expectation, with a good 2022 guidance;

SPMIM: plan of 2bln capital increase (with support of CDP/ENI for 43% with banks support to) to be voted. S&P increased rating from BB- to BB on it;

LOXAM: good results for a strong name (2.18bln revenue +9.9yoy, strong FCF and leverage at pre-covid level at 4.7x)

Regarding losers we have all the galaxy related to ADLERR/ADJGR after the news of Vonovia to plays down possibile bid for Adler as KPMG report looms.

Sorry, I know I was a bit long today with my words but there was a lot to thinks to talk and analyze. I hope you enjoyed.

Have a great weekend!