Weekly Credit Market Review - Apr 29

Weekly Credit Market Review - Apr 29

A thread from macro to micro

Welcome back and thanks to new subscribers. This week we have a lot to talk, so let’s go!

MACRO/NARRATIVE:

The main drivers of this week were:

The Covid challenge in China with strong lockdown measure. Fortunately some realtime indicator suggest the worst maybe behind us with mobility measures edging up. At the same time Politburo confirmed infrastructure and housing support to boost growth

Hard macro data (as GDP) confirmed the weakness in macro momentum (especially in Europe with low growth on average and contraction in some countries in Q1). US 1Q economy shriked at annual rate of -1.4% but that reflected an import surge tied to solid consumer demand, suggesting growth will return imminently. Inflation was confirmed high on both parts of Atlantic

An aggressive monetary policy by FED pointingto deteriorating economic outlook

High political risk with Russia that halted gas flow to Poland and Bulgaria that refused to pay in ruble

A mixed reporting season with disappointment by big tech like Alphabet and Texas Instruments. Leading indicator here point to pressure on margins.

MARKETS:

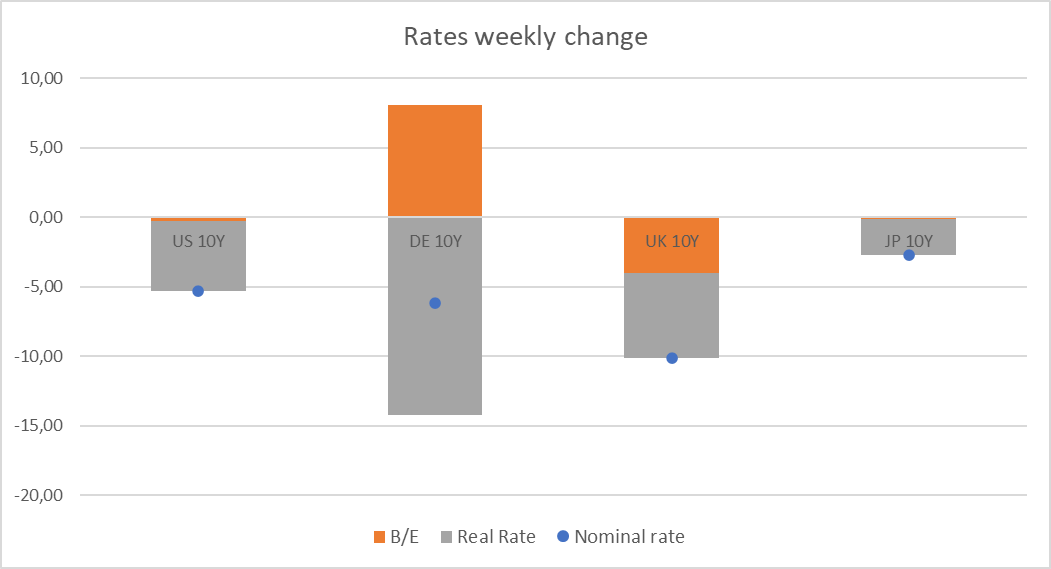

Rates: Overall globally rates are lower or flat vs last friday. Under the surface real rate closed lower (driven by low growth momentum) while in Europe the B/E (implicit inflation priced by market) edged up driven by high gas prices, after the stop of export by Russia.

FX: USD (and DXY) continued to remain the beneficiaries of risk aversion and the aggressive FED. While this week JPY broke above 130 due to BOJ saying t would buy an unlimited amount of bonds at fixed rates every business day as it protects a 0.25% ceiling.

Credit: given these headwinds, it is not a surprise the weakness of credit with spread wider (especially HY more linked to growth). IG widened 4/5bp while HY cash and ETF were 40/50bp on average.

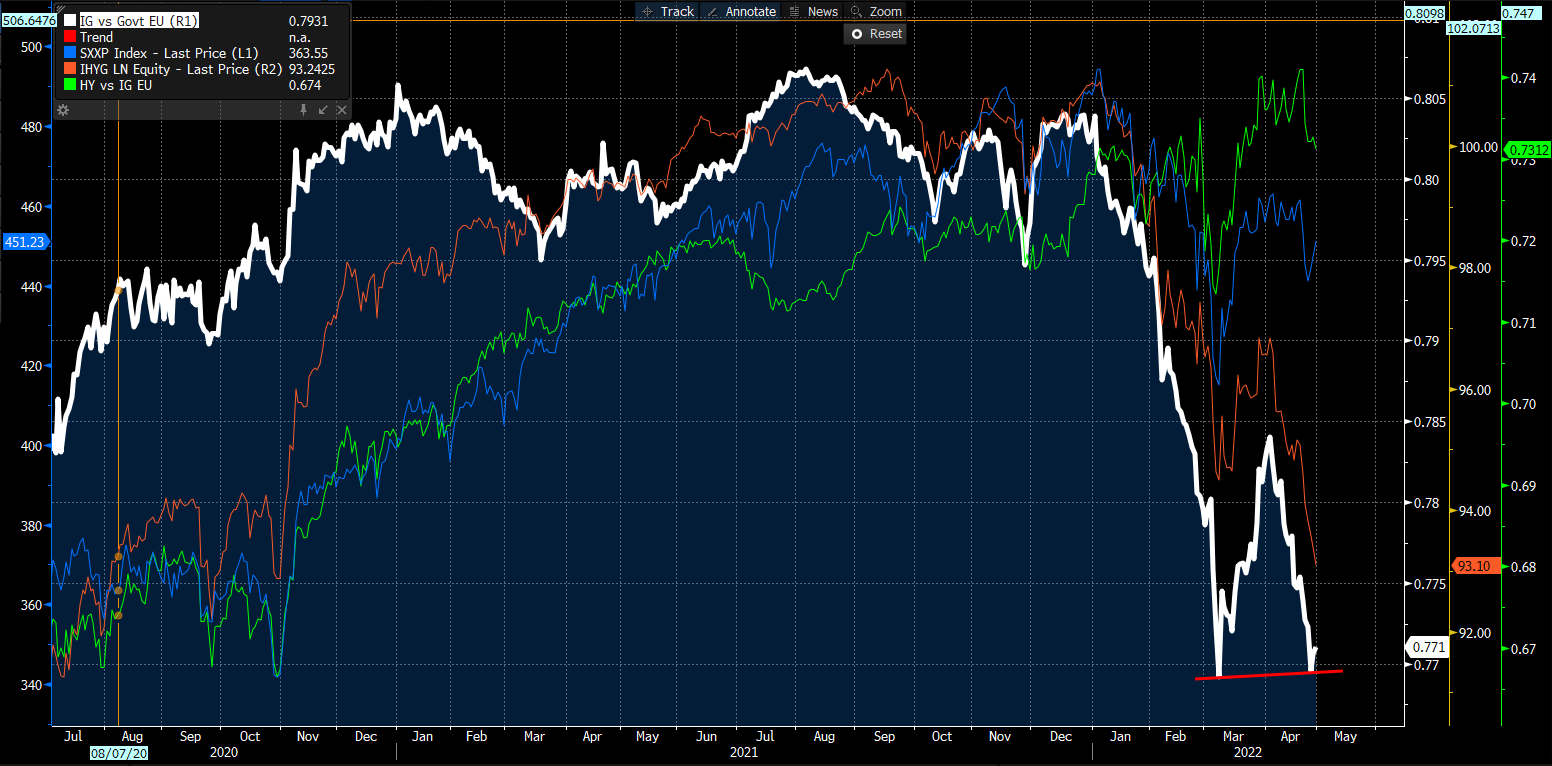

Looking at intermarket relations the IG to Govt ratio in Europe (in white) stabilezed while HY etf continued to going down. Also the HY/IG ratio (in green) topped and signals some problems ahead for equity and risky assets. The problem here is the impact of growth.

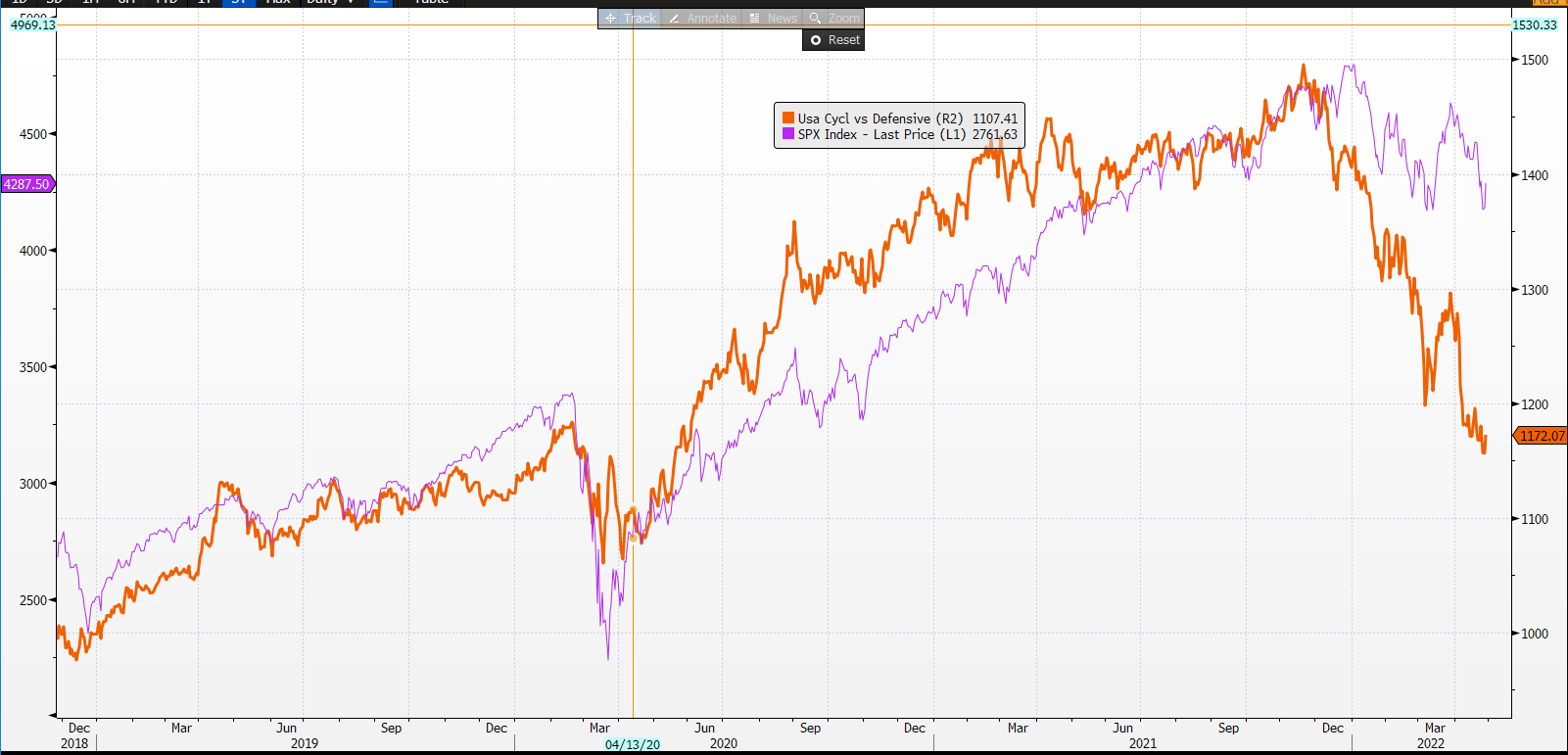

Equity/Internals: Near the peak of the equity cycle the sector leading is battled between energy/materials (the strongest sector until now) and defensives (staples, healthcare and utilities). Below the ratio of SPDR ETF and SPY. Staples is now the leading sector while energy and materials topped with lockdown fear in China.

By the way I expect that with some reopening and more stimulus we will view some new top on oil again given the limited supply environment. This will put, however, put pressure on disposable income and discretionary consumptions.

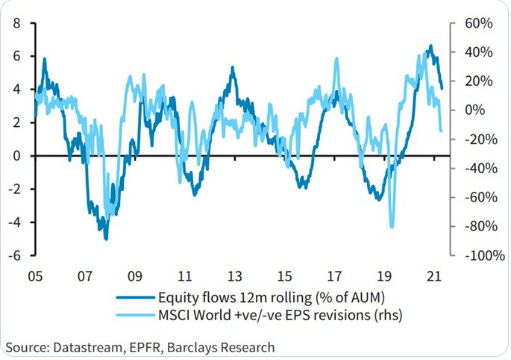

The breadth for SPX continue to be a bad omen here and given the bad fundamentals (macro + liquidity) people started to sell equity funds despite very negative sentiments. Last week I advised that sentiment could be a short term contrarian indicator but mid-long term its the trifecta (fundamentals + techicals + sentiment) that matters.

Commodities: driven by fear of an european embargo on oil, stop to gas and shortage of refined products the energy complex was the best sectors. Below the inventories related to crude, gasoline and distillate (diesel). Diesel that spiked and continue to have a strong backwardation curve.

The other subsector that remain hot is that one of agriculture. Wheat and Corn always related to Ukraine/Russia situation but also oilseeds. After pressure on sunflower oil (produced and exported in Ukraine) Indonesia halted the export of Palm oil with high pressure on all the sector.

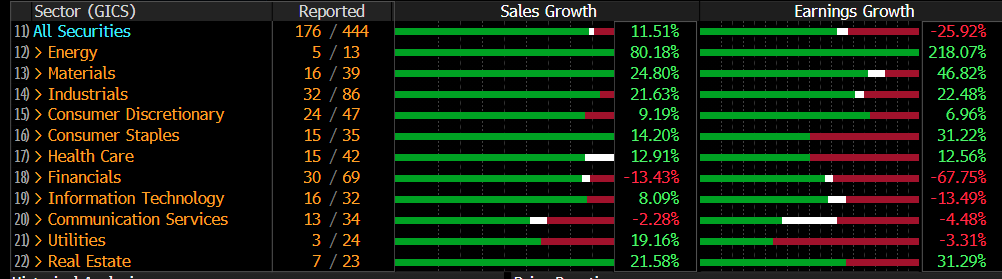

MICRO: In Europe we are almost in the middle of reporting season and it’s clear that the big driver of growth come from energy and materials name.

Glencore poised to an other strong trading year and the same for Bunge (the bigger agri trader). Syngenta (fertilizer producer) printed strong Q1 22 results, while name depending a lot on gas for productions like Ardagh showed a good revenue growth but price pressure on margins (especially in glass business).

Given the weak market context there is only a dispersion on downside with big losses suffered by:

ADJGR/ADLER after KPMG report spurs more questions like Caner’s influence, related deals, writedowns and disagreements on valuations;

CCAPGR (Corestate) after talks related to restructuring and further downgrade;

It’s all for today. I hope you liked and find usefull this. If the answer is yes subscribe and share it! Have a good weekend!

Great summary, thanks for sharing this stuff!