Weekly Credit Market Review - Apr 8

Weekly Credit Market Review - Apr 8

A thread from macro to micro

Welcome back to all! Before starting, a service communication. Next week there will be no weekly review as usual due to Easter holidays (I’ll be out 3/4 days). Now let’s go.

MACRO/NARRATIVE:

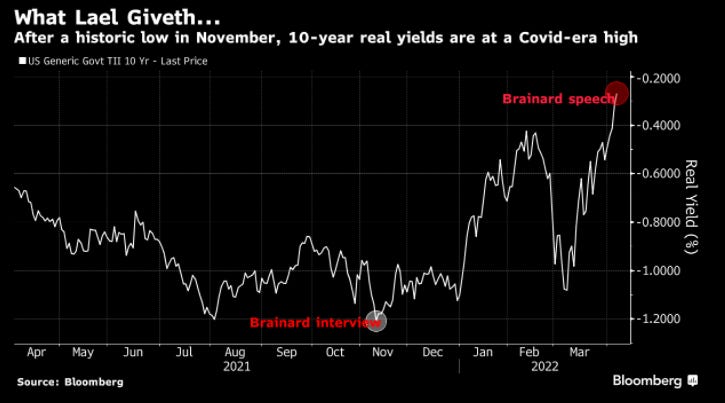

All the week newsflow was related to central banks actions and speech. At the beginning of the week Brainard (usually the most dovish at FED) started to prepare the FOMC minutes with a series of hawkish words:

“the Fed will continue tightening monetary policy methodically through a series of interest rate increases and by starting to reduce the balance sheet at a rapid pace as soon as our May meeting.”

“given the recovery has been stronger and faster,” the balance sheet will shrink much more quickly this time than when the Fed attempted quantitative tightening in 2017 and 2018. There will be “significantly larger caps and a much shorter period to phase in the maximum caps,” she said.

It’s clear that the main focus of FED at the moment is on inflation and that they are ready to eventually kill growth to reduce inflation.

The FED minutes of March were published this week too and they showed that officials would opted for a 50bp hike (without war). FOMC broadly agreed on monthly caps of about $60bn for Treasuries and $35bn for agency MBS (reducing size of 95bn at month). This is equals to 1.1trln dollar in 1 year. Below the total size of balance sheet (>8trln) to put these numbers in put in perspective.

To conclude with FED, always this week, Bullard said he favors 3-3.25% rates to blunt inflation.

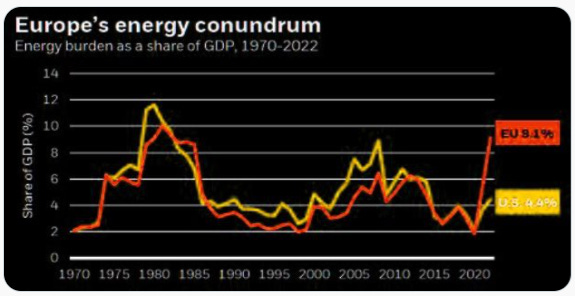

Passing at ECB the account of March 9-10 monetary policy meeting some members preferred to end APP net purchases during the summer to be ready to hike in September and December. They view the risk of strong impact on inflation expectation with a risk of wage spiral. On the argument I finded this chart on twitter without the indication of author (sorry but I can give him/her credit) showing the weight on GDP of the energy burden. Clearly the risk in Europe are higher on inflation and on growth too.

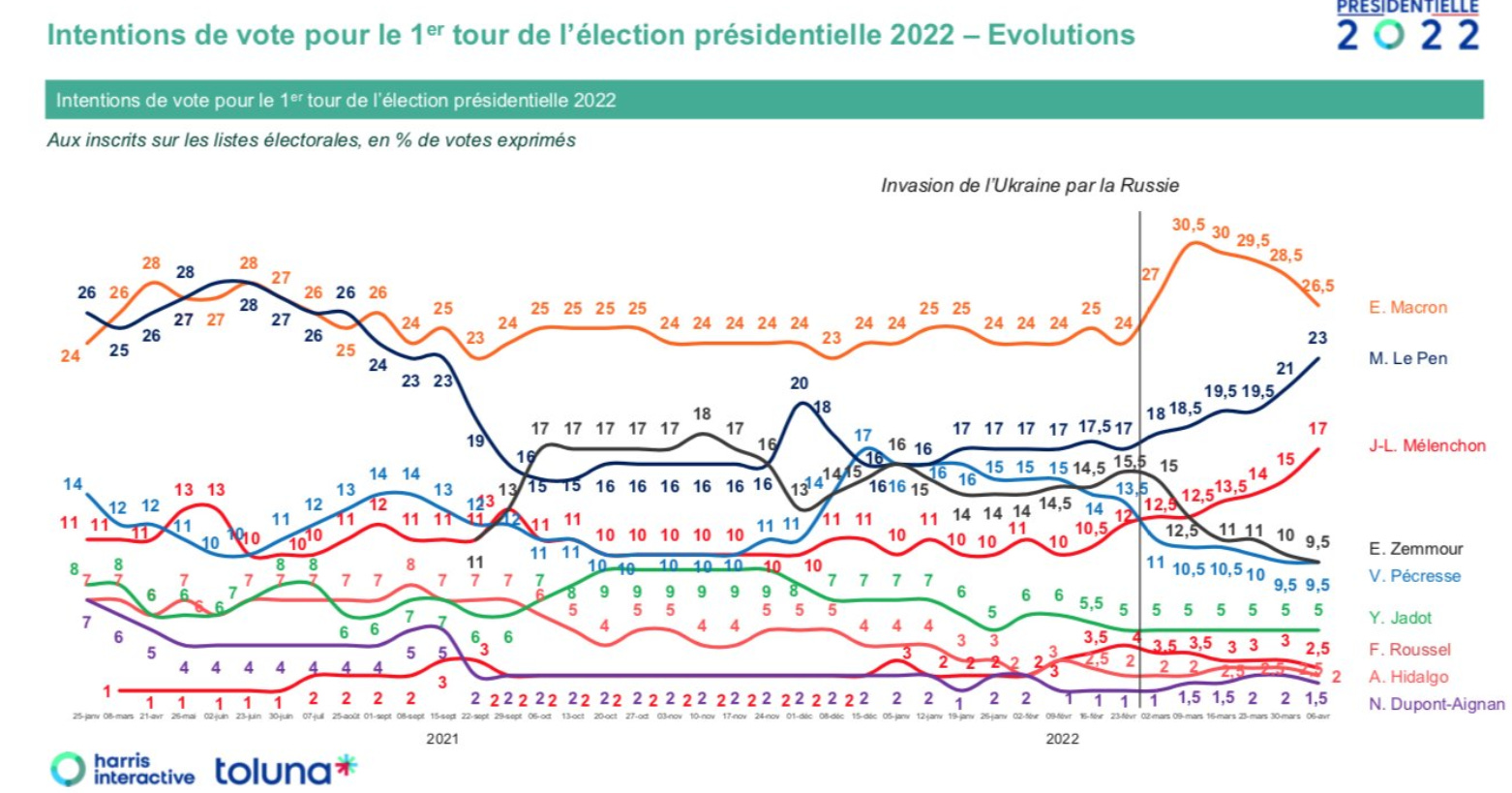

I conclude this section with some political risk. This sunday there will be the first round of french presidential election. The margin between Macron and Le Pen is very tight at first and second round (especially compared to 2017). Market started to price some risk on OAT vs Bund but I don’t think is prepared in case of a Le Pen win.

MARKETS:

This week I start from commodities: oil was penalized by oil strategic release we talked last week but some demand destruction started to appear on gasoline demand in US (given the high prices). China covid lockdowns did the rest. Nat Gas in US (Henry Hub) climbed to 6.5$ due to high demand for LNG from Europe and on concerns that Russian flows through key transit country Ukraine may be disrupted.

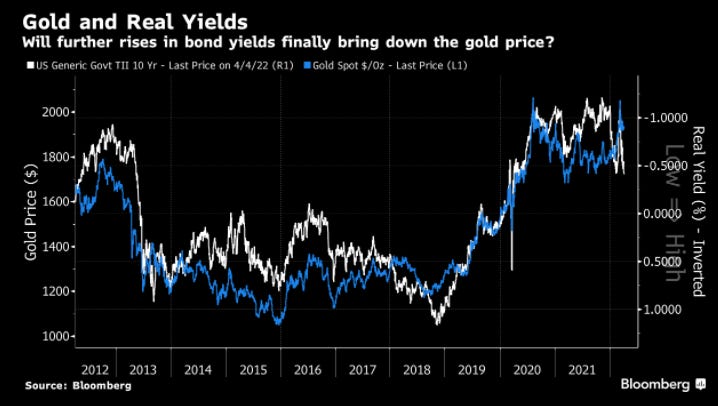

On government bond, rates continued the march up given the hawkish central bank rethoric to fight inflation. Real yield are now come back to pre-covid era but gold remained resilient breaking (for now) the usually correlation.

Equity markets were flat (SXXP +0.55%, SPX -0.6%) maybe due to the light positioning on equity and bearish sentiment (a lot of bad news are in the price).

But below the surface I like to look at intermarket signals. In US the IG/govt ratio put a top on the equity rebound for now (impacted by the high real rates - below in the panel).

Also the internal of the market speaks about a low growht or recession risk. A leading energy subsector is typical of late cycle expansion.

Here a series of internal famous ratio. All scream for growth risk. The real risk is when market leadership shift from energy to consumers staples (have a look at this).

Spreads in credit were generally stable this week given the Ukraine-Russia conflict that appears to have slowed geographically while there was no news on additional sanctions against Russia. Given the low supply cash tightened some basis point while some hedging activity put some pressure on CDS.

Using european ETF IG/govt ratio stopped to rise after the new increase of real rates (and the impact of financial condition) weighting on the total return of the HY etf. Also the XOVER/Main ratio drifter higher reflecting some growth risk.

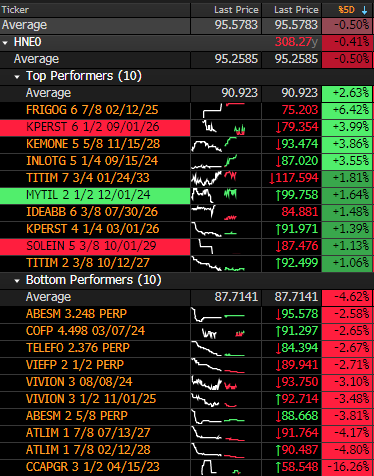

MICRO:

The loser league is full of ATLIM and related names (Abertis) given the interst by Blackstone on the company.

In the winners some words on KPERST that reported weak 4Q 21 results (EBITDA down 26% Yoy and net leverage increasing to 8.5x) but reassuring on the price pass throught to customers. Also FRIGO was up, but they will report next Wednesday (13 April)