Weekly Credit Market Review - Aug 12

Weekly Credit Market Review - Aug 12

A thread from macro to micro

Welcome back to all readers. I am returned from 2 weeks of holidays with my family. It was what I needed to clean-up my mind and my ideas.

As always if you like my job/analysis please subscribe below and share it and I remember you that I am also on twitter at @Credit_Junk.

And now let’s look at what happened this week.

MACRO/NARRATIVE:

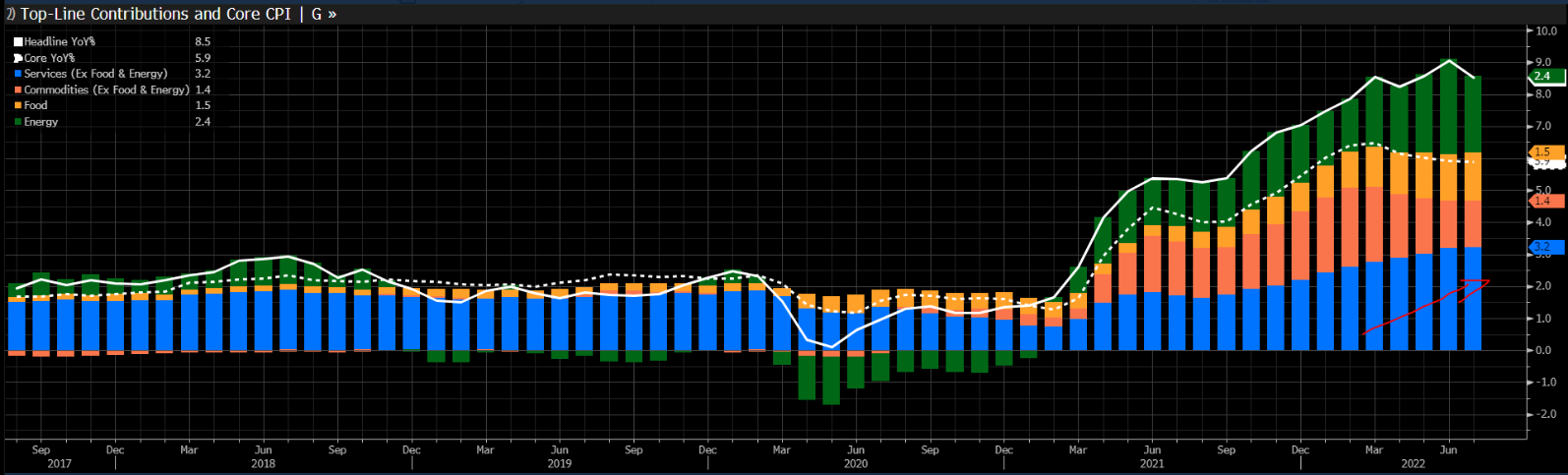

The most important event of the week (we did’t have a lot of events to be honest being in the middle of August) is for sure the CPI print in USA, followed by the PPI the day after. I wrote a lot about the headline numbers and the details. To sum up:

CPI YoY printed at 8.5% vs 9.1% last month (below expectatios);

CPI MoM was 0% (yes 0%, Biden talked about this);

CPI ex food and energy YoY was flat at 5.9% (below expectations)

CPI ex food and energy MoM declined to 0.3% from +0.7% (below expectations)

So the headline was clearly softer than expectations and confirmed that we could have seen the “peak” in inflation (for now) but some doubts remain and it’s to early to say victory on it.

In fact, while energy component declined (with the fall of oil, gasoline, etc) service YoY remained strong and are driven by wages by definition. We know that given the tightness of job market there is a pressure on wages (FED look at this) that pass on core goods and services, with the risk of remaining more persistent. The Atlanta FED indicator of “sticky” prices continue to rise for the moment.

Always looking at core inflation (with MoM) is up 0.3% the only strong dowside is given by airfares that by definition are volatile and with a lot of seasonality.

After the CPI data a series of Federal Reserve officials responded to softening inflation data by saying it doesn’t change the US central bank’s path toward even higher interest rates this year and next:

Kashkari says softer inflation data don’t change Fed’s path

Inflation has eased but it’s ‘unacceptably high,’ Evans says

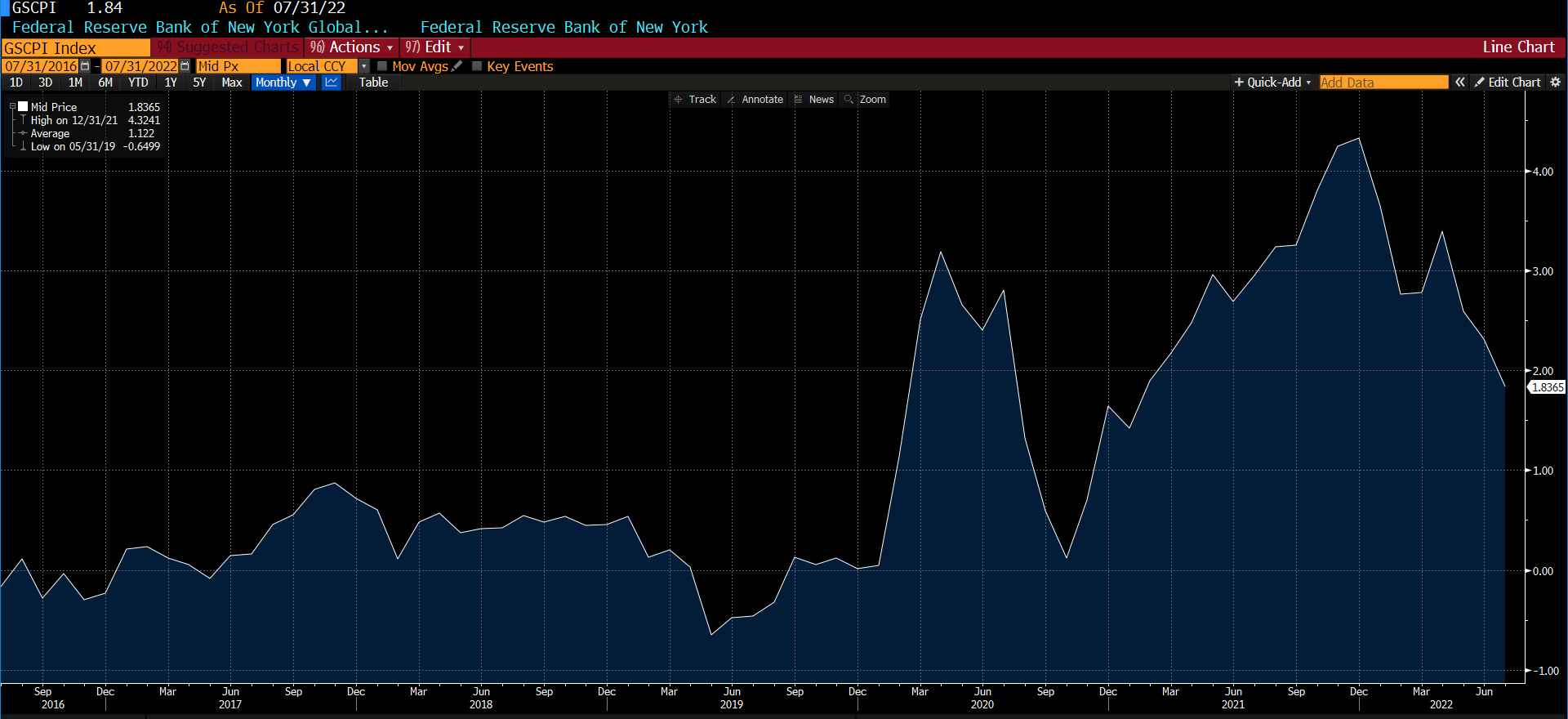

And passing to PPI, it confirmed some easing of price pressure, especially in the energy prices components but was broad-based thanks to the better supply-chain conditions.

MARKETS:

To speak about market reaction at the events of the week I choose to start with market pricing of the next FED meeting. While after the payroll probability of 75bp hike was sure, after the apparently softening of CPI the odds are now on a 50bp. In the meantime, before the next meeting we have an other job and inflation data, with the FED now more data-driven and no more giving us a forward guidance.

So market cheered this hoped less aggressive FED and in the fixed income space we had:

a steepening of yield curve driven by long end (bear steepening) with lower treasury prices (3 in the chart below)

higher breakeven at the long-end (less inflation now, more later)

the later was reinforced by higher commodities prices (1 in the chart below), that where reinforced in turn from lower dollar (2 in the chart below). The dollar was driven down by the less aggressive FED expectations.

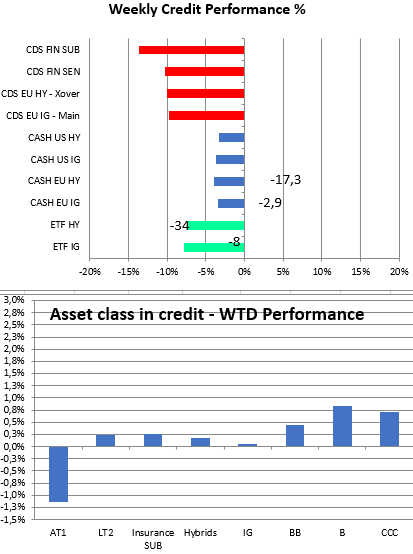

At the same time risky assets (above with the number 4 the ES1 US equity index) but it’s the same for credit spread, decoupled and recorded strong performance during the week with equity on average up 1.5% this week and almost 20% from the bottom. HY and IG spread tightened a lot, especially in the syntethic space where a lot of investor had their hedges (XOVER -47bp, Main -10bp this week).

If you didn’t it yet have a look at my last “educational” piece regarding credit allocation framework where I talked about a lot of interesting thing inside this market (like fundamentals, supply and positioning).

Regarding equity ES1 arrived at the 50% Fibonacci retracement this week, I remembered that in the past we saw also retracement of 66% before seeing new bottom.

Here the reason for rebound were a lot like:

the high negative sentiment and positioning too (especially CTA and hedge funds) that given the techical setup and the run low of the Vix jumped to cover their shorts (it’s for this that bear market rally are so strong)

The better than feared inflation data and economic data (with the rise in surprise index)

But partecipation in the rally. in the last leg was low, (below a chart of @alessiourban), pay attention. Risky market for the moment is a la-la-land environment (almost a reflation scenario) with financial condition better than at the beginning of FED hiking cycle. When market will wake up and FED will continue to hike the risk are higher, especially given the macroeconomic weakness remain.

MICRO:

Looking at single name in the looser land we have:

COFP - Casino that reported a mixed bag with good top line but lower margin across the various segments. Rising inflation and deterioration in consumers sentiment impacted the name here.

While looking at winner we have:

SHILN (SIG PLC) up 9% after strong results (strong revenue and return to positive FCF in H2)

TUICR (Tui Cruise) an other strong result with revenue for 3Q above estimates €4.43B, EST. EU4.3B, strong liquidity and summer booking at 90% of 2019 (good cross read for other leisure names)

TITIM (Telecom Italia) with the news that italian right party (Brothers of Italy) plan to take the company private to reduce debt

It’s all for today. If you enjoyed my job/analysis feel free to forward it to friends/colleague and remember to subscribe to the newsletter. Bye.