Weekly Credit Market Review - Feb 04

Weekly Credit Market Review - Feb 04

A thread from macro to micro

Welcome back. If I have to choose one world for this week price action, I’ll choose without doubt “volatile”. So to start:

MACRO/NARRATIVE:

This week the ball passed on the BOE and ECB central banks. BOE raised rate 25bp as expected but there were 4/9 of members voting for an increase of 50bp. On ECB Lagarde opened the door to a faster QE ending and a 2022 hike (the reference on unlikely hike this year was dropped out). March will be a live meeting to evaluate new forecast and to calibrate monetary policy.

Overall market was shocked by this hawkishness. What shocked me was the 180° change in some months. After several months claiming inflation was temporary now CB are in panic mode!!

But maybe the hawkisness of ECB and other central bank is gone too far.. Sentiment is bearish on rates (too much.. confirmed also by positioning that is very short) A very strong contrarian indicator is “The Economist” cover page.

MARKETS:

The reaction of the market was clearly negative on rates with movement over 2 sigma in some cases with trader increasing bets of rate hike at short ends.

Mr Curve (here the 5-30 european swap curve) say we are cooked, with an inversion signalling central banks to tighten into a recession!

While on commodities Dott. Copper don't confirm for now, with the ratio of copper to gold stable in the last 2 months. Energy sector continue to be strong with high demand and low supply coming to the market (inventories at cushing is always lower and lower). This week OPEC+ confirmed an increase of 400K barrel per day despite high demand (for me it’s an indicator of low capacity to increase production due to low spare capacity).

Equity market rebounded from the last week weakness and internal forces show a positive outlook (as Druckenmiller said: “Market is the best macroeconomist”).

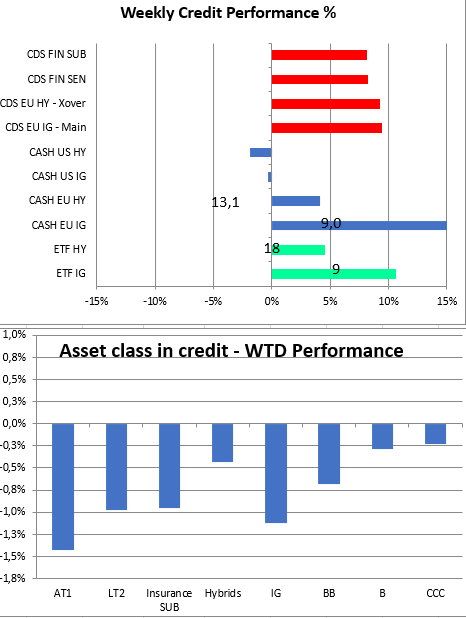

In credit market the week was very negative with no places to hide. Spread widened in IG and in HY too. By asset class IG suffered from rates and spread movement, while high beta bonds were impacted too.

I like looking at intermarket signals too. In credit the IG to govt ratio decreased (in line with weakness in equity last week) but the ratio between HY and IG diverged, remaining stable, thanks also to a low level of supply entering in the european reporting season.

MICRO:

No place to hide here (I said it before). Just to do an example today the ETF HY is dow 1% at least.

So I’ll talk only of looser. The focus is on:

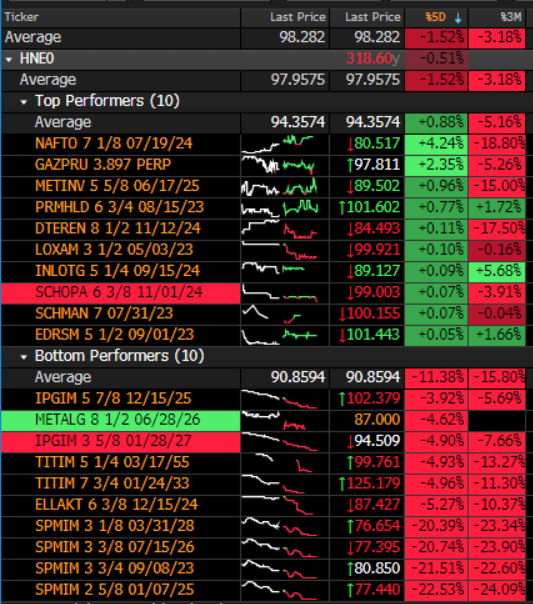

SAIPEM: last week the guidance was cut and also the backlog. The high cost of materials and trasportation will weight a lot on the projects and there will be a loss of 1/3 of capital. Shareholders (ENI and CDP) are talking about a capital increase of 1,5-2bln at least and there are talking to waive some covenants from an undrawn credit line to be able to pay the short term maturities. Just to make an example the 04/22 bond trade below 90 now for fear of cross default on the credit line.

ORPEA/KORIAN: the scandal on the retirement homes extended also to Korian with weakness in equity and bond too. The government announced the start of investigation.

For this week it’s all! I hope the next one will be better than this one.

Have a great weekend guys.