Weekly Credit Market Review - Feb 11

Weekly Credit Market Review - Feb 11

A thread from macro to micro

Welcome back after this very volatile week in the market. So step-up immediately and look at what happened.

MACRO:

As I posted during the week the focus of all was on CPI in United States. Like said in the song ““if inflation’s too high, people are gonna cry”.

CPI YoY come out at 7.5% (vs expectation at 7.3%) while CPI core printed at 6% increasing from 5.5%.

The increse was as usual on energy and goods (that benefited most from pandemic and lockdown).

In Europe, after a very hawkish ECB meeting last week, some members tried to calm the market. Also Christine Lagarde yesterday affirmed that tightening a lot could harm economic rebound and that excessive rated increases not solve all the problems.

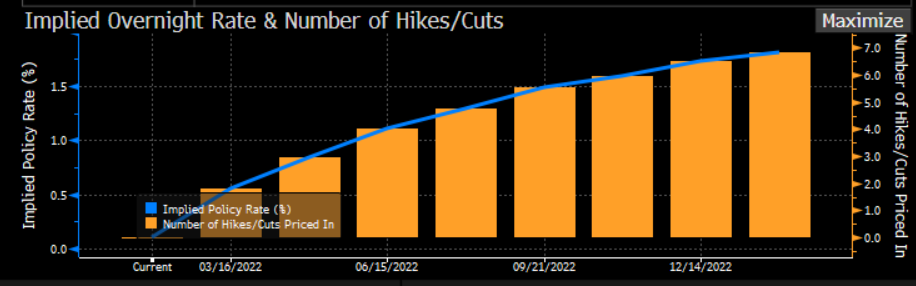

But the genius is out of the lamp yet and money market (thanks also to high CPI in USA) now price 6 hike by the FED in 2022. Bullard support also two 50bp hike before july.

MARKET:

Hawkish central bank = high rates usually. And this was the name of the game this week. Front end of DM curve were impacted by rate increases bet, while curve (usually on long term) continued the flattening move (with fear of policy error).

Looking at commodities from an intermarket point of view, despite Mr Curve flattening, Dr Copper continue to price a good macro environment thanks to a credit impulse in China that returned to growth.

Gold was resilient despite a high level of real rate (inverted in the chart below) while in energy sector we have stable oil after EIA report that showed a decline of 4.7mln bbls of reserves (the largest one since last year), similar for gasoline.

Nat gas, in the meantime, tumbled after a warmer weather outlook.

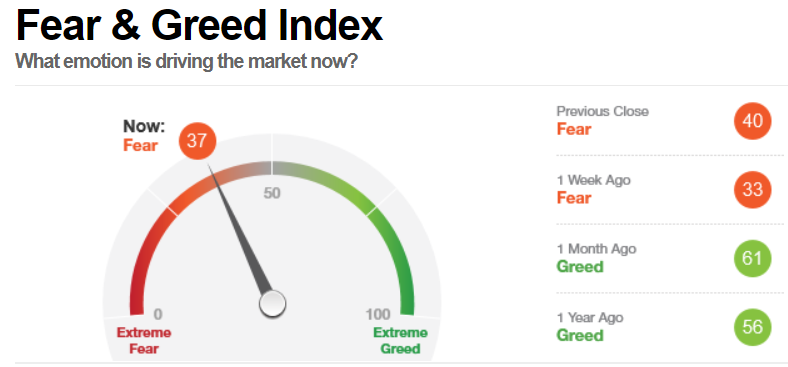

Equity in DM close the week stable (SPX and SXXP) where we have also a normalization of volatility. We have reached in the past very high level of negative sentiment. Emerging market index was support by the chinese credit impulse and by the news that “CHINA STATE FUNDS” said to buy stock to slow market decline.

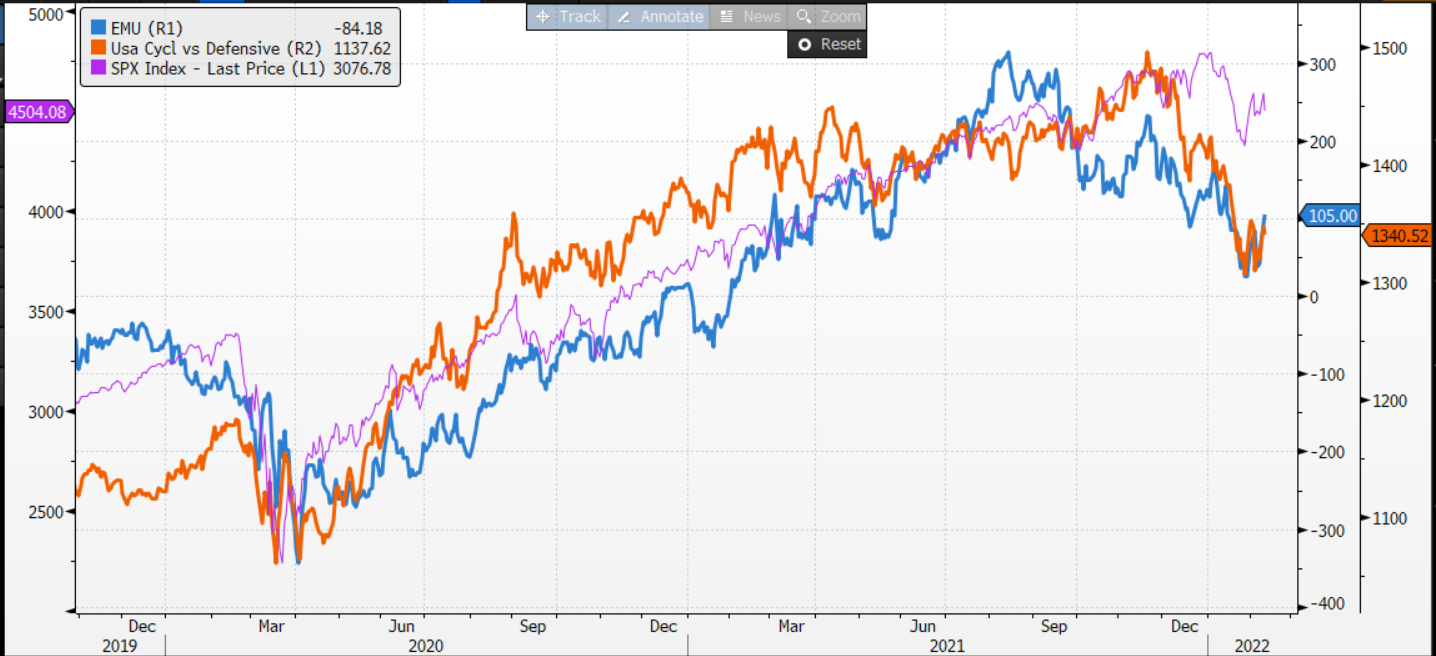

Looking at cyclical vs defensive, this ratio follow the fear of Mr Curve (with the sector most exposed to growth declining the most).

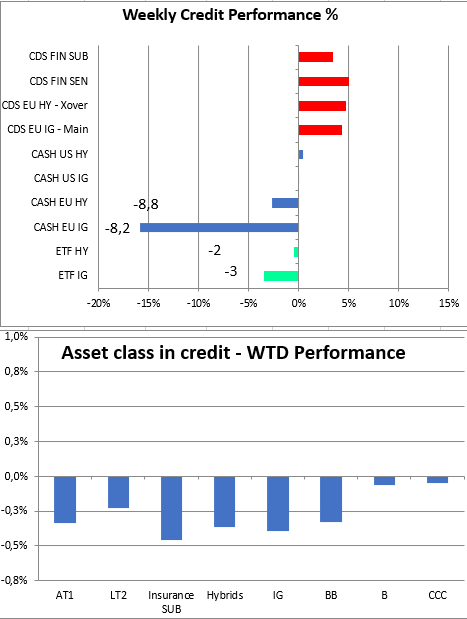

In credit we saw strong outflow from IG and HY funds in euro credit. For both the impact of rates increase and of volatility impacted on total return and we know that flows follow performance usually.

The week started with some stabilization of spread that, despite widening again today, closed with some tightening.

Total return continue to remain negative in this environment while looking at ratio of different part of bond market (IG to Govt ratio) followed the rate increase while (HY to IG ratio) remain stable not following what said by the cyclical-defensive ratio of stocks. Below the ratio are calculated using ETF.

In a past thread on twitter I looked at what happened in past cycle of tightening cycle of central banks.

MICRO:

This week credit remained driven by macro (rates and risk aversion) but there was some single name volatility too driven by specific newsflow.

SAIPEM: after huge loss related to profit warning (and need of capital increase) curve remained under pressure due to fear of some restructuring before the maturity of the 2022 short term bond. Some positive newflow appeared in the week thanks to some headline

”According to Messaggero, Saipem is in talks with banks including Intesa and UniCredit, for a €500m bridge loan to repay the upcoming 2.750% Apr-2022 bond”

While not visible in price action there was some newsflow in TMT HY with Iliad trying to bid for Vodafone italian activity at 11bln value (Vodafone rejected the approach). In Italy government said to consider KKR Bid for Telecom Italia as too low, while in Spain Masmovil and Orange continue to talk about a consolidation with a 50/50 JV.

Primary remain low, with a big pick-up expected next week after the end of reporting season. There is a trend emerging from US of switch from fixed to FRN. We saw some of this also this week with Cerved dual tranche (fixed and FRN) and Anacap but that due to volatility postponed the deal.

It’s all for today. Have a great weekend. Stay safe!!