Weekly Credit Market Review - Feb 18

Weekly Credit Market Review - Feb 18

A thread from macro to micro

Welcome back again! It was an other volatile market characterized by too much noise. So let’s go to see what happened.

MACRO/NARRATIVE:

From this week to help me to be more more methodical I will add this words cloud that I made using https://www.wordclouds.com/ while based on all the news of the last week of Bloomberg Market Wrap (the daily summary).

Clearly the two most important driver were:

the FED minutes for January meeting that showed FED will be more aggressive in the hiking cycle than last time thanks to a stronger outlook for growth and strong job market. They could start to sell bond also before than planned. Despite this market thinked it was dovish than expected due to the fact that there was no reference to 50bp hike in March. This for me is due to the fact that the high CPI print was not available at that meeting. Now for markets, the prospect of 50bps in March are now at 43%, while that was over 100% last week. (Graph below of Fred Goodwin - Mr Risk)

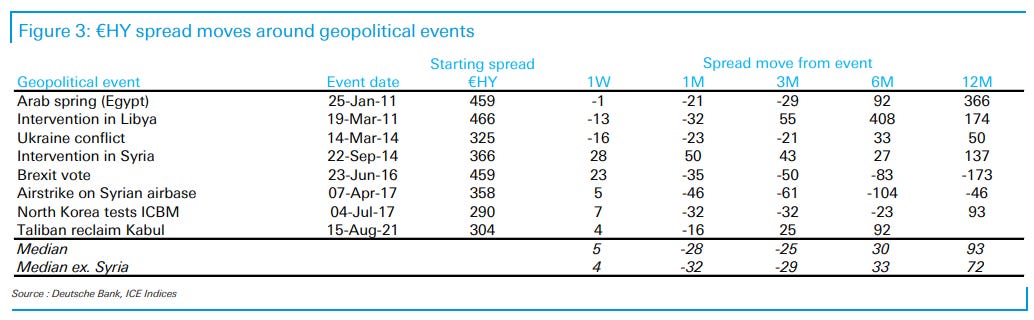

The geopolitical situation in Ukraine. The situation is not easy there. Russia don’t want NATO close to the border and try to weaponize gas and oil to have a deal on the North Stream 2, while United States don’t want to loose grip on Europe. I can add more but newsflow is chaotic. Situation is deteriorating every day with 170-190k russian troops ammassed near the Ukraine border. What I can say is that I finded this interesting study on HY made by DB that compared past geopolitical events. What happened? In the immediate first week after the event spreads are very modestly wider however on a one-month and three-month basis, spreads are generally around 30bps tighter.

MARKETS:

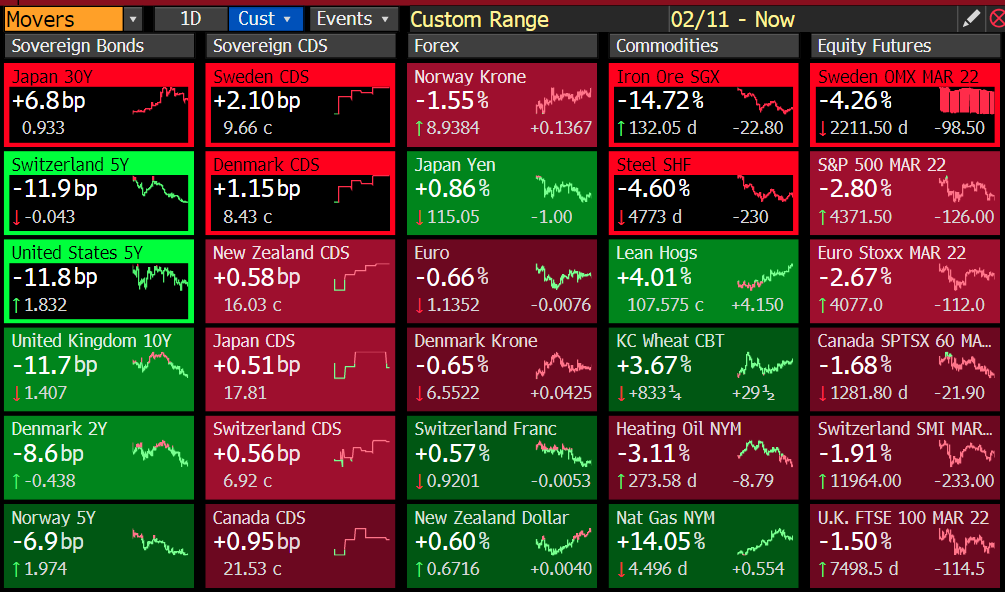

Risky asset suffered a lot this week due to this doble negative catalist (low global liquidity and high geopolitical risk). Equity (S&P and Eurostoxx) is down 3% this week and looking at the ratio IG to Govt (a good proxy of liquidity tightening) there is a lot of downside here. And technicals here doesn’t help with ES future below the 200 days moving average.

Bonds market bearish momentum has decelerated due to continued Ukraine/Russia tensions with some priced hike by central banks now out of the table.

In commodities agriculture products (like wheat and corn) continued to be impacted by the same drivers with Russia and Ukraine two of the bigger producers countries, while the biggest movers this week is “Iron Ore”, where China started to cool speculation to limit prices. After the end of Winter Olympics steel production is expected to return.

MICRO:

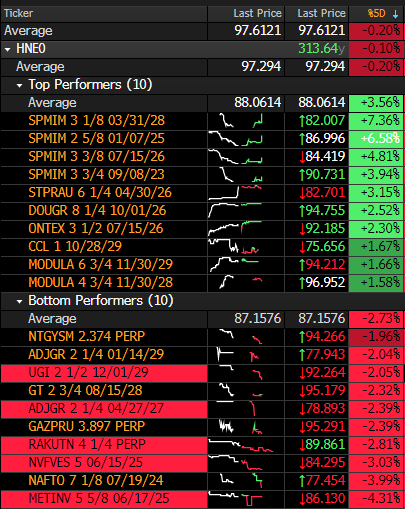

SPMIM (Saipem) remain the most volatile name after this week announced 2bln capital increase and 1bln drilling sale. Today ENI CEO said that they will support SAIPEM along with CDP (the other shareholder). Below the 1 week chart. Who say that bond are boring?

Looking at looser I see two Ukraine names (NAFTO and METINV) while:

NVFVES (Novafives) was under pressure after a Moody’s outlook change and a memo of “Everest Research” focused on M&A and refinancing risk.

RAKUTN reported a weak FY21 with mobile growth remaining sluggish

It’s all for this week, enjoy the weekend hoping a descalation in Ukraine.

Thanks for this. Just an intern question: how do you compute the IG to Govt ratio?