Weekly Credit Market Review - Feb 25

Weekly Credit Market Review - Feb 25

A thread from macro to micro

Welcome back at our classical review of market as usual from macro (the big driver and the big asset class) to micro (credit, my bread and butter).

MACRO/NARRATIVE:

Looking again at “Bloomberg Markets Wrap” (the daily summary) the main focus is clearly on Ukraine and Russia.

The escalation was fast and very strong from Russia and Putin. Initially there was a declaration of independence by the two provinces of Donetsk and Luhansk. These culminated in the decision by Russia to launch a full-scale invasion of Ukraine on Thursday.

The reaction of US, UK and EU is now on sactions on Russia, but the most drastic solutions are now excluded (no exclusion of Russia from SWIFT and no oil/gas ban). Situation remain fluid and there is a lot of news out (true or not) like an headline saying: “RUSSIA ready to send delegation to MINSK for talks”.

On central banks, FED confirmed to go ahead with his plan to exit from extraordinary stimulus while for ECB Holzmann said that risks from war in Ukraine can delays stimulus exit.

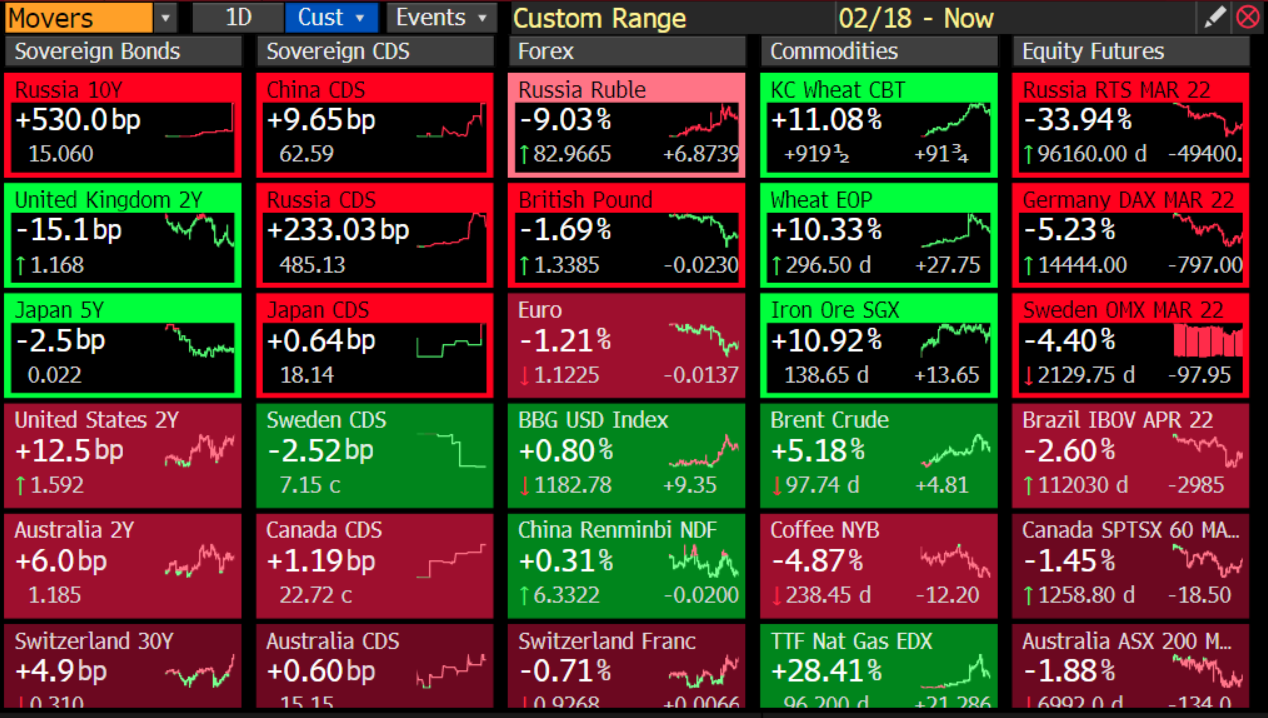

MARKETS:

Risky asset (like equity and HY) suffered again this week, but very bearish sentiment and some headline (like that one of Russia ready to talk) created some rebounding starting from yesterday. Russia stock market crashed amid sanctions of west while the asset class gaining the most was agriculture products.

Wheat and Corn spiked on the news of Russian invasion of Ukraine. The two countries are key suppliers of the region, and the attack appears likely to upend global trade flows. Rally paused after some positive news and on inflation concerns.

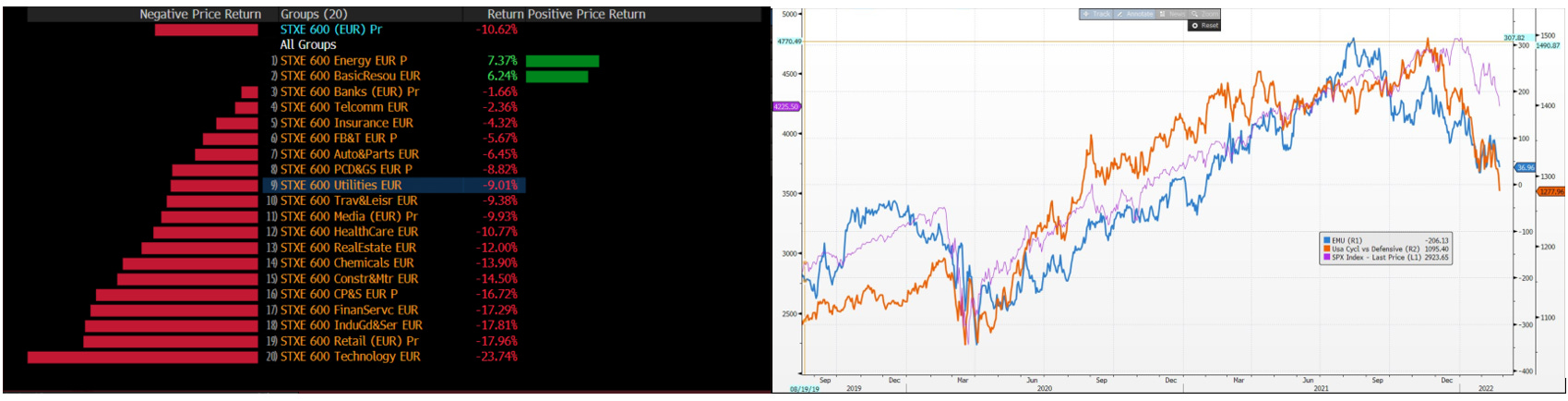

Regarding equity YTD only Energy and Materials stocks are up, while EU and US cyclical/Defensive ratio is down. “Market is the best economist”.

This to me is a stagflation problem and for FED tightening (and reducing liquidity) in this environment will not be an easy task.

In the bond market interest rate remained muted amid the high geopolitical risk but looking below the level of the sea we can see a confirmation of stagflation fear (with lower real rate and high breakeven). High inflation fear arrive from the high level of all commodities (energy, food and metal) and the fear of supply problems after the start of the war.

Credit was weak again with a widening in cash both in IG and HY while the positive newsflow out give the CDS a boost to close the week tighter. XOVER today is tighter 40bp. But before being to greedy I want to see a stabilization of the IG to govt ratio (the credit is in fact the canary in the coal mine).

Until now credit suffered also from the liquidity tightening fear of central banks while showing also a growh fear. In fact this month XOVER to MAIN ratio (applying a 5x adjustement to IG) continued to decompress.

MICRO:

And finally we arrive at the winner and loser of the week.

On the winner league we find:

ADJGR and ADLERR bonds. These bond are very volatile and pass up and down week by week due to continue newsflow;

SAIPEM: this week reporting confirmed 900M euros of loss for Q4 (1/2 of equity value) but Eni and CDP continued to support company (for now only with talks).

The big losers are:

name linked to Ukraine and Russia like GAZPROM but also NAFTO (Ukraine gas company) and METINV (with sanctions applied on the securities);

Wintershall DEA (WNTRDE) after the expected stop of approvement of Northsteam 2 (the company is one of five companies to have lent money to Russia’s Gazprom for the project, alongside Shell, Germany’s Uniper, France’s Engie and Austria’s OMV)

SBBBSS: after a short position piece of VICEROY that you can find in the link below

https://viceroyresearch.org/2022/02/21/samhallsbyggnadsbolaget-hard-to-pronounce-harder-to-justify-value/

It’s all for this week. Have a nice weekend.