Weekly Credit Market Review - Jul 01

Weekly Credit Market Review - Jul 01

A thread from macro to micro

Welcome back after a weekend at the seaside for me and my family. I needed that. As always if you like my job/analysis please subscribe below and share it. Now let’s go to see what happened.

MACRO/NARRATIVE:

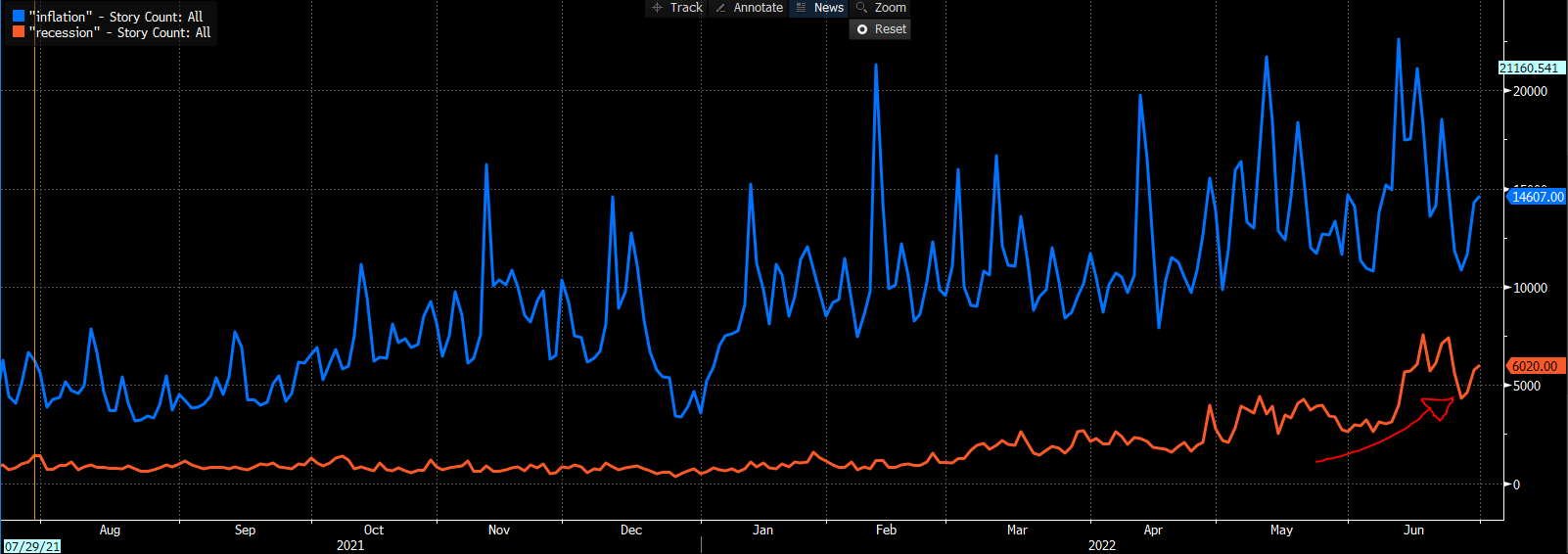

This week continued the battle between inflation and growth. I like to see at the “google trend” of both to see if there is crowdness in some part of the market or on a narrative. Overall number of story is always greater for inflation, but the trend is changing.

Regarding inflation in Europe we had the print of June estimates. For now it's a preliminary data and we know only:

- Core: from 3.76% to 3.74% (rounded number says from 3.8% to 3.7%)

- Energy: from 39.1% to 41.9%

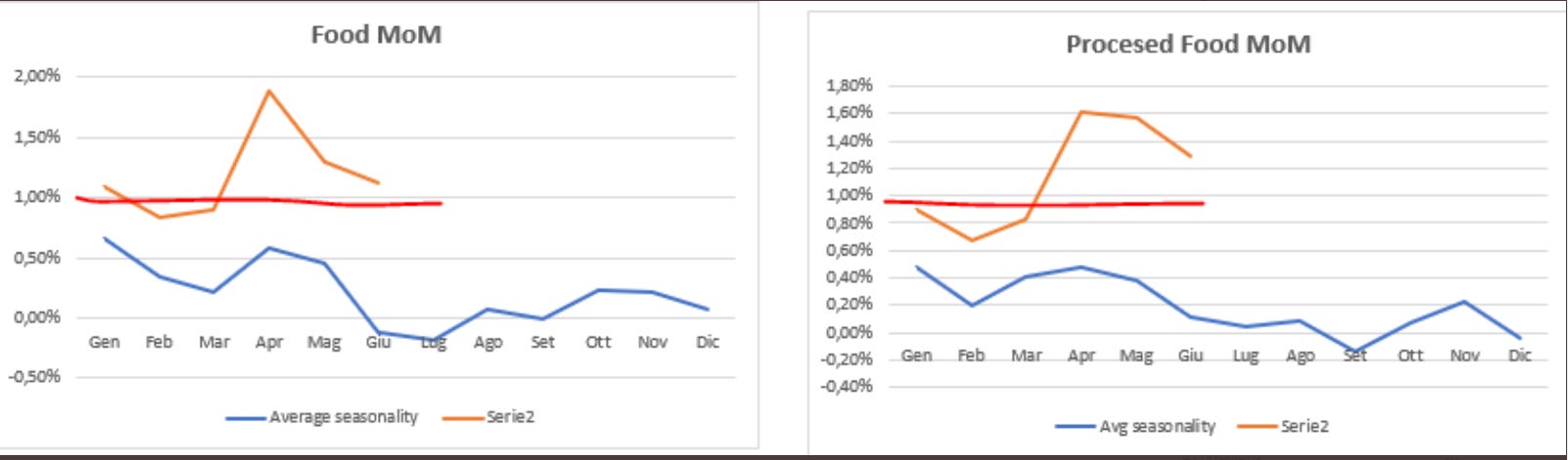

- Food: from 7.5% to 8.9% (processed from 7% to 8.2%, unprocessed from 9% to 11.1%)

What is more worryingly for me is the MoM in food (but processed and unprocessed) that remain constantly above 1%.

Always this week we had the Sintra symposium of central bankers. Here global central bankers warned that inflation is here to stay (both Lagarde and Powell said the same). This confirm that between recession and price stability, for now, they prefer to defend the latter, acting fast and increasing rates. On this point I’ll add that:

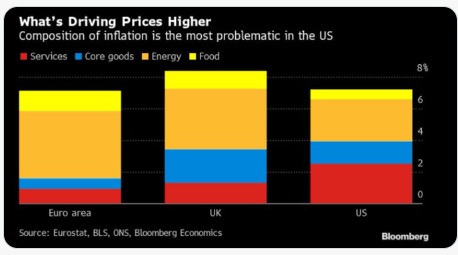

Euro inflation is almost driven by energy/food (so supply driven) --> ECB can't do a lot

US inflation is driven by services/goods --> FED can reduce aggregate demand and have a chance on it

—> Two type of inflation - two responses needed

Regarding growth this week macro data were not so supportive, with an associated strong down-shift in surprise index. The only place with positive data is China, where both manufacturing and services PMI rebounded thanks to a better health situation and a pick-up in services spending.

MARKETS:

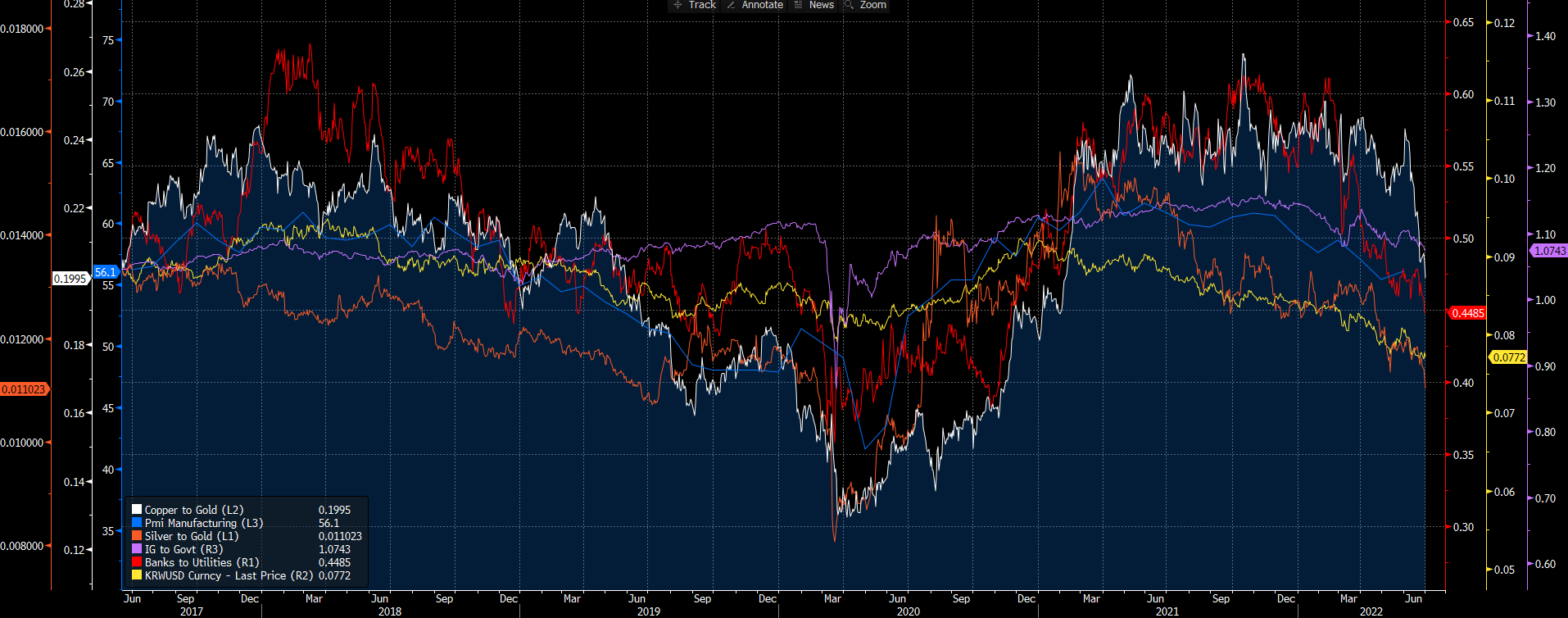

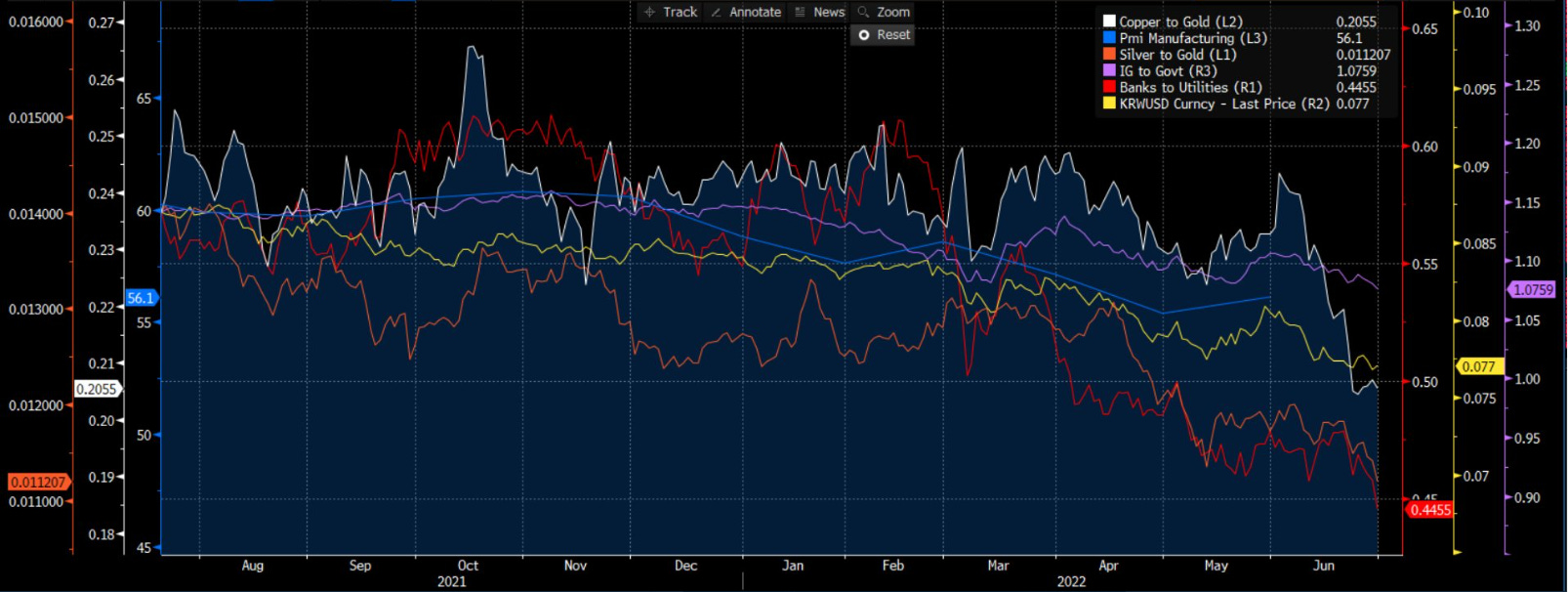

Given what I said above the market responded accordingly. I am a strongly believer in intermarket analysis and you can’t trade one without looking at what happen in other. I created a chart that I love to call “All-in-1” or “The chart of charts” putting all together.

I thinks also there is hierarchy in the market with some smarter and forward looking than others:

Here in the top chart the mid-term chart and below the YTD one. Given we passed the end of the month (of the quater and of the semester too) I looked at what happened here starting from metal and going down:

Copper/Gold and Silver/Gold accellerated down, driven especially by the copper (the doctor that spotted most of the past recession)

Won (Korean Won) was weak too. Here it’s most driven by less aggressive stance by central bank vs FED but also by the less positive growth environment with Won particulary sensitive

Rates market (not covered in the chart, but following the trend of copper/gold) performed well, with a bottom in bond prices driven by a reduction in rates increase by central banks priced in terminal rate

IG/Govt down, an indicator of liquidity tightening that put pressure also on HY and equity (risky asset in general);

Banks/Utilities it’s one of the most used internal market indicator and indicate a defensive positioning.

All of this confirm a shift away from “inflation” to an “economic problem”.

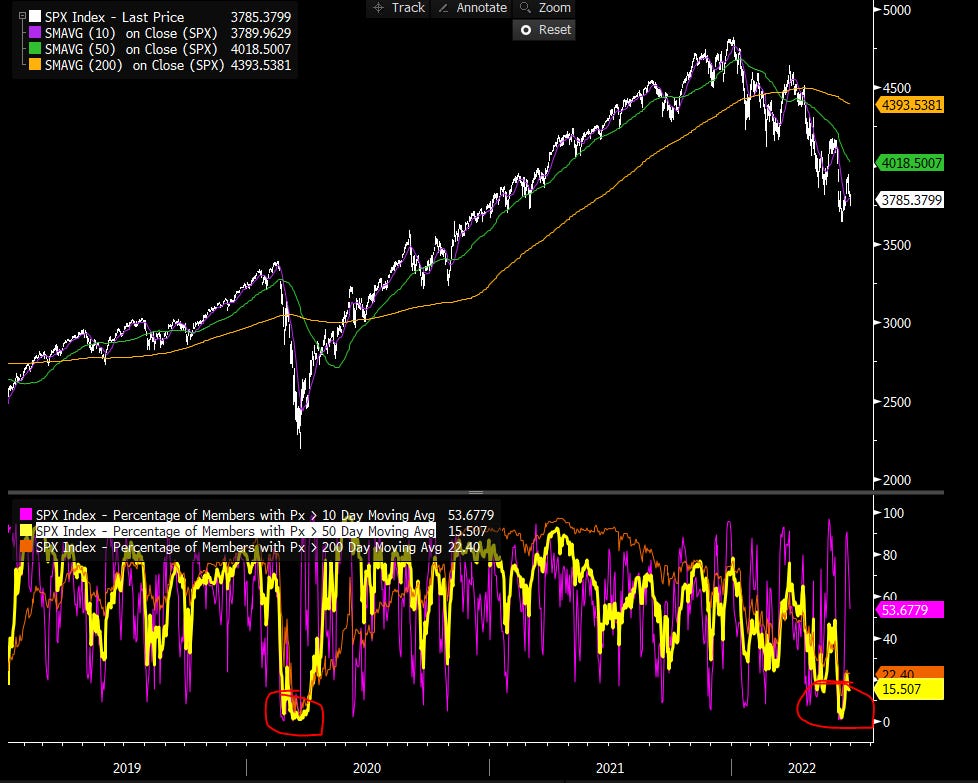

And to conclude, while it’s true that technicals are starting to appear intenteresting from a contrarian approach, with sentiment very depressed and breadth (below numbers of name above moving average) near a capitulation level…

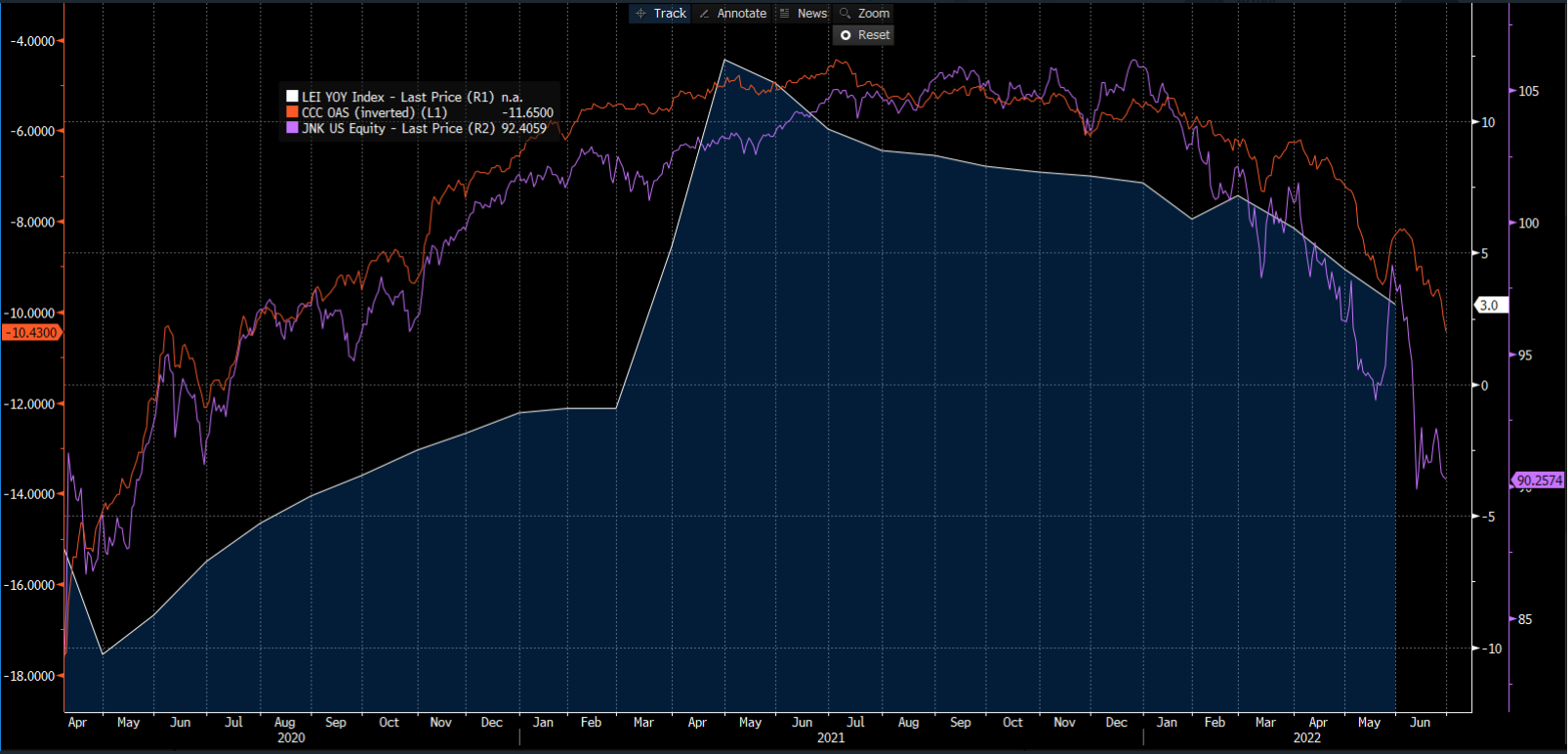

..liquidity, the most important driver continue to go down and is not good for risky assets:

- JNK (HY ETF) new low

- CCC spreads in USA a 1043bp

In credit markets IG and HY widened 20 and 60bp respectively but the change in narrative was visibile in the credit spread widening but with bund yield dropping, driven by risk-off.

While it seems a bottom in the IG/govt ratio was reached (we were here several times this year) pricing a sufficient recession risk, HY market (below the HY/IG ratio) do not yet in my opinion, preferring always BBB and BB rated names.

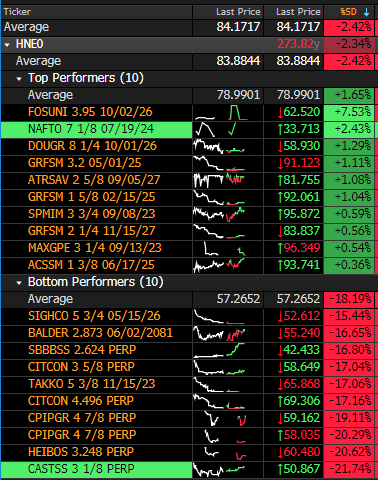

MICRO:

On a single name I have a lot to say this week. Performance speaks itself.

The big loosers are hybrids related to real estate sector, after the never ending story of Viceroy short on same names of the sector.

A big loss also for TAKKO a problematic retailers of which we talked a lot with my friend (@KillinGswitCH98 and @CavaggioniMario) on twitter.

Some positive news come on Grifols this week with some rumours of a capital increase (that caused a spike up in bonds prices) but denied by the board.

Have a great weekend, relax"!

As always if you liked it, share it!