Weekly Credit Market Review - Jul 08

Weekly Credit Market Review - Jul 08

A thread from macro to micro

Welcome back. As always if you like my job/analysis please subscribe below and share it. Now let’s go to see what happened this week, there is a lot to talk about.

MACRO/NARRATIVE:

The market continue to be driven by the pendulum between two narattive (recession vs inflation). As we know, market is able to think just 2 or 3 stories each time. The main events/macro data of the week were:

FED Minutes (and ECB minutes too): nothing new from FED. There was a continued focus on inflation, that could be higher than expected (and persistent), so there is the possibility of a even more restrictive policy (with a 75bp also in July. For ECB, too, could be ready to follow FED with more aggressive hike (and 50bp always on table);

US macro data this week confirmed the FED view (despite most commented that the comment was based on old data) with better than expected ISM services and a strong payroll (increase 372K, vs 265k expected). This for sure give the FED a greenlight for their planned frontloading hike cycle;

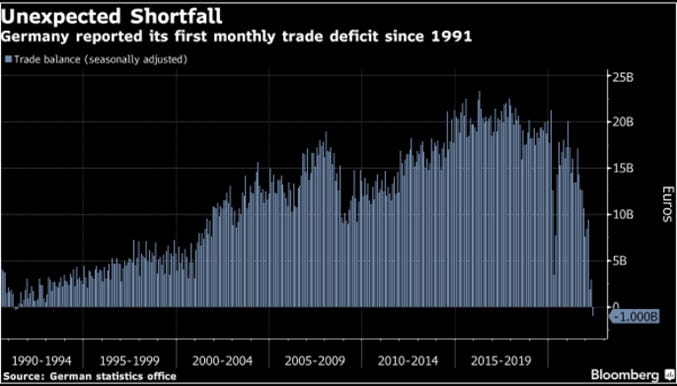

In Europe the situation is different given the strong import of commodities from abroad and the gas crisis. Germany had the first monthly trade deficit since 1991 (this is the great driver of EUR weakness). Always this week Scholtz signed the bailout for gas giant Uniper (impacted by the high cost of the raw material) while next week from 11th of July there will be a stop of flow on Nordstream1 for 10 days (officiallyfon only 10 days.. and after that?);

Consumer’s inflation is at the center of the Biden agenda so had some talk to reduce some tariffs from China. At the sime time China (whre there is the great % of refining spare capacity) increased export quota of gasoline/diesel and jetfuel by 5M tons to 22.5M tons totally;

In Uk Boris Johnson quitted as UK prime minister, dragged down by scandals and lack of support by government members.

MARKETS:

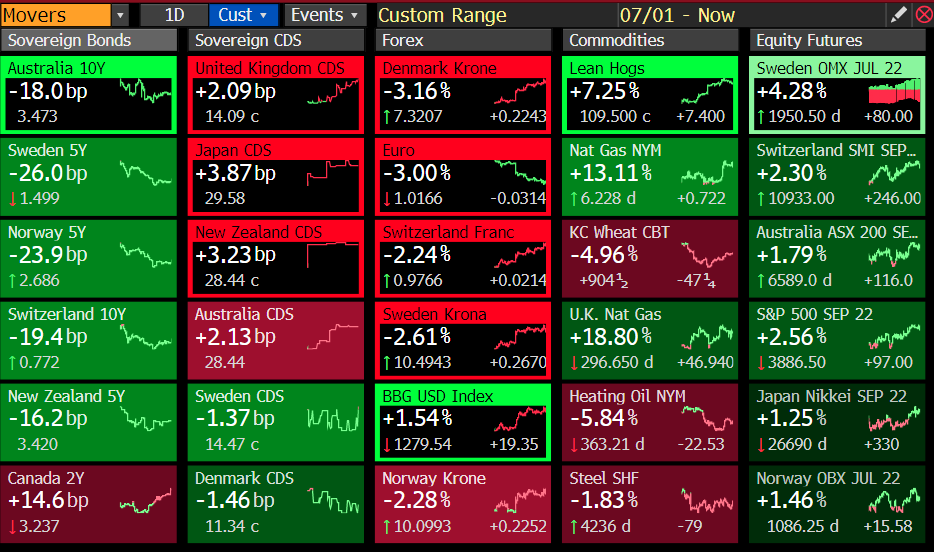

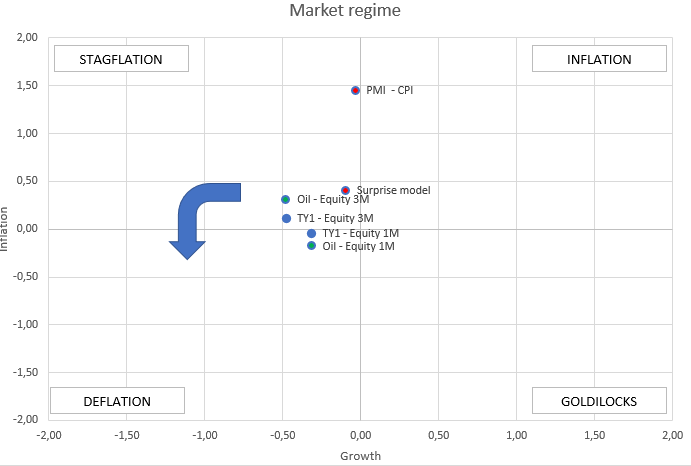

The biggest mover of the week from a macro point of view is for sure the dollar (king dollar) given that we are on the cusp between stagflation and deflation but I want to analyze what happened also at other asset class.

→ Commodities: all the subsectors were impacted by growth fear and liquidation (with a very low open interest on the main futures). In agriculture the wheat returned at pre-Ukraine invasion. In Industrial metals dr. Copper arrived at -26% YTD and also oil succumbed at the main narrative despite a tight phisical market. Gas in Europe remained high due to Russia pressures on Europe and the fear of a strike in Norway;

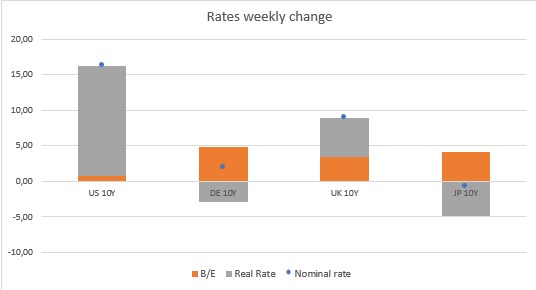

→ Rates: due to the better than expected macro data in USA and the hawkish FED the rates in US returned to growth (with some of the hike returned in the forwards), driven by high real rates. In Germany/Europe remained stable due to high risks of gas cut by Russia and the possibile impact on growth. Always looking at the drivers of US 10y we can see that copper/gold bounced a bit (thanks to newsflow of infrastracture stimulus in China), despite indicating a lower treasury yield target, while YTD rates are following more oil and oil/golds.

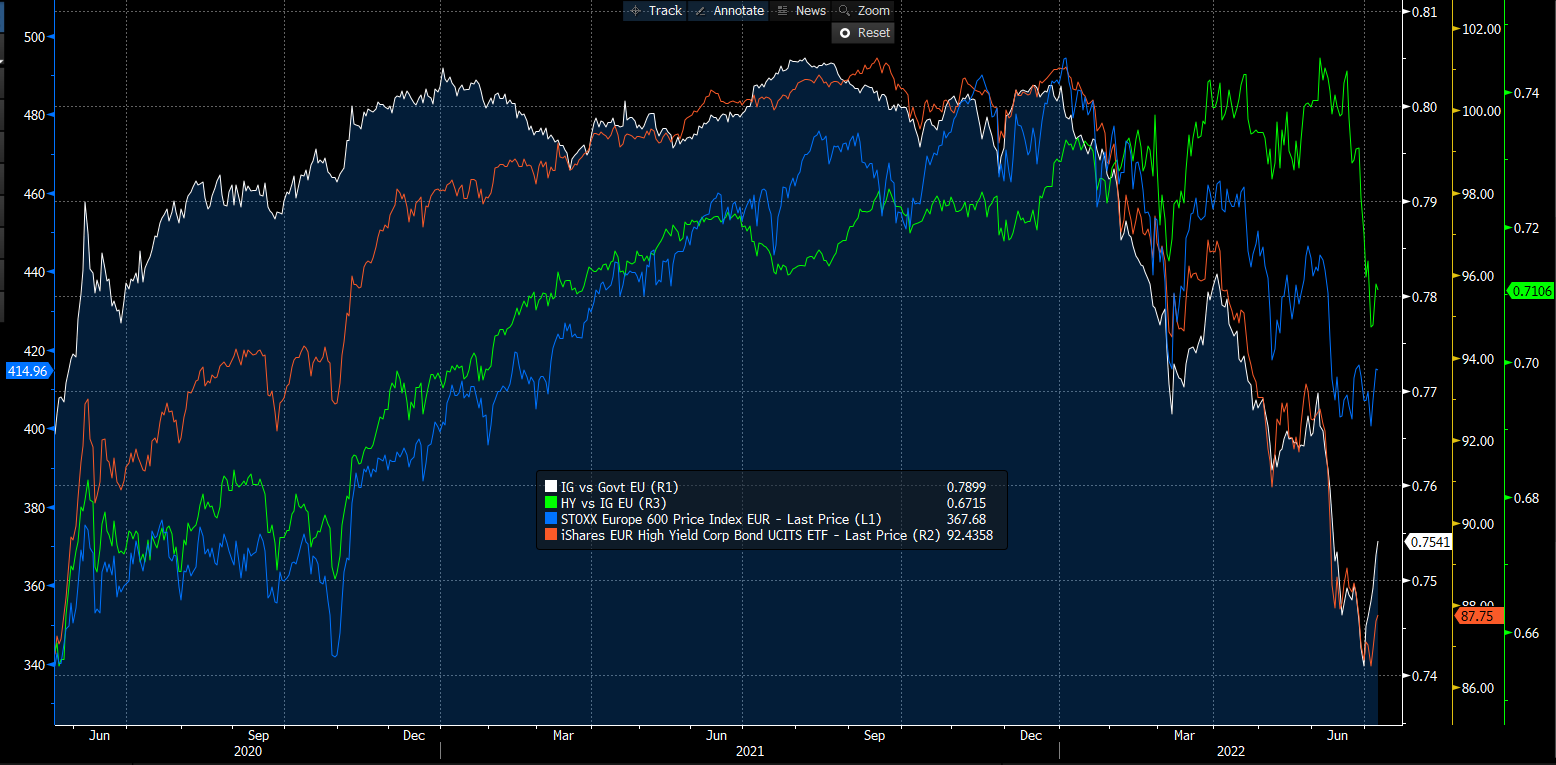

→ Credit: spreads on IG and HY tightened this week (-15bp and -17)given the good macro sentiment this week that boosted the bear market rally but the undeperformance of HY vs IG points to more recession risk priced now vs the past weeks. Given the further downside risk to economic growth going forward to me the best sweetspot remain on IG or in the BB of the HY spectrum.

→ Equity: as always I’ll look it from a top-down and intermarket point of view. Financial conditions (and liquidity) were better this week with IG to Govt bouncing strongly from the low. This, together with the better than expected macro data allowed to equity a positive week ( +2% on average for SXXP and SPX). As said before the biggest impact in credit is on the ratio HY/IG that decompressed and is now more in line with the economic context.

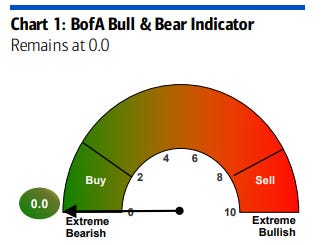

The sentiment, using Bofa Bull & Bear Indicator (or AAII Bull-bear, Put/call ratio) remain very low, but also breadth (with a lead driven by defensive sectors).

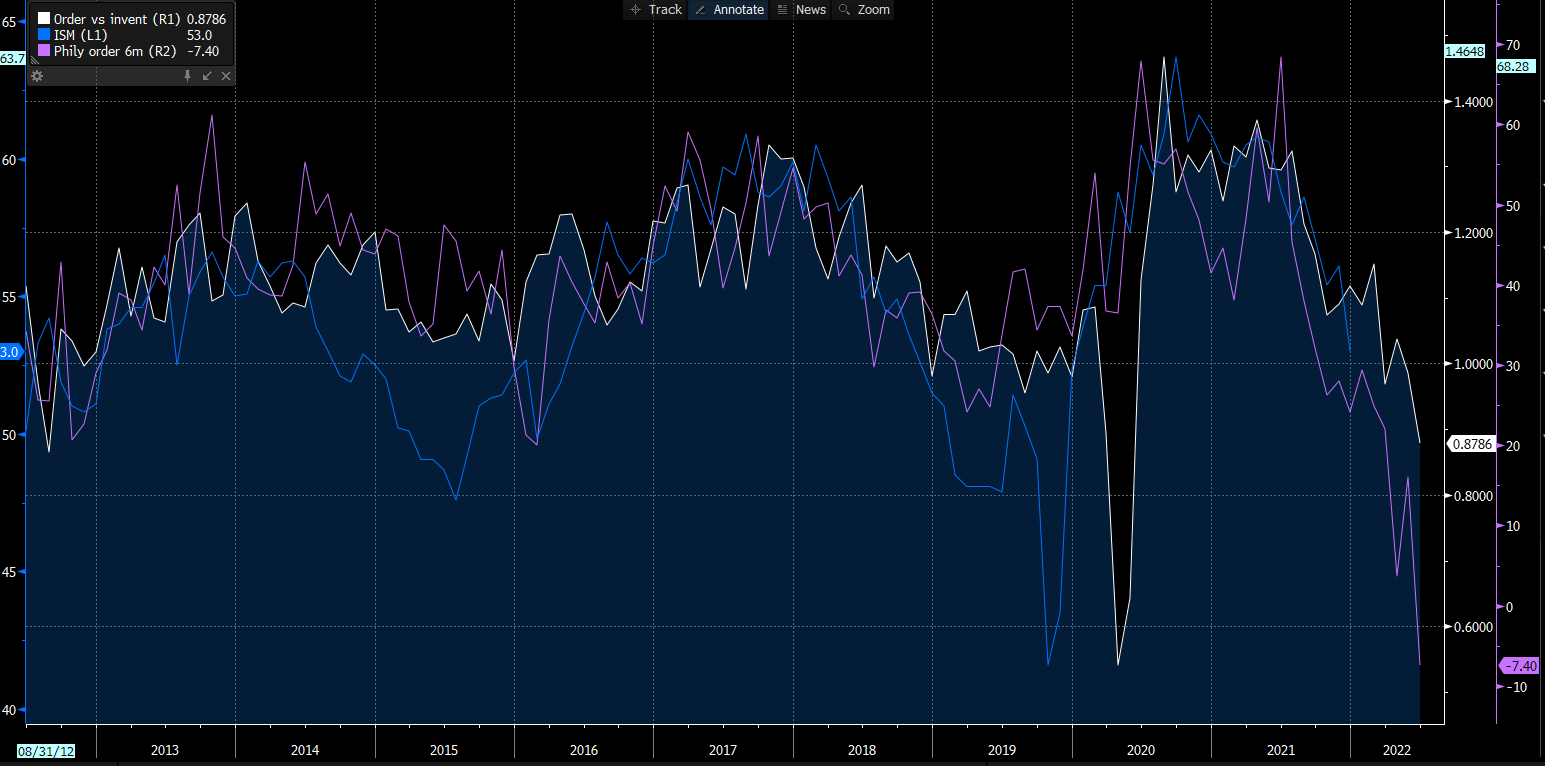

From a fundamentals/liquidity is too early to call a bottom here given pressure on macro data ahead, EPS too high and central banks draining liquidity. Below order/invetories ratio that leads ISM of several months, like the Phily FED order index.

MICRO:

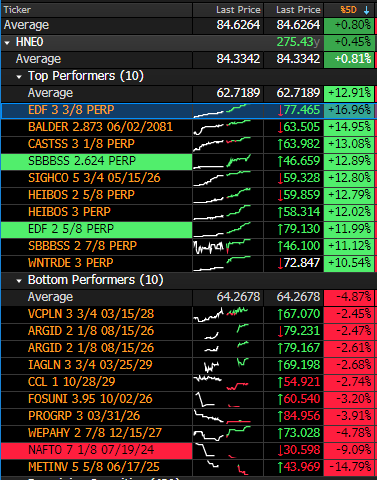

On the micro front we are at the beginning of reporting season, that could move some single name bonds, but until now it’s macro that drive, with on average bonds up 0.80%/1% on the week.

I’ll spend some words on thw winners (basically all the hybrids that suffered last week), and a positive news on EDF (nothing new but a confirmation) with French government that want to return holding 100% of the national electricity producer.

On the losers ARGID return to be impacted by the high gas prices (this could be a return for other name too), while IAGLN suffered of the cut of more flight due to the lack of workers after pandemic and the high demand of flight.

It’s all for today and this week.

Bye

As always a great article!

Thank you very much