Weekly Credit Market Review - Jul 15

Weekly Credit Market Review - Jul 15

A thread from macro to micro

Welcome back. As always if you like my job/analysis please subscribe below and share it. There was a long list of negative news this week to look, so let’t talk about them.

MACRO/NARRATIVE:

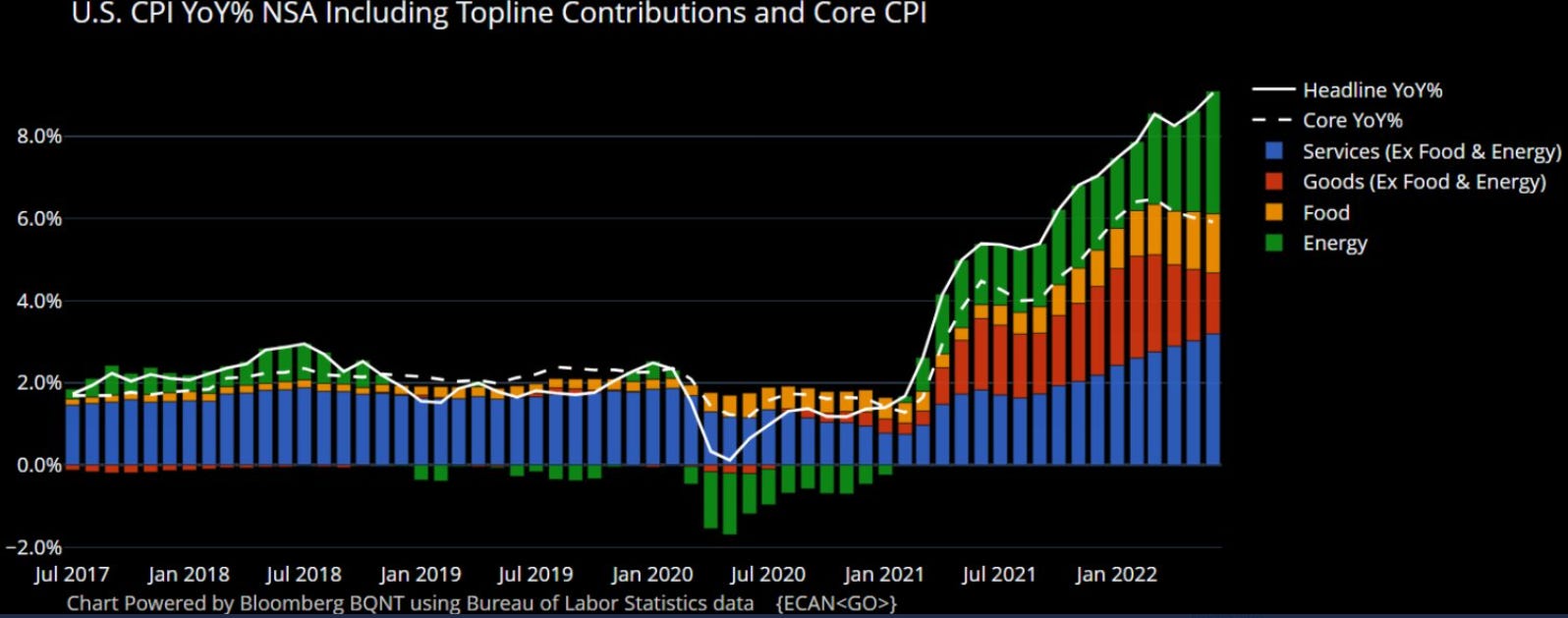

Starting from US macro data all attentions were on inflation. The CPI print for July was 9.1% from 8.6% (while expectation was for 8.8%). A lot of comments was that this data is old (and in part is true if you look at gasoline and energy costs), but under the surface price pressure are persistent, widespread and sticky (below in the first chart for headline and core prices).

Looking at contributors there is continued uptrend in services (and down in goods). Food & energy (due to gasoline) continued to put pressure here.

This data, together to a strong job market and today retail sales could give the FED a greelight for a 100bp hike at next meeting, despite Fed Waller and Bullard both said they would back a 75-basis-point hike in July after a hot inflation print.

On gas crisis, impacting especially Europe, we had (from 11th of July) the stop of gas flow through Nord Stream 1 for a 10 days period of maintenance. Here there is the risk that for some political reasons the flow will not restart anymore;

Finally on a political point of view in Europe we had the start of a new political crisis in Italy. After the 5-Star Movement's (M5S) failure to take part in a confidence vote in the Senate on a government decree. Draghi offered his resignation, that the President Mattarella rejected. Now next week there will be a confidence vote and the risk of going to vote earlier than what market expected;

This will complicate the job of ECB next will (hiking 50bp to fight inflation or only 25bp given the political risk and on growth?). Next week will be also the date to present the new “antifragmentation tool” but spread widened and arrived at 220bp (below btp-bund vs eurusd inverted).

MARKETS:

Commodities market had an other week of sell-off. All subsectors were impacted but the bulk of the movement come from industrial metals (copper -9%, Aluminium -5%; Iron ore -9%). From the “All-in-1” chart above we can see that Copper/Gold, but also Silver/Gold (Silver is also an industrial and a precious metal) signal more weakness ahead.

Rates market responded at the macro environment with an increase in the front-end of the curve (the 2y) with some hike by central banks again on the table and a more front-loading cycle (as said above job market and retails sales are good enough for FED). The long end of the curve (I’ll speak of the 10Y) was volatile around the data but closed with low rates (price action vs newflow confirm that positioning is short on rates) indicating more focus on growth and recession. The movement of the curve was that of a flattening, with 2-10bp (a good proxy for long duration) going to -25bp and remaining inverted.

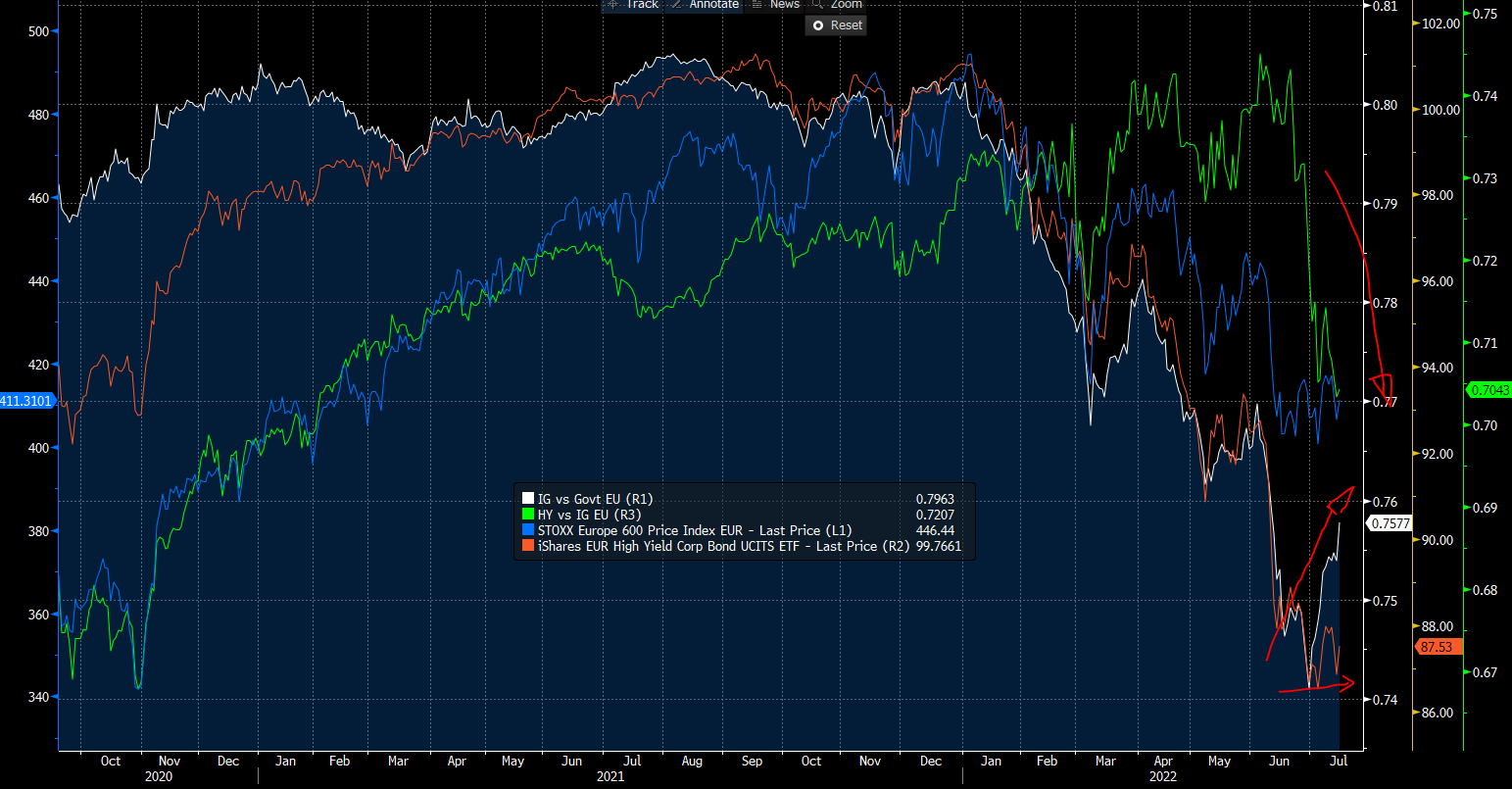

Credit, my bread and butter, is now pricing better the environment with an underperformance of HY vs IG (in green the ratio of european ETF always). Spread on cash bond of IG and HY were flat on the week, while total return was driven by rates. Crossover (the HY CDS) remain above 600bp. I’ll continue to prefer the quality rating (BBB/BB to B/CCC), like also defensive sectors.

One of the reason (beyond liquidity - the most important of fundamentals) is also the rating drift, that follow the EPS revision, with more pressure on weakest name, sectors and rating (see below). But one point of optimism come from the uptrend in IG/Govt ratio, that benefit from the hope of having saw the peak in interest rates yet (We will see).

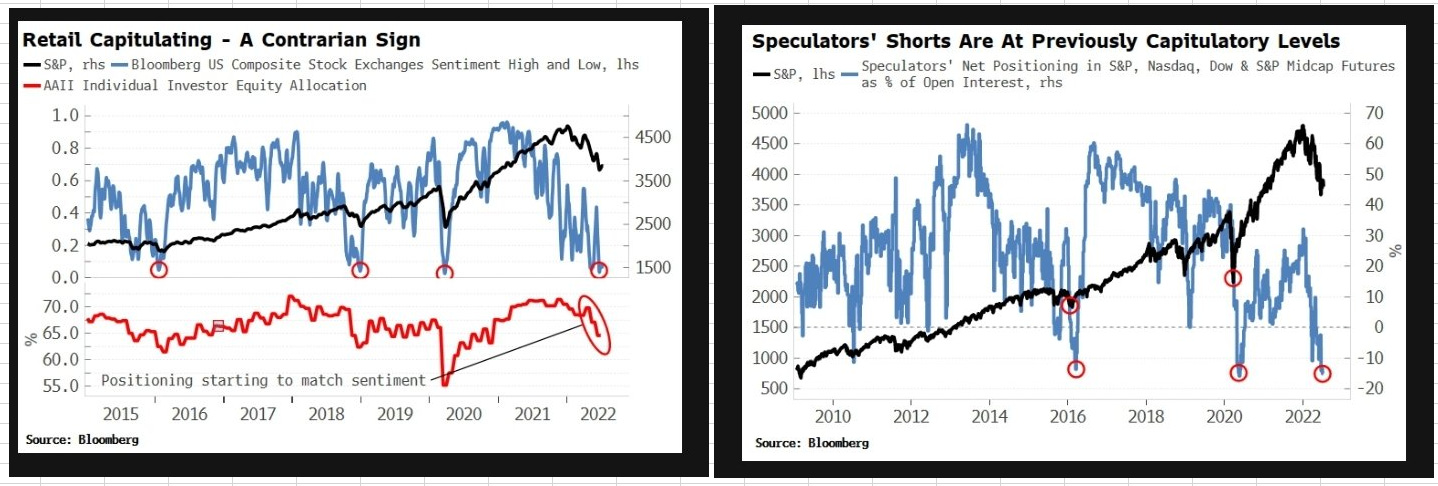

On equity some consideration are similar to HY. Liqidity is negative and will impact EPS. To turn positive on risky asset we need so a stable top in yield (IG to Govt is good but not enough yet). Here we have very negative sentiment and position indicators. Below we can see that retail equity allocation (AAII) converge with negative sentiment and speculators shorts remain at capitulation level.

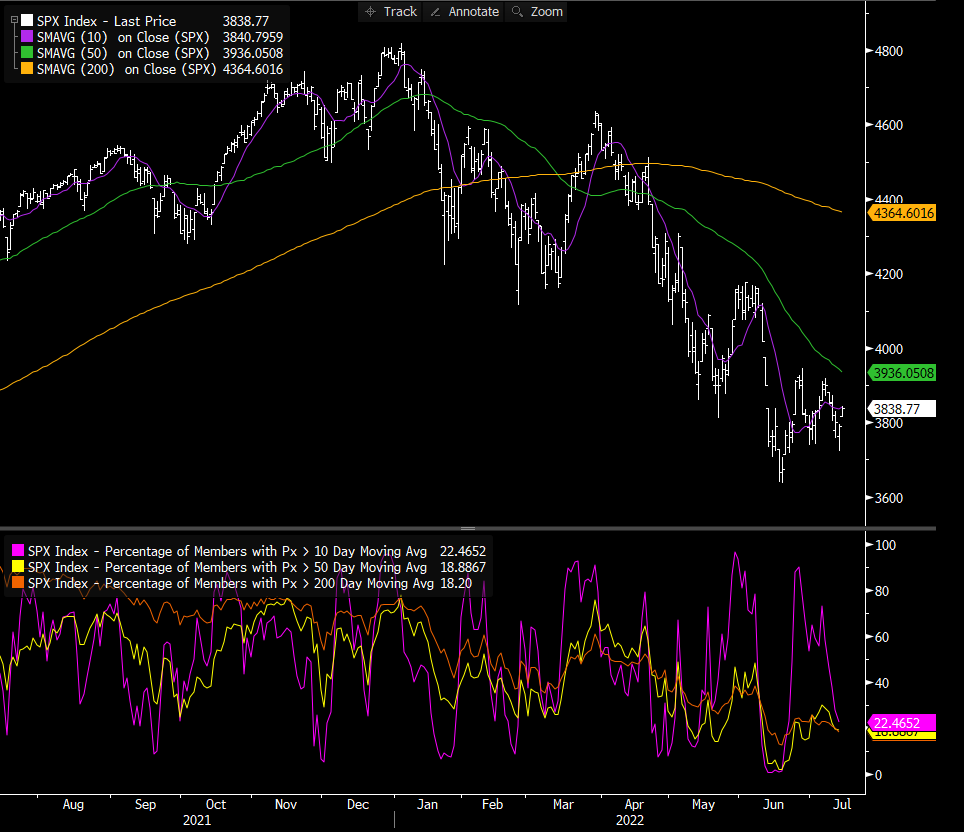

Also the breadh (below the % of stocks of SPX above moving average) remain at depressed level. All indicators are good contrarian indicator for a short term rebound.

MICRO:

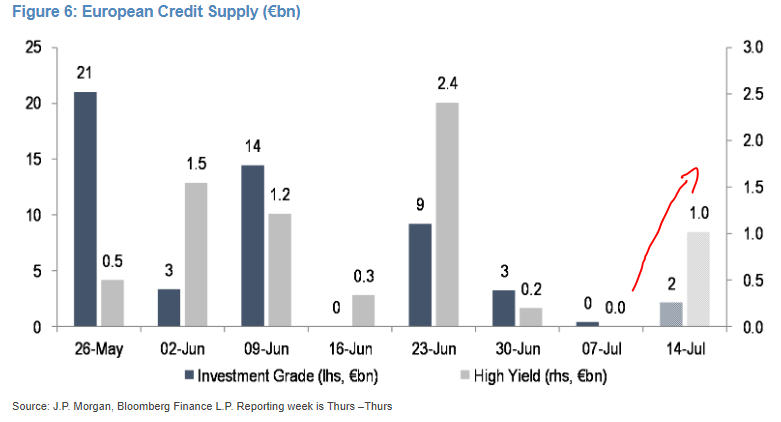

I want to start with a chart of supply new issue. Finally we have a return for that market, with Prestige Bid co to issue to refinancing their 2023 bond.

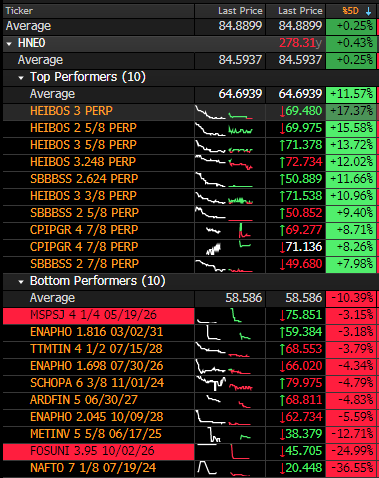

Regarding single bond performance the biggest performers of the weeks are:

the perpetual of HEIBOS (where there is a tender of these bonds)

the perpetual of SBBBSS that, like others name in the sector, suffered in the past weeks but benefitted by news of disposals newsflow by the company

It’s all for the week, yestarday was my birthday (39yrs old). Now I am older, and I hope wise to.

If you liked my job, feel free to forward it to colleague and friends.

Have a nice weekend, bye.

Your updates are cool, I’m a bit behind in reading so belated hbd!

Cool!