Weekly Credit Market Review - Jul 22

Weekly Credit Market Review - Jul 22

A thread from macro to micro

Welcome back to all readers. Before starting just a note of service. Weekly Credit Market Review is going to holiday for some weeks. As always if you like my job/analysis please subscribe below and share it and I remember you that I am also on twitter at @Credit_Junk.

There was a long list of events this week, so let’t talk about them.

MACRO/NARRATIVE

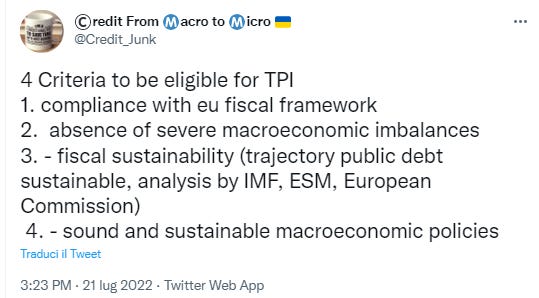

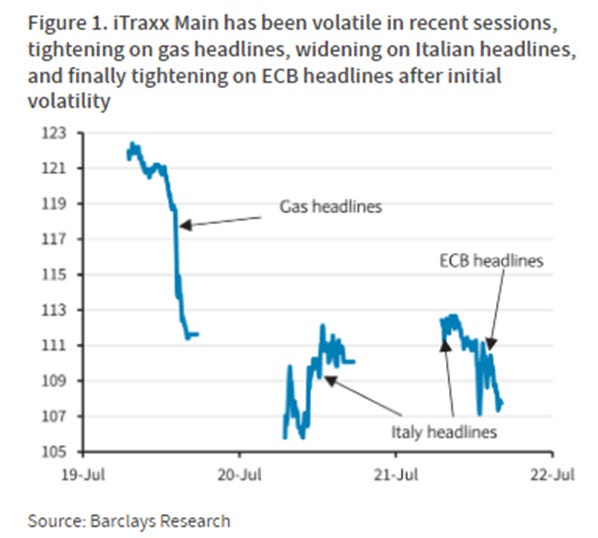

The biggest event of the week, without doubt, was the ECB meeting. ECB started the hiking cycle with 50bp move, abandoning forward guidance (having said that this meeting was 25bp) for a meeting by meeting approach. The focus was on inflation that remain persistent and the need to raise rates frontloading them (more now, less later) mantaining terminal rate stable (their forecast is for a neutral rate between 1-2%). To be able to increase rates, without having fragmentation, and having a good transmission of policy they presented the new instrument (TPI - Transmission Protection Instrument). The functioning remains a mistery for the moment below the point of sterilization and balance sheet and is linked but was presented as “unlimited” regarding the size and with actions as a function of severity of risk facing policy. Yesterday during the meeting I showed the criteria considered by ECB to be eligible (basically are linked to macreconomic and fiscal rules like the old OMT).

On the positive front at the end of the scheduled maintenance period of NS1, Russia began sending again to Europe, despite at only 40% capacity (as 10 days ago).

The most looked political newflow come from Italy where, Draghi won the confidence vote in the upper house without the support of M5S, Lega and Forza Italia (basically a big part of the parties that supported him until now) and resigned definitely (with election expected to take place between end of September and start of October)

MARKETS

This week I’ll start talking about the equity market, given that (volatility adjusted) it’s here that happened the big movement. This week Eurostoxx is up 6.4%, S&P 500 +5.35% and also Nikkey +4.6%. Clearly the positive news regarding gas from Russia helped to balance the negative news coming from macro and political situation.

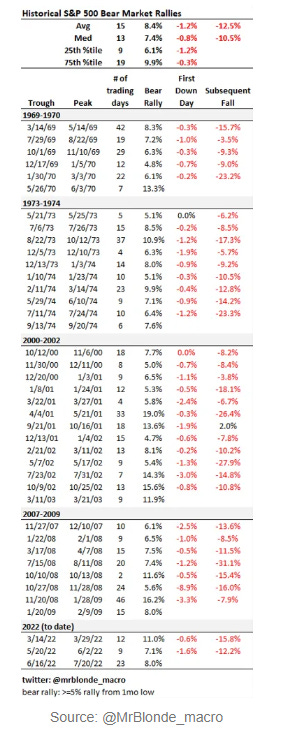

How it’s possible? Clearly recession fear is now consensus and sentiment/positioning is very low and depressed and at the margin also some positive news coming from reporting season (that started in USA) could give push to a bear market rally.

It’s not unusual, during bear market, to have mini really like this one. Below a great recap of @mrBlonde_macro.

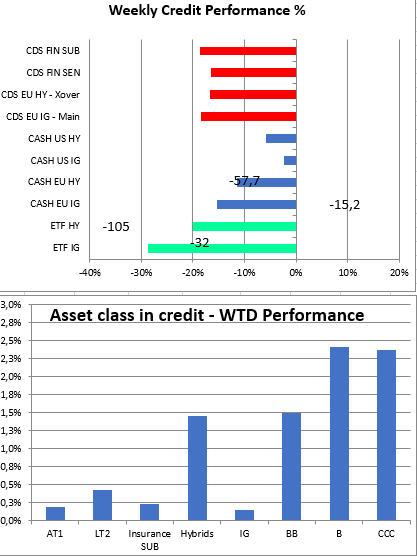

A great driver of the positive sentiment on equity this week was a stabilization of the main liquidity indicators (IG to Govt and HY etf - below in their euro version) turned up strongly thanks to a stabilization in rates.

Looking also at US indicator (JNK - US ETF and CCC spread) the tone was positive, but long-term indicators (I use LEI index) show that the direction of travel remain weak.

Passing now at credit both IG and HY had a great week, in line with equity tighening 15 and 50bp respectively. From an asset class point of view low rating of HY benefited the most (CCC/B) with total return of 2-3%.

Looking at price action of credit during the week we can see that the big movers was the gas headlines given it’s the big risk on the head of european economy. Looking at european gas reserves, if Russia go all-in halting all gas flow, Europe will not have enough gas and this will require a cut to consumers and companies (with a great impact on growth).

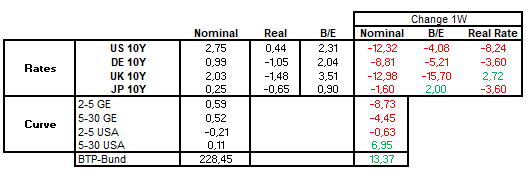

And finally some words regarding rates and governemnt bonds. 10Y in Eu and US closed the week with a tightening of 12 and 8bp. The movement is driven both from real rates (boosted today by low growth surprise and weak PMI index in Europe) and from low breakeven (thanks to a low impact of energy prices, low gas prices and commodities in general). The narrative of “low growth” is totally consensus.

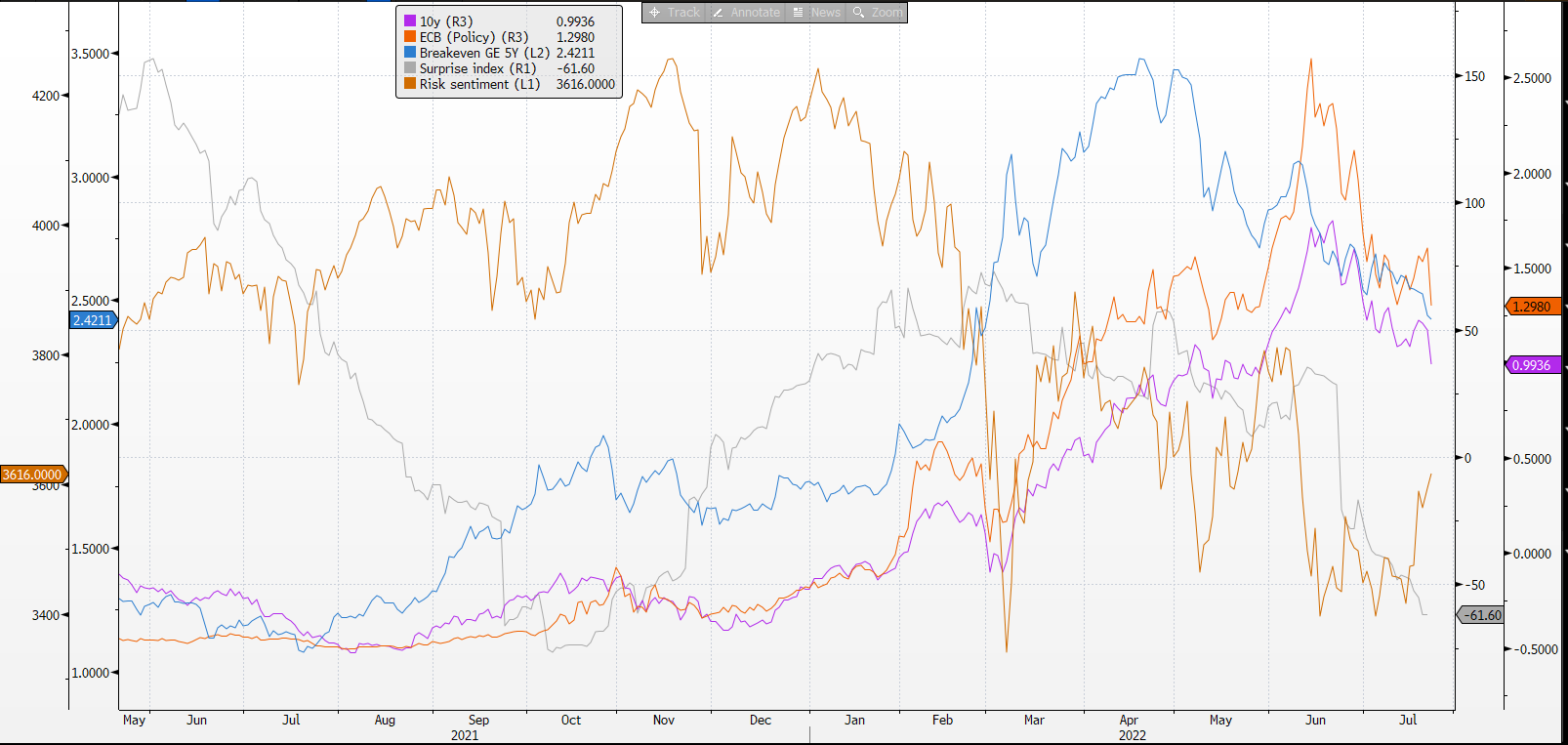

Below the main driver of rates in Europe (surprise index down, breakeven down, ECB terminal rates here 1y1y eonia an Risk sentiment using equity as a proxy).

MICRO

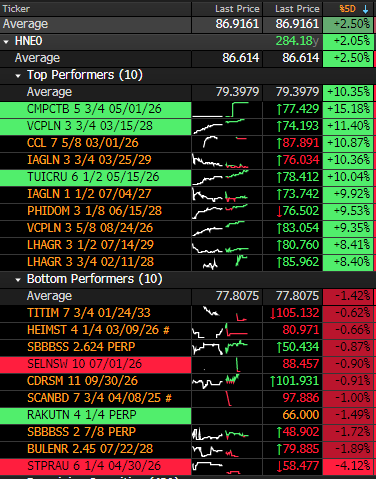

Finally, we’ll look at top and bottom performers.

On the top names we have:

travel and leisure names (CCL, IAGLN, TUICRU, LHAGR) given customers continuing choosing to spend money saved on travel after 2 years of stop;

CMPCTB - Consolis , after signing 30M of a news term loan

On the bottom list:

STPRAU: a low rating name (B/CCC) of the automotive sector with a great exposure to Turkey. No news here but CDS of the country remain high, like all other EM.

It’s all for today and for 2/3 weeks. I hope you’ll enjoy a good holiday period after a very bad and weak year.

Bye.

Great writeup, have a nice holiday!