Weekly Credit Market Review - Jun 03

Weekly Credit Market Review - Jun 03

A thread from macro to micro

Welcome back. If you like my job/analysis please subscribe below and share it. Now let’s go to see what happened.

MACRO/NARRATIVE: The main events and data out this week were:

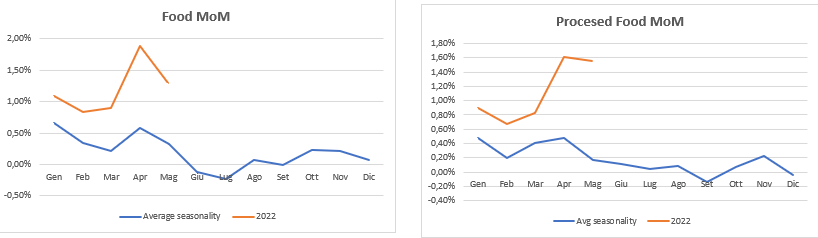

Eurozone inflation: surprised to the upside (core at 3.76% and headline at 8.05%). Prices pressure are broadening by countries and by subsectors (food expecially);

In USA we had PMI/JOLT and payrolls that showed a strong job market and a resilient economy. No big easing on wage pressure;

Central banks and market focus shifted again on the hawkish side, with no pause expected in September (FED - Brainard) and ECB expected to frontload (now 115bp increase expected at the end of the year vs 50bp 1 month ago);

China reduced some covid rules thanksto lower new cases and announced new measure to stimulate the economy from fiscal (a tax break) and monetary (increase national bank bond issuance to increase lendings);

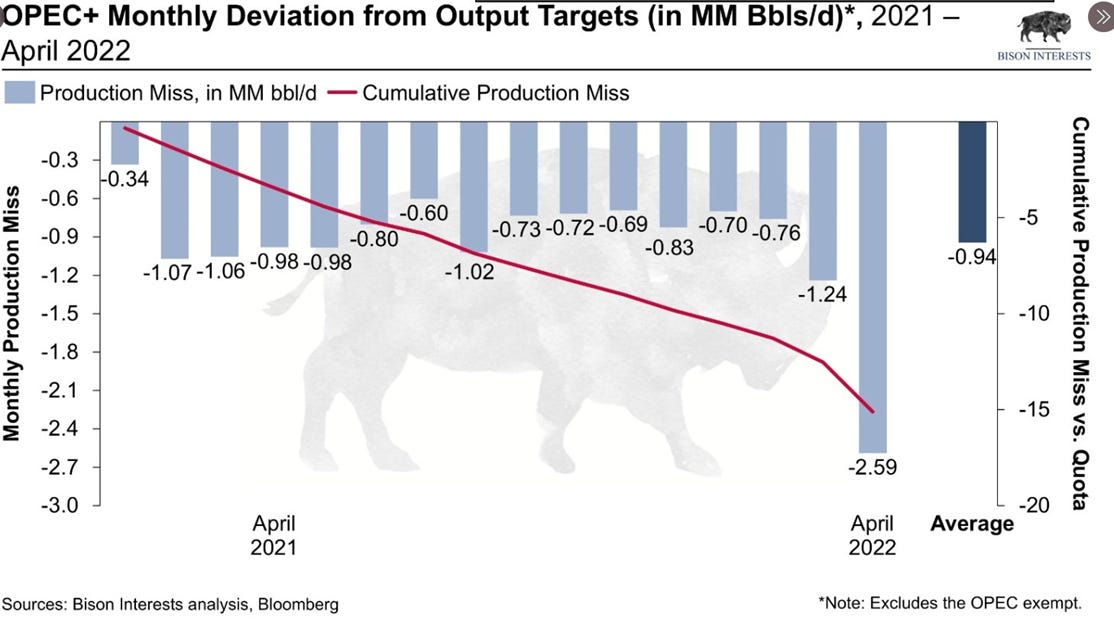

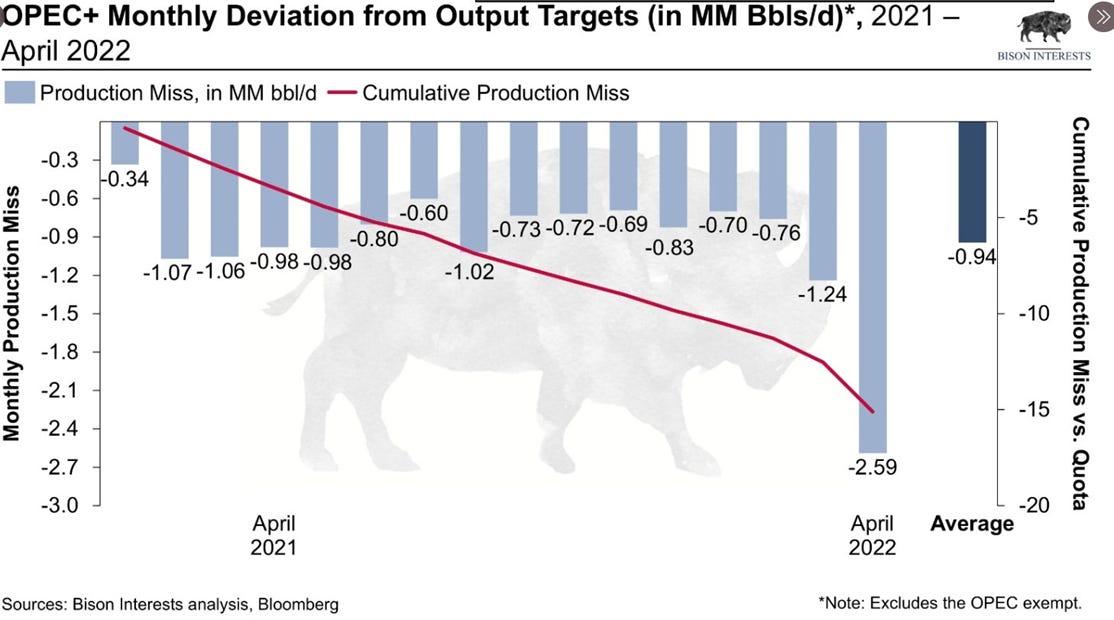

OPEC+ Agrees increasing to 648K barrels a day in July, August up from 432K barrels a day in recent months but production missed always quotas and spare capacity remain low (below a chart of Bison Capital - @BisonInterests)

MARKETS:

Most of the movement in the market happened in “RATES”, especially the front-end given what we wrote above about inflation and central bank stance.

Given their job is now to reduce inflation they are ready to kill market, housing market and job market.. No FED PUT for the moment and low liquidity.

Curve returned to flatten and peripheral spread remain at risk.

“EQUITY” closed the week in green (S&P +2% and Stoxx +1.3%) continuing this “bear market rally”.. ok it’s now consensus.. but that’s it.

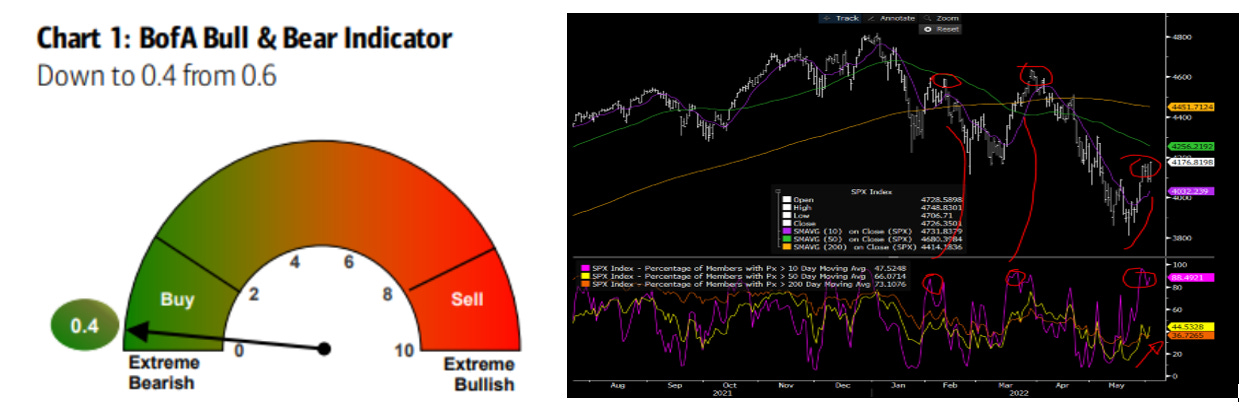

ES1 is now approaching big level (pay attention when supports become resistances). Clearly the sentiment is very negative at the moment but position is not extremely short. Fundamentals (liquidity and macro momentum) remain weak and also EPS momentum could be at risk. Also breadth is better than some weeks ago (% above 200ma reached a bottom) but short term (% above 10day) could be and indicator of top.

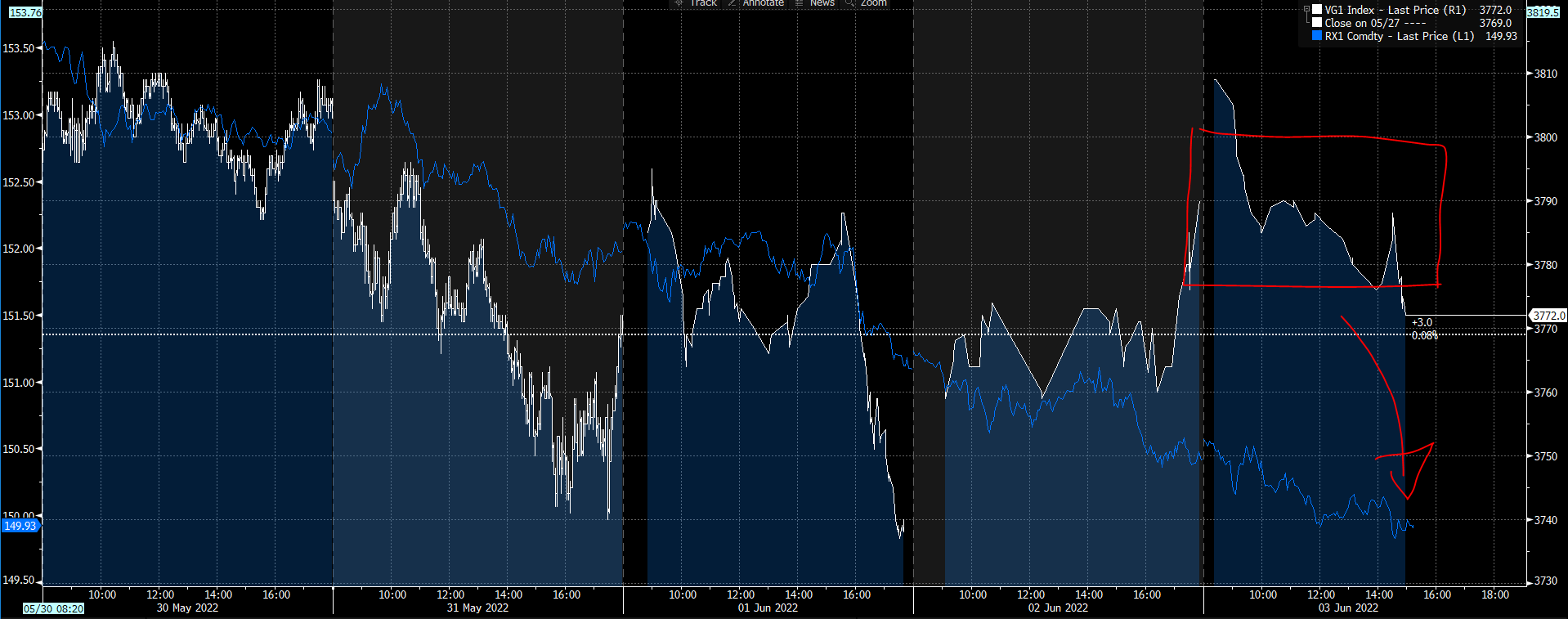

And with pendulum again on the inflation camp (vs growth) returned the positive correlation between stocks and bonds during this week (below the VG1 european index vs bund 10y germany), a difficult enviromentent for investment again.

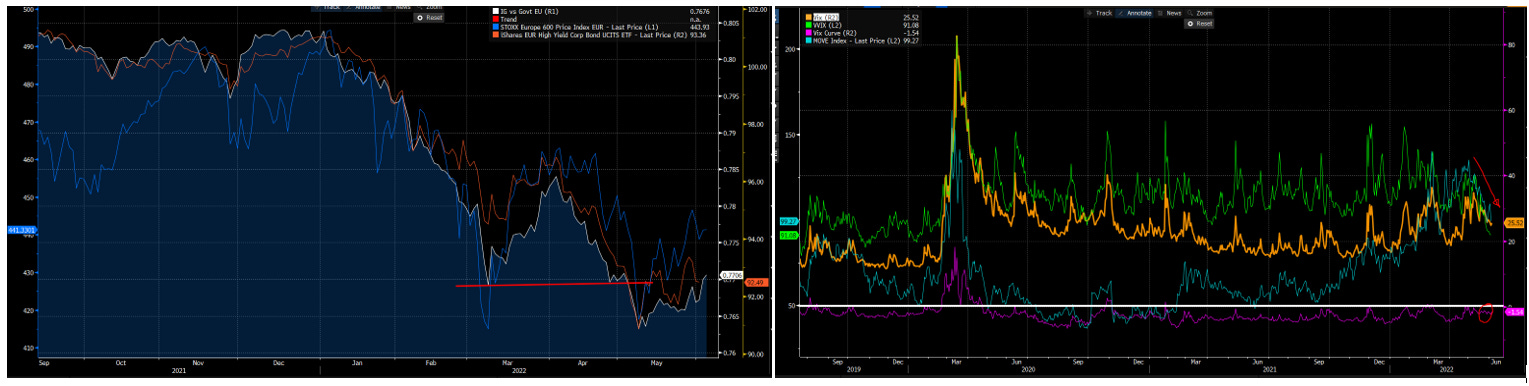

Looking at STOXX Europe from a intermarket point of view.. it seems that credit continue to give green light to the rebound (IG to Govt up) and until MOVE (rates vola) decrease, like VVIX and VIX (with the VIX curve not inverted) we could go ahead with this choppy environment.

In “COMMODITIES” we had a strong energy subsectors thanks to oil rebound (despite OPEC production increase the inventories remained low) and strong gasoline/diesel price (low inventories ahead the driving season).

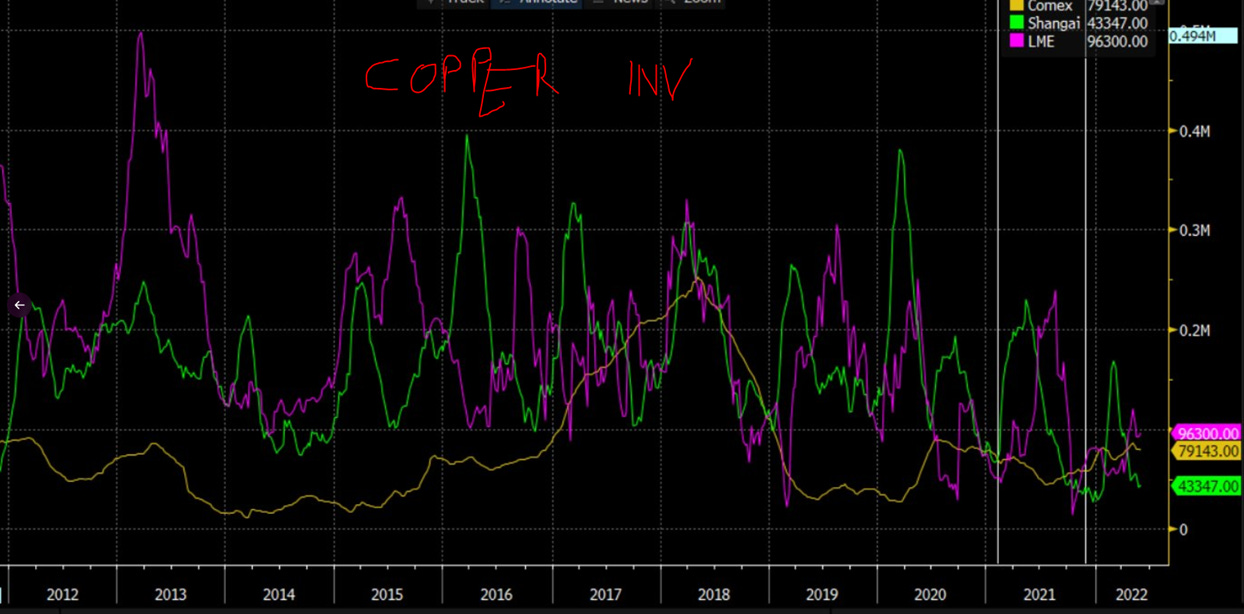

Copper rebounded due to China reopening (and stimulus) and a market that remain tight (below the inventories level) and at risk of supply problem (il LATAM).

Agri (Corn and Wheat) closed the week weak as more grain seen coming from Ukraine (21-22 season) after some talks of Turkey facilitating to establish safe corridor for grain.

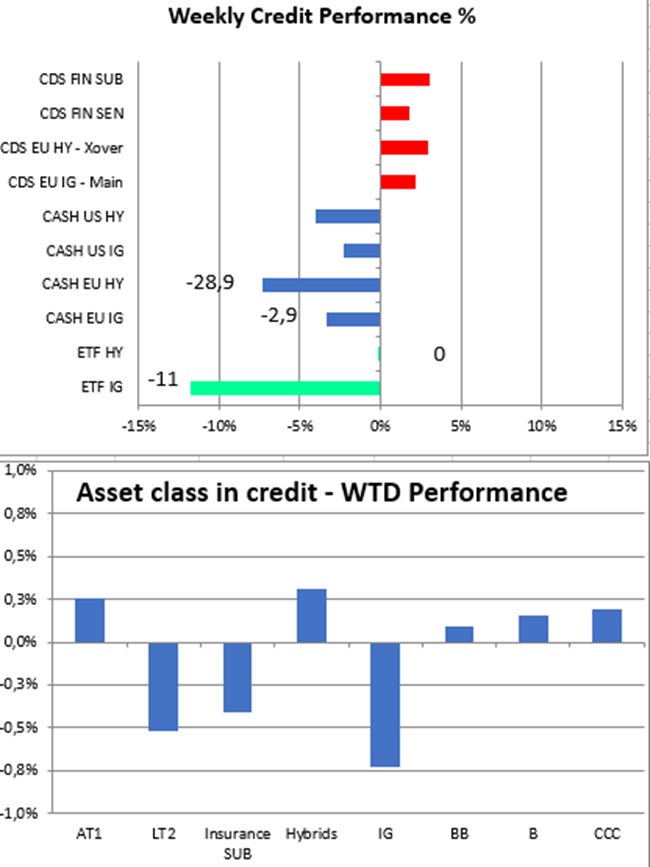

“CREDIT” spread closed strong (with -28bp on HY and -3bp on IG). From a total return IG suffered from the duration link while low rating (CCC/B) closed better than BB with the ratio B/BB and in general the HY/IG ratio not protecting enough in case of recession.

MICRO:

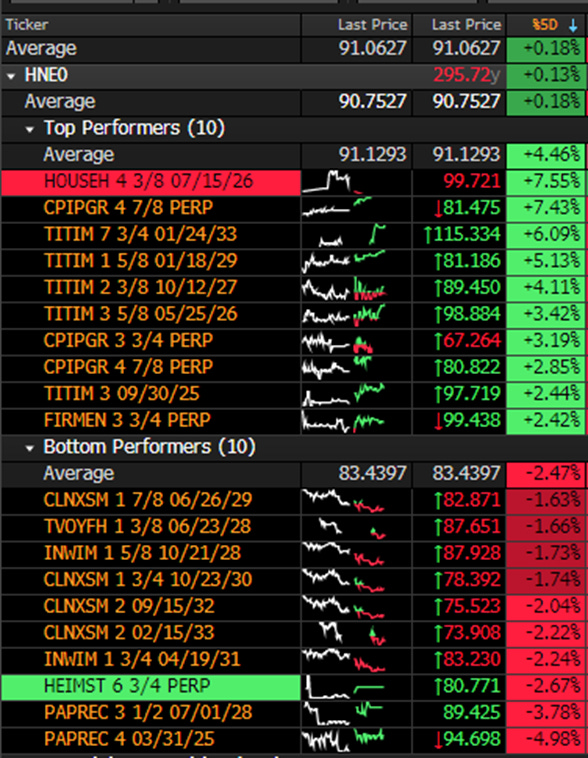

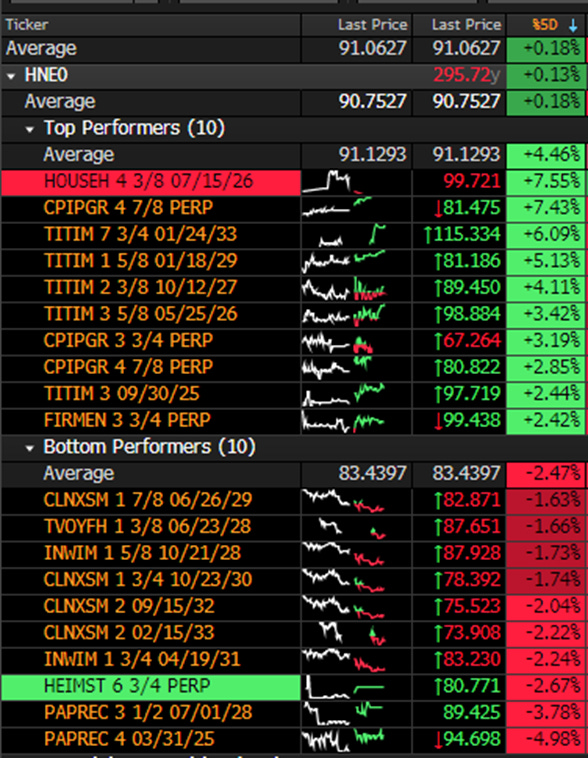

Loser of the week is clearly

PEPREC: following press articles referring to an investigation for"favoritism," "corruption," "unlawful taking of interest," and "acting as a cartel" as part of the award of a public contract in waste processing.

Winner of the week is

HOUSEH (House of HR) after news of last week that Bain Capital becomes new majority shareholder

TITIM that signed a preliminary contract with CDP regairding single network