Weekly Credit Market Review - Jun 10

Weekly Credit Market Review - Jun 10

A thread from macro to micro

Welcome back. If you like my job/analysis please subscribe below and share it. Now let’s go to see what happened.

MACRO/NARRATIVE: The main events and data out this week were:

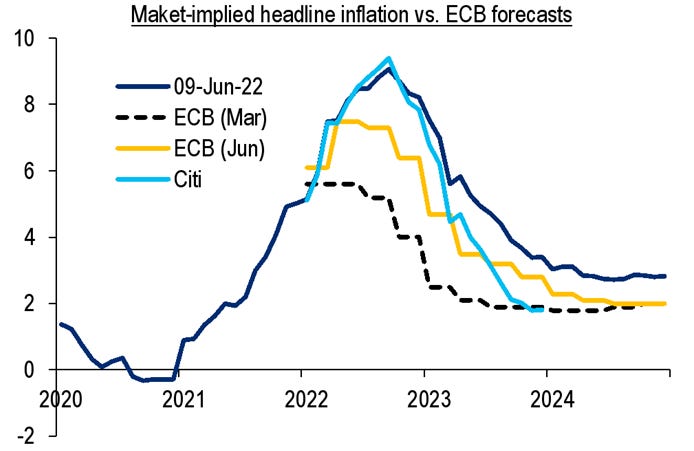

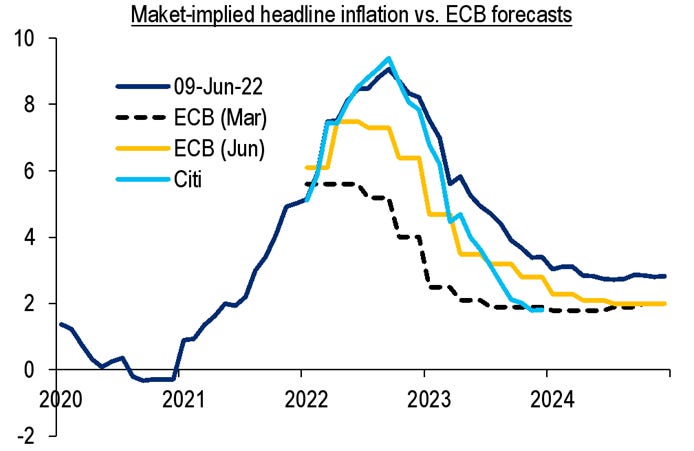

ECB meeting: where board downgraded growth expectations and incrased inflation forecast, while announced it will end the net purchases under the APP programme on 1 Jul. Given the situation they said yet that intends to hike policy rates by 25bp in July. For September they remain data dependent but if inflation will remain at this level (or higher) they can go for a 50bp hike. These will set the stage for zero policy rate in September yet and positive at year-end.

The outcome is clearly hawkish, because together there was no details about to prevent “fragmentation risks”, so market reacted with a strong widening of BTP-bund and a weakening of euro currency vs dollar.

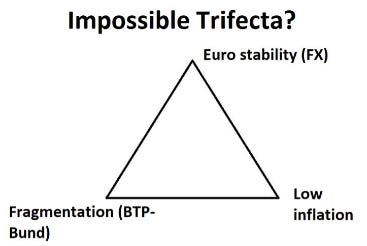

Going in this ECB meeting my theory was that of a “possible trinity” with central bank able to achieve only 2 of them, but the weakening of BTP (and the fragmentation fear) was so brutal that impacted the sentiment on the single currency too.

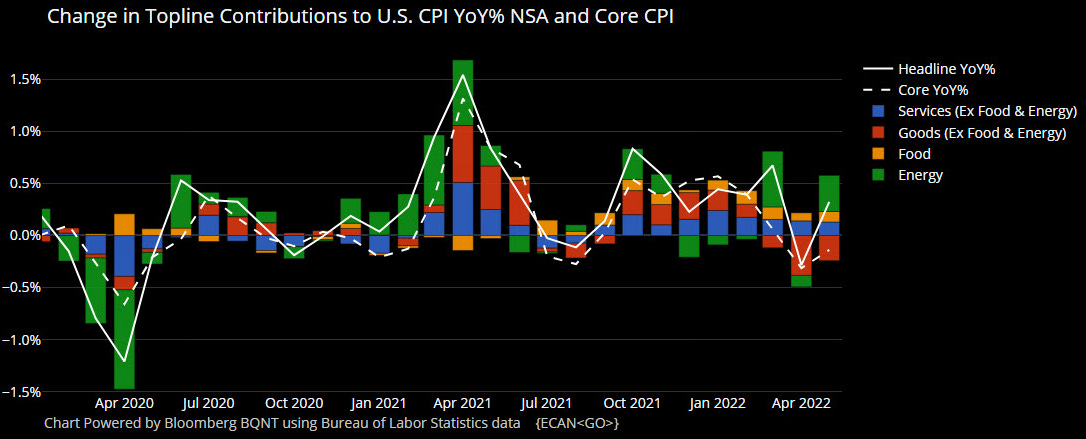

The other big event of the week was the US CPI print for May. Inflation was hotter than expected increasing to 8.6% vs expectation for 8.3%. The core (ex energy and food moderated) from 6.2% to 6% but less than expected (5.9%). The switch from goods to services continue and shelters, airfares and hotels continue to rise going into summer. The energy part (with high gasoline prices and low inventories) could remain high for other months too.

MARKETS:

On markets, given the importance of the move and my background I’ll start with fixed income and credit (that are also the main liquidity driver).

RATES:

Rates around the world continued their march higher (US 10y is back above 3% and Bund above 1.4%), driven especially by short term rates. Given the high inflation sentiment now market expect central bank to act more now and less later (frontloading the move) and terminal rate continue to rise (in EU it’s almost at 2%, with some central banker believing neutral rate is near 1.5/2%), with the move almost driven by real rate. Curve flattened on short term (hike by central banks) and long end too. Given the lack of clarity about “anti fragmentantion” BTP-Bund spiked and reached 225bp. Where will be the trigger for ECB to act? Lagarde said “we are not here to stop the spread”. It’s evident my president.

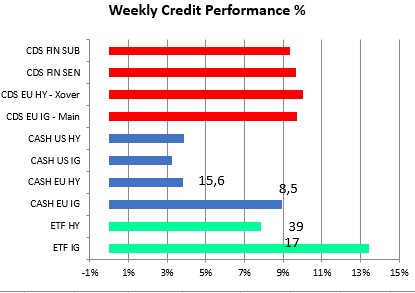

CREDITS: credit suffered from tight financial conditions given by high risk free rates and despite low positioning and lack of supply both IG and HY widened this week (9bp IG - 15bp HY using index, 17bp IG - 39bp HY using ETF). In this environment ETF is a better indicator of direction and market sentiment being based on true trade.

The multi time frame that I used to look at liquidity (the main fundamental driver) and ispired by @macroops ) started again to give red light on all the time frame. In fact now (using dollar and US index below) all they are going south:

LEI for L/T liquidity

CCC spread for M/T liquidity

HY ETF for S/T liquidity

Most of the indicator are credit spread related because credit always leads equities.

“The availability and pricing of credit is a direct lever on liquidity”

EQUITY: this week market reaction was very bad. Liquidity, as seeing above, is bearish and also technicals don’t support the market now. S&P 500 is -6%, Europe is -5% (with italian banks near -10% too impacted by BTP).

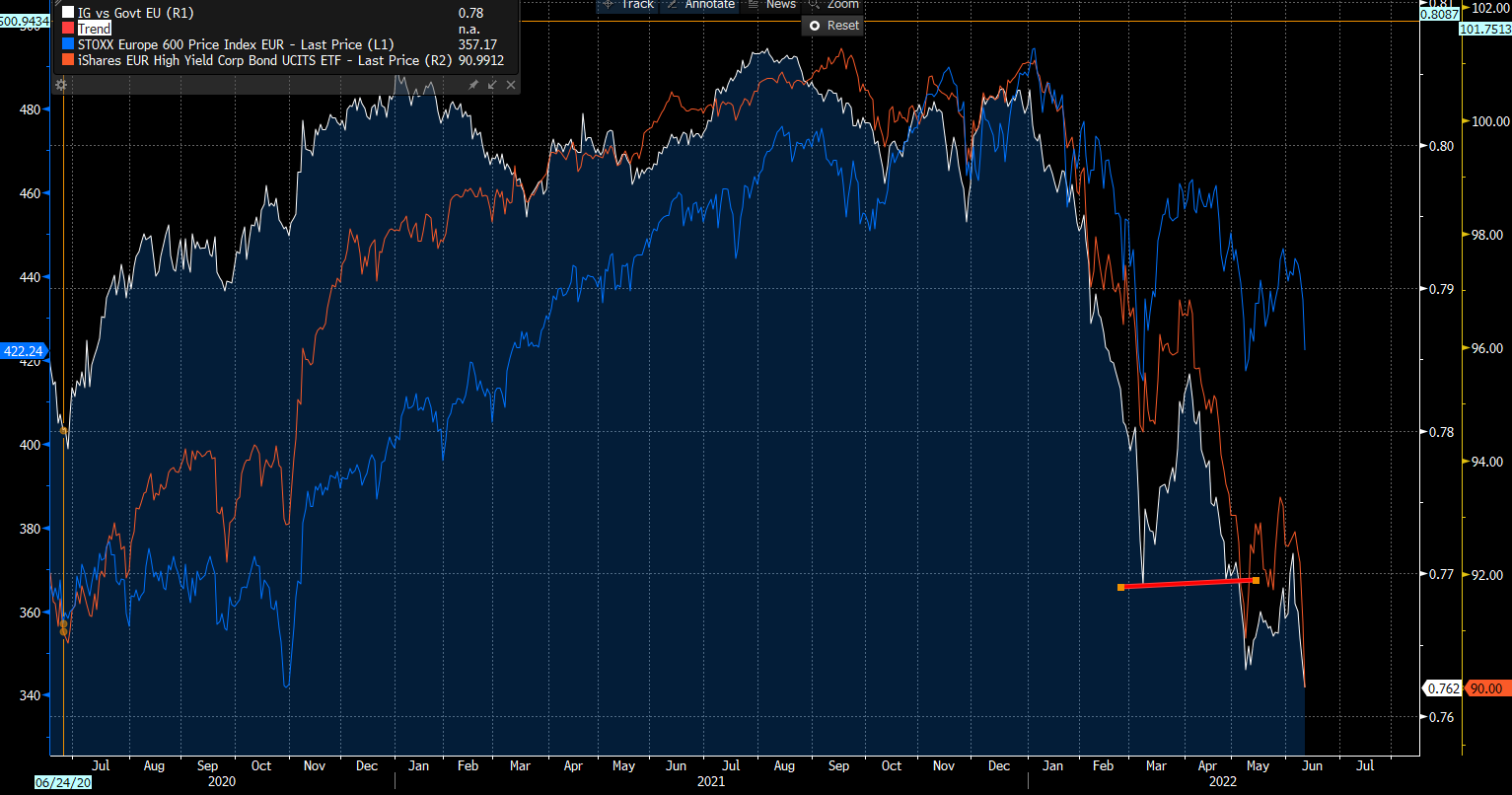

Below the main liquidity indicators for Europe that I use are IG/govt and HY ETF (IHYG) are now below their recent bottom and opened a huge gap with equity markets.

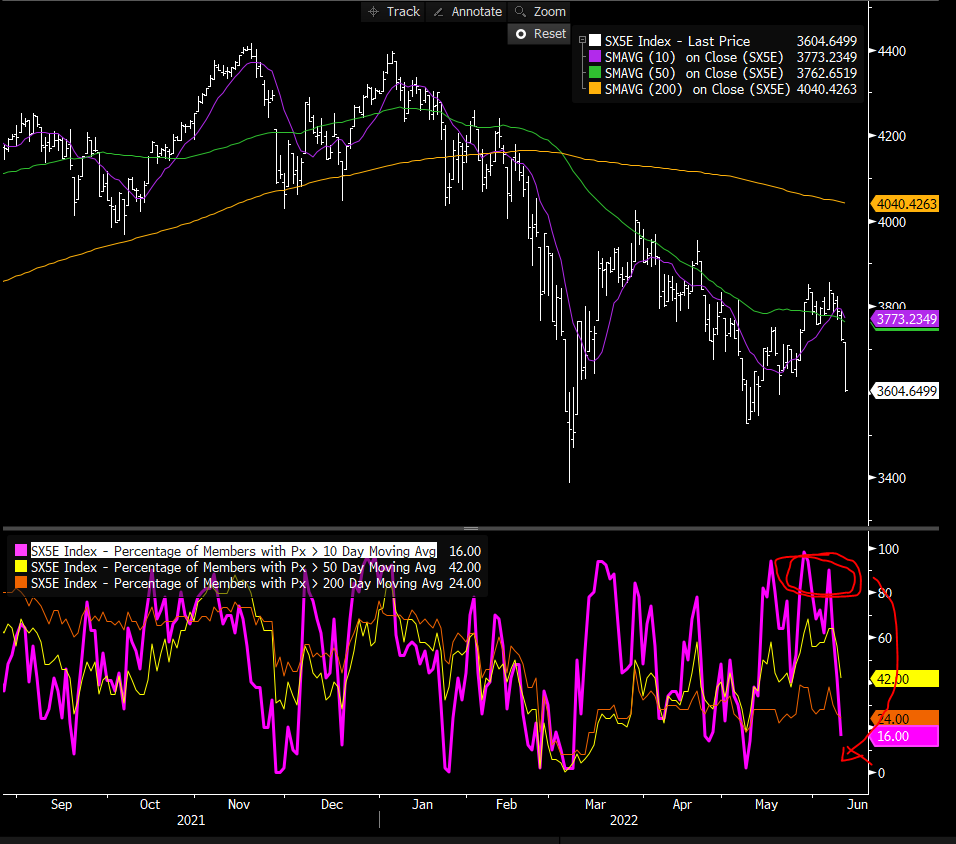

Looking at technicals on Stoxx Europe the trend remain negative and price action is that of a liquidation to be honest. The “bear market rally” arrived at very important level (where converged also some moving average) but as I said last week short term breadth (% above 10day) was extreme and indicating a top.

Now until we reach a top in inflation and a top in hawkishness of central banks (the true one) that lead at a bottom in bonds prices we can have a very tradable bottom in equity I think.

MICRO:

The travel direction was negative so in the winner league we find only dead cat bounce names like ADLER/ADJGR and FRIGOG.

Idiosincratic negative stories arrive in the loosers league with:

PAPREC selling pressure after Chairman questioned in corruption case last week;

GRAANU with results highlighting pressure on margins and low raw material availability

It’s all for today. Have a nice weekend.