Weekly Credit Market Review - Jun 17

Weekly Credit Market Review - Jun 17

A thread from macro to micro

Welcome back and thank to all new arrivals (we are almost 300 now). If you like my job/analysis please subscribe below and share it. Now let’s go to see what happened.

MACRO/NARRATIVE: The week was dominated by central banks actions that, after months to repeat that inflation was temporary, decided to act and prioritize inflation over growth. This mean to tight financial conditions and to sacrifice financials markets.

FED: after a strong CPI print last Friday at this meeting FED hiked rates by 75bp (in line with market expectation but above their last forward guidance. With the dots they showed their estimates of terminal rates (at 3.4% at end 2022 and 3.8% at end 2023). With the estimate of “neutral rate” at 2.5% this mean that they will arrive 100 above this (an in restrictive land) this year yet. After that they could increase by 25bp at meeting but before they can continue with 50/75bp at least;

SNB/BOE: Swiss central bank hiked by 50bp (more than expected) despite a lower inflation than peer while BOE hiked by 25bp as expected given the trade off of inflation and growth (but with a hawkish forward guidance given by the high level of inflation);

ECB: after last week meeting were was introduced some sort of backstop to spread (without details) market pushed for more and with BTP-Bund spread at 250 (and yield at 4% on 10y tenor) Schabel delivered a speech on fragmentation and an extraordinary meeting was announced with more details about that (a flexibility in the PEPP use and a new instrument to be presented at the July meeting). Some leaks about that suggest that some instruments should be sold to permit to buy debt of peripheral bonds and a line in the sand was drawn at 250bp for that with spread tightening strongly and arriving below 200bp;

BOJ: Despite the attack of the market on their bond market and currency, BOJ mantained stable the YCC with a 0.25% target on 10y bond. On the weakness of JPY they made a rare reference to the currency market, saying it needed to watch its impact on the economy and markets. Only today they are affirming: “BOJ'S GOVERNOR KURODA: WE ARE READY TO EASE POLICY FURTHER IF NEEDED”.

Looking at some importants macro data this week in US we had weak housing data (logically with this mortages rates) and the start of an uptrend in initial jobless claims (the FED announced they want a less tight job market too):

US housing starts 1549K vs 1693k expected (prior 1724k)

Building permits 1659k vs 1778 expected (prior 1819k)

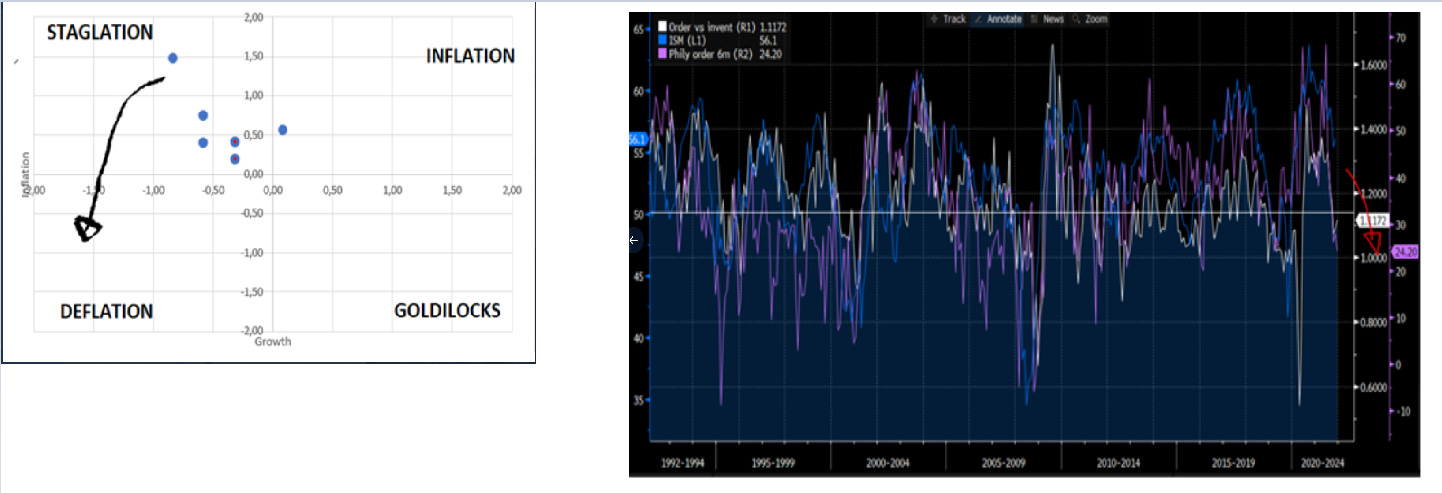

So the scenario continue to be one of high inflation (at least until we reach an effective top on data, knowing that monetary policy works with a lag and a macroeconomic environment of slowing growth. Below on the right we have the order/inventories ratio for ISM or Phily FED that says that in 6/9 months we’ll have a below 50 ISM. Basically we are on the cusp from a stagflation scenario and a deflation scenario. On the top left quadrant we have positive correlation between bonds and equity and only commodities outperforming. On the bottom left we return in a environment of good performance of bonds. But timing will be very important! (Also Stanley Druckenmiller now is less confident to be short bonds vs 5/6 months ago)

On the market regime below the single dots are done using different measure and different time frame. Nothing rockscience, but if you have questions, be my guest!

MARKETS:

This week we had a lot of volatility around central banks meeting (with an increase in all measure of volatility) but at the “end of the day”:

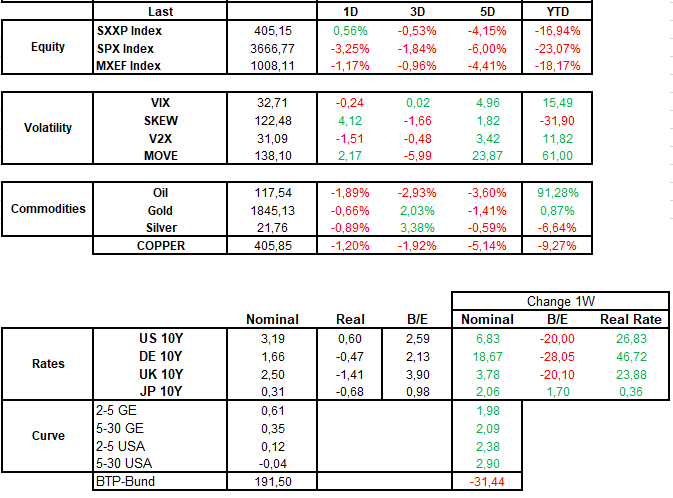

on RATES we have a logical reaction with an increase in rates driven by an increase in real rates and a decrease in breakeven (the inflation priced by the market). If the central banks want to “kill” inflation they have to bring out us from the negative real yield world. Also the decrease on inflation priced from the market is in line with expected and with the scenario we talked above. Btp-Bund spread was the big winner of the week on govies land while curve steepened a bit with some more details about the FED future path of interest rates (25bp after they reach neutral rate, so less front loaded than expected).

this environment continue to impact EQUITY (and also the next one) with performance between -4%/-6% on average this week in Europe and US. Internals of the market say clearly were we are in the market cycle. With high inflation the consumers is impacted by high bills for energy, food, etc, etc.. so at the end of the cycle there is a battle for the lead between energy and staples/utilities/healthcare. At the end (when we are on the cusp between late cycle upturn and early cycle downturn) the defensive sectors win given the real wages are negative and only essentials consumers benefits.

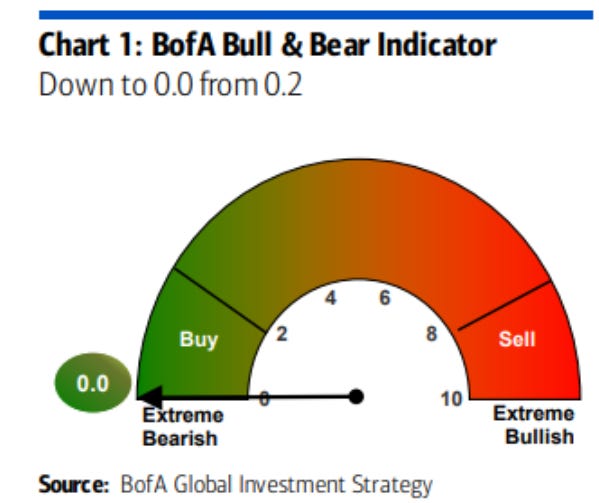

Sentiment is depressed, true (below the Bofa Bull & Bear) but it’s the same for other indicator like AAII and also breadth is very negative with only 10/12% of name above long term trend. This could be a catalist for a short term rebound (but please don’t put me on the list of people talking to buy each dip, could be only a short term one).

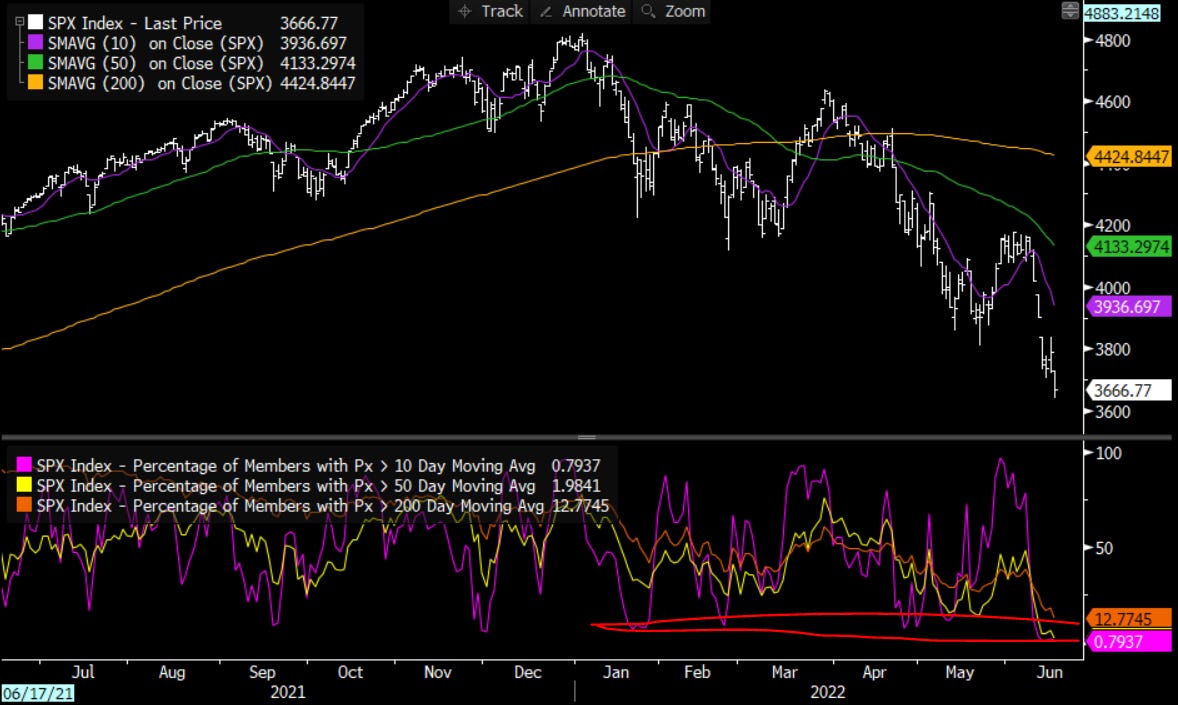

Looking at valuation of equity (using the SPX below) the correction is important and returned on the average pre-covid (the winners of Covid are the big loosers now). But you don’t need to look only at valuation to trade the market.

Looking at EPS they remain on the moon despite a tight liquidy (below I use the multi time frime model of LEI, CCC spread and HY ETF) and financial conditions. I’ll add also that a regression of oil, rates and dollar say it’s impossibile they’ll remain there.

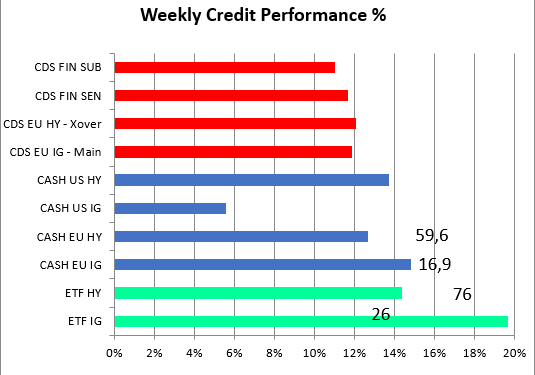

In credit, like in equity, this week was brutal with widening of 50/60bp on HY and 20/25bp for IG. CDS is more volatile but less impacted by liquidation flow and technical problem linked to rates.

MICRO:

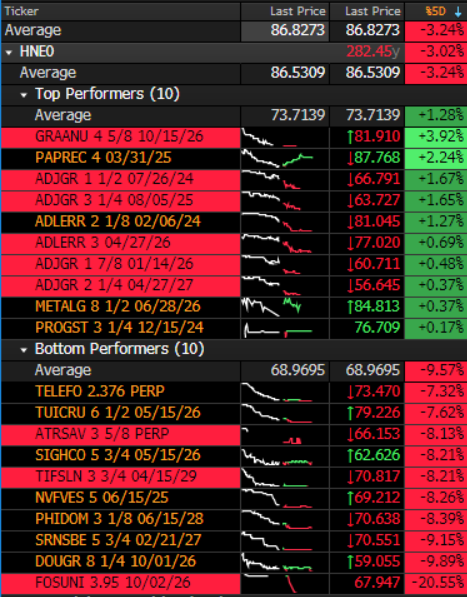

Looking at single name the list of winner is very small and populated by loosers of past weeks (like PAPREC, ADLER/ADJGR).

On loosers this week we have same names related on consumers discretionary like:

DOUGLAS and PHIDOM where there is a deterioration in operations cauded by inflation (cost of materials ans supply chain problems) + business risk in Russia and Ukraine

or more industrial names like:

SRNSBE e NVFVES impacted more by the less supportive macro enviroment for credit.

It’s all for this week. Next week maybe (if weather is good) I’ll take a break given local holiday’s in my town. So probably next week I’ll not publish the weekly recap!

Have a nice weekend and be prepared for the next week.

Bye.