Weekly Credit Market Review - Mar 04

Weekly Credit Market Review - Mar 04

A thread from macro to micro

Welcome back and while we pray for peace in Ukraine we need to analyze what happened on the land of macro and market. Let’s go.

MACRO/NARRATIVE:

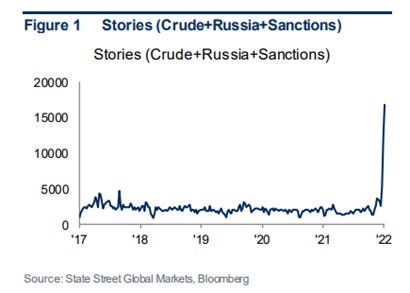

This week was dominated again by the by Russia’s military action in Ukraine. Situation deteriorated and there was an escaltion with Russia to threaten the use of nuclear weapons. US/UK/EU and all the occidental word reacted compacted and the saction on Russia have increased (like the removal of certain Russian banks from the SWIFT system and the freeze of asset reserve of Central Bank of Russia and oligarchs).

There are no sanctions on Russia energy assets (oil/gas) but investors “self sanctioned” and prefer not to buy it. Below the huge discount of Ural oil (produced in Russia) vs Brent but no buyer arrived for it.

Russia supplies ~5mbd to a global oil market which is already 1.5-2mbd in deficit this help to explain the large swing in oil and gas this week. With this increase the odds of a recession given by demand destruction and together with market now also various bank economist started to write of high inflation and weak growth, the world that nobody want to pronounce “Stagflation”.

MARKETS:

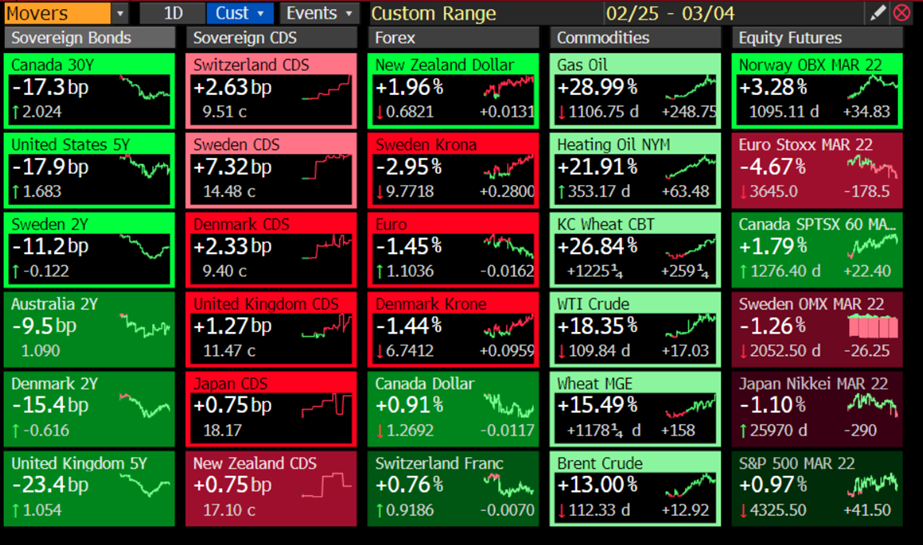

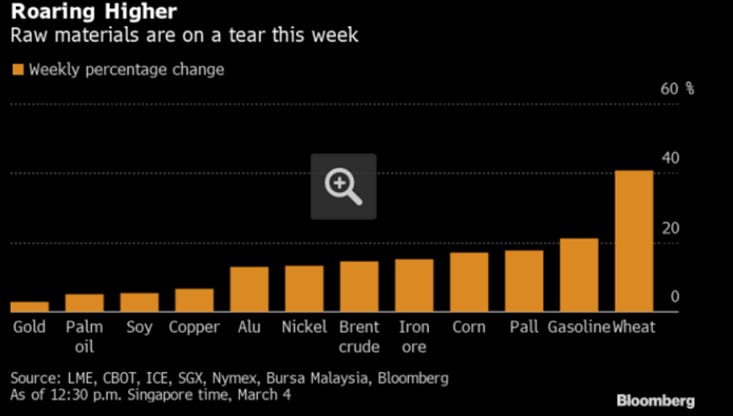

Risky asset (like credit and stocks) remained weak this week and it’s logical. The bulk of movement remain in commodities. Oil and gas prices surged reflecting risk of supply problem and more saction ahead. Wheat (and other grains) continued to be bought considering that Ukraine produced the big size of european wheat and that ports in Ukraine were the starting point of export and that Ukraine ships more than two-thirds of its annual wheat harvest and 80% of its corn.

In the stock market Europe is the most impacted (down 4% this week) being near Ukraine conflict while S&P close the week more stable. European bank stocks have underperformed dramatically given strong link with Russia in some cases. I continue to look at intermarket signals for risky assets (I know bond know a lot of economy than equity investor in 90% of cases). SPX remained muted as I said, thanks to lower real rate but the ratio of IG credit to treasury don’t confirm this view maybe looking at continued stress in funding and liquidity conditions (below the spread of FRA vs OIS swap a measure of stress in the banking sector).

Linked to funding stress in US there is also the big breakout of EURUSD after stronger-than-expected U.S. job growth that added momentum to existing haven demand for the currency.

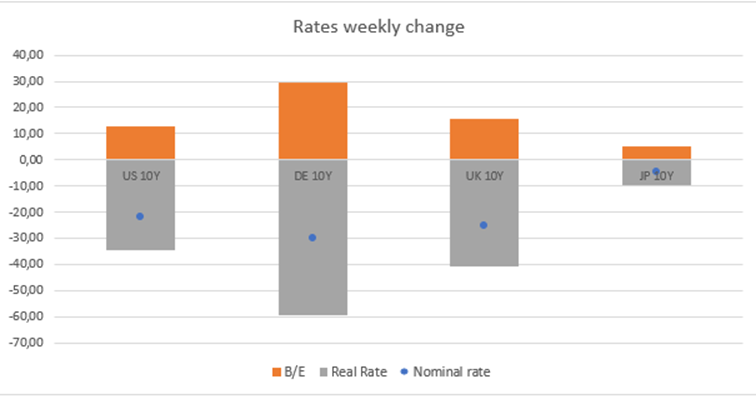

Government bond reflected the fear of less growth and short-end curve priced out some rate hikes from central banks like the Fed, the ECB and BoE while high commodities prices fired again the breakeven market confirming the stagflation scenario (given by low real yield and growth and high inflation).

In credit IG finish the week tight (thanks to a dovish ECB that could delay stimulus exit) while HY wide 30bp in cash. the message is not similar on IG and HY. Inside IG there was first signs of decompression, suggesting that downside risks to growth are starting to be priced into credit. .

..while the same message doesn’t appear in HY with the tightening of ratio of BB/BBB, implying that this same concern has not yet been priced into the HY market.

MICRO:

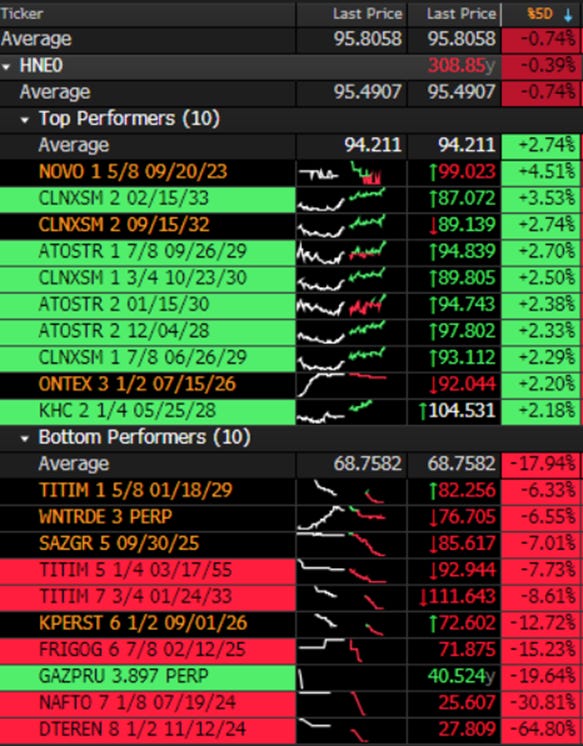

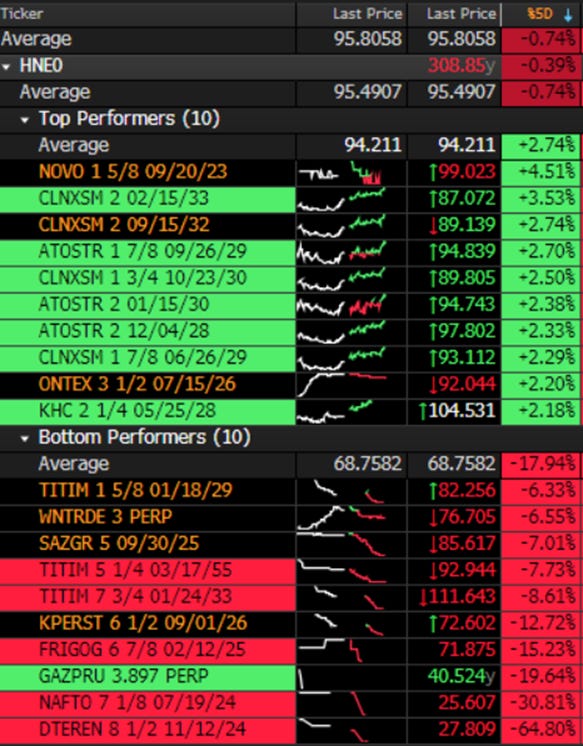

Looking at winners in single name

CLNXSM: Cellnex, after the U.K.’s CMA cleared its purchase of CK Hutchison’s U.K. towers on the condition that the Spanish company sells more than 1,000 telecom sites.

ATOSR: thanks to duration and strong BTP-bund spread after ECB dovish tilt

ONTEX: On news that top Investor GBL Said to Mull Buyout

Looking at losers there is a long list of name linked to Russia or Ukraine like:

NAFTO/GAZPRU and WNTRDE

DTEREN (Fitch Downgrades Ukrainian Corporates Following Military Invasion by Russia)

While from a fundamental point of view some more on weakness of:

TITIM: Telecom Italia reported 4Q21 and FY21 results that were in line with market consensus at the revenue level but a weak EBITDA trend given value destruction in domestic market. In FY21 revenue came in at EUR 15.3bn (-1.9% yoy, organic) and EBITDA at EUR 5.1bn (-9.6% yoy, organic). Negative reaction was associated with negative 2022 outlook that implies a 20% decline in domestic EBITDA. This will imply a rise in leverage and a probable downgrade ahead. In the presentation they confirmed their plan to separate Netco from Servco and so to go ahead alone (without KKR) with a possible merger of their network wit OpenFiber (CDP)

For this week it’s all, sorry for being too long. I hope we could write next week with better information from Ukraine. Peace!!