Weekly Credit Market Review - Mar 11

Weekly Credit Market Review - Mar 11

A thread from macro to micro

Welcome back again! An other week of war is finished and the violence of the attack is always higher than before. I continue to pray for peace or for these poor people that run away from his own country (Ukraine).

MACRO/NARRATIVE:

Sentiment and narrative continue to be driven by the newsflow related to war in Ukraine. In one week stocks market had one of the worst day in history together with one of the best bounce. In fact Russia’s attack to Ukraine continue with a lot of deaths in civils population, while some positive opening appeared on the diplomatic front:

PUTIN: CERTAIN POSITIVE SHIFTS IN TALKS WITH UKRAINE: IFX

While from an economic point of view there is a continue retaliation between EU/US/UK/JAP and Russia with a ban on import of oil/uranium by the first one (at least United States and Uk) while Russia banned export of some key commodities. Clearly this impact inflation outlook.

Inflation that was the key driver of the ECB's decisions yesterday (10 March) that in their economic outlook upgraded strongly inflation expectation and reduced only slightly growth expectation (welcome on the stagflation camp). With this scenario in mind announced a faster reduction of asset purchasing program:

with PEPP (pandemic related program) to end in March;

a reduction in APP to 40bn in April, 30bln in May and 20bln in June (with the aim to conclude in 3Q also this program).

This give them the possibility to rate hikes in September yet.

While they remarked always their flexibility and their data dependence policy this was a hawkish tilt.

MARKETS:

Looking at market movements together it seems that war fears dissipated.

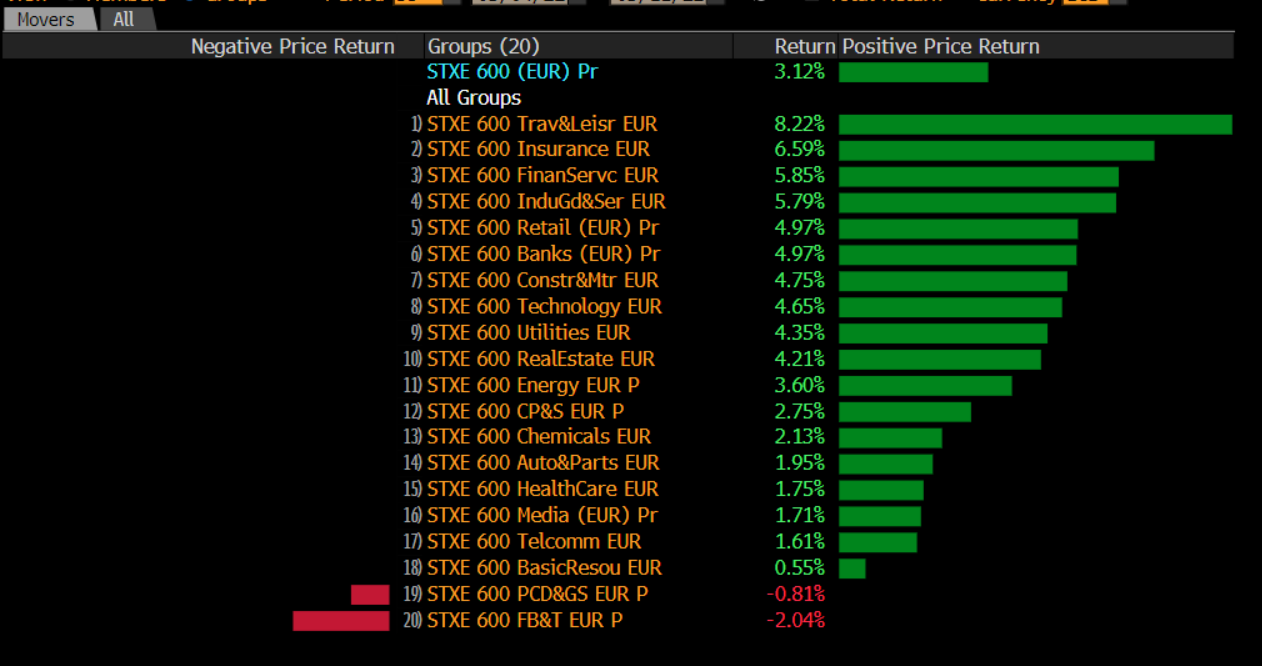

In fact, despite the high volatility, equity markets were mixed with SXXP Europe up +3% while SPX Us down -2%. Almost all sectors in Europe had a big rebound, being impacted a lot in the past one and cyclicals/defensive ratio closed in favour of most cyclicals sectors.

In commodities space optimism regarding talks between Russia and Ukraine, ban on oil import from US together to fear of some demand destruction weighted on energy sectors (Oil -6%, Gas in Europe -40%, Gasoline -8%) and on wheat (-8% on average).

On Wheat I continue to be positive. Fundamentals remain strong (on demands and on supply). Beyond the supply problem related to Ukraine ports impacting this year crops, the big problem will come on next season crop given:

Ukrainian spring planting increasingly likely to face severe disruption (all country is under war);

High fertilizer prices for the rest of the world (given by high gas prices and exports ban by Russia of ammonium nitrate

But the commodity winner of this week (almost for me) is Uranium, given White House considering sanctions on Russia’s state-owned atomic energy company, Rosatom.

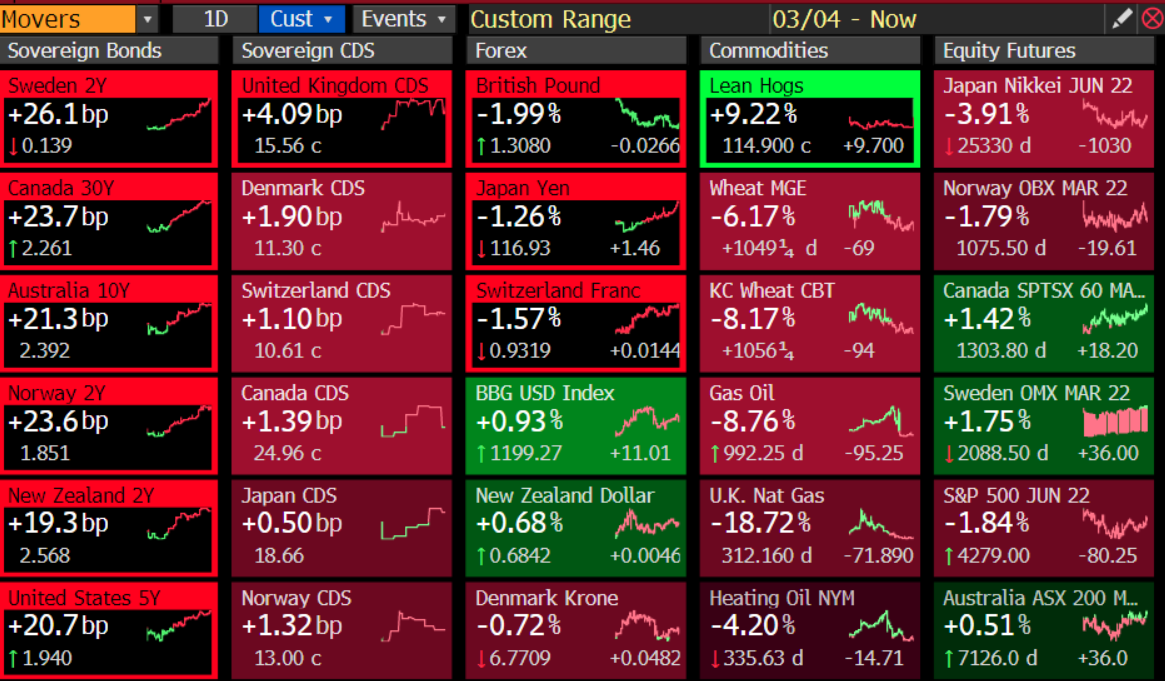

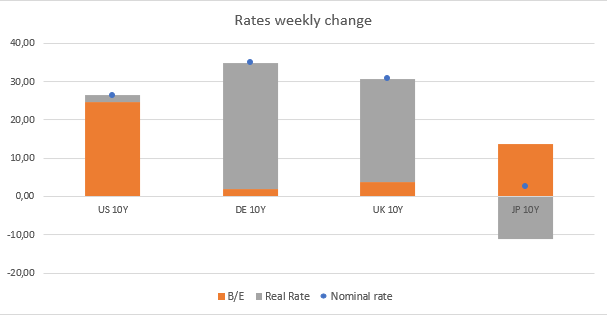

Passing now on bonds rates increased in US driven by breakeven, while in EU driven by high real rates (given positive news regarding war). Short term part of the curve repriced a lot after ECB hawkish tilt (now curve price 4 hikes before the end of the year). Overall curve flattened.

But credit market is not buying this optimism with spread widening 11bp in IG while tightening of 8bp for HY cash. Syntethic index (CDS) remained more volatile. Overall the total return this week continue to remain weak.

I continue to be not so optimistic on risky asset and I continue to look at internal of bond market for a signal. This bounce in HY ETF (in orange below) is not confirmed by my IG vs Govt ratio (in white). Financial condition are impacted by less liquidity by central banks (the best macro indicator)

"It's liquidity that moves markets.” Druckenmiller

At the same time Xover to Main ratio (HY vs IG) remain tight given low growth / high inflation scenario.

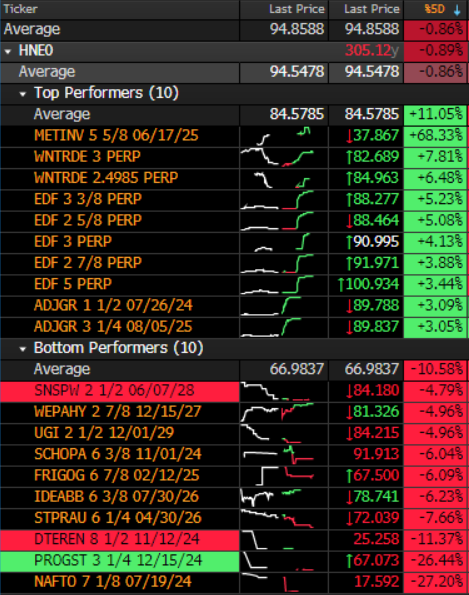

MICRO:

Performance continue to be driven by macro (growth - impacting more high beta name like B/CCC and rates/liquidity - impacting more defensive names like BB-high duration bond).

Looking at the winner of this week we find:

the losers of past weeks WNTRDE (given link with Nordstream 2), METINV (bouncing from 20 to 37) and ADJGR

EDF perp bonds after a report that France could considers nationalization (not confirmed)

KPERST (moving high today +6%) after rather reassuring trading update of the firm. Above all, company saying "strong process on pricing actions" (Thanks to @KillinGswitCH98 Pete Sampras for this)

Looking at losers we have:

NAFTO (Ukraine gas operator) and DTEREN (Ukraine renewable operator);

PROGST (an italian paper producer that halted production due to high energy costs). The issuer is high leveraged and big problem (CCC rated) but be prepared with this type of newsflow.

I know I was again too wordy!

Have a great weekend, praying for peace!