Weekly Credit Market Review - Mar 18

Weekly Credit Market Review - Mar 18

A thread from macro to micro

Welcome back and thank you to the new subscribers. Go immediately at what happened this week!

MACRO/NARRATIVE:

The crisis in Ukraine remains the focus for the market and we had some headlines talking of some progress in negotiations between Russia and Ukraine. We had also a talk between US and China on this but for market the big event was the FED meeting.

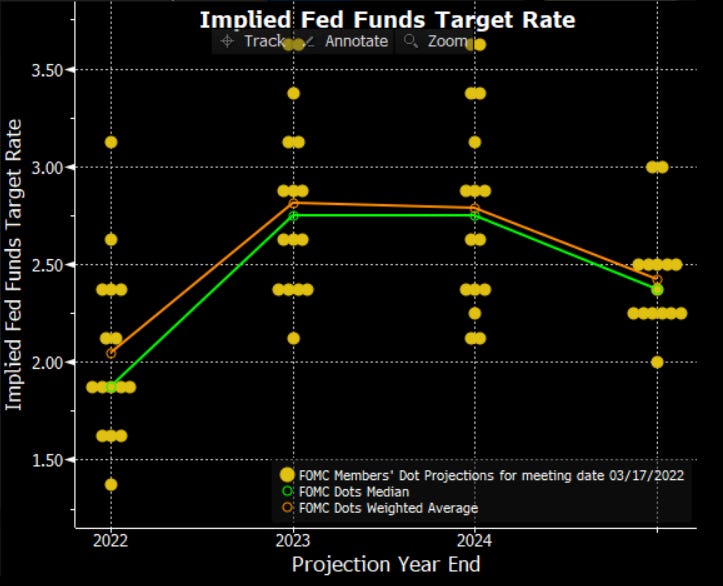

The FOMC hiked rates by 25bp at this meeting with a very hawkish statement affirming (by the dots) that they are prepared to hike:

other 6 times this year (arriving at 1.9% at year end 2022);

arriving at 2.8% at year end 2023 (with a front loading in response);

LT dots are placed at 2.375% (decreasing from 2.5%)

It’s clear that the focus of central bank is “the battle on inflation” and during the meeting the words were all regarding the strong job market and the wages pressure.

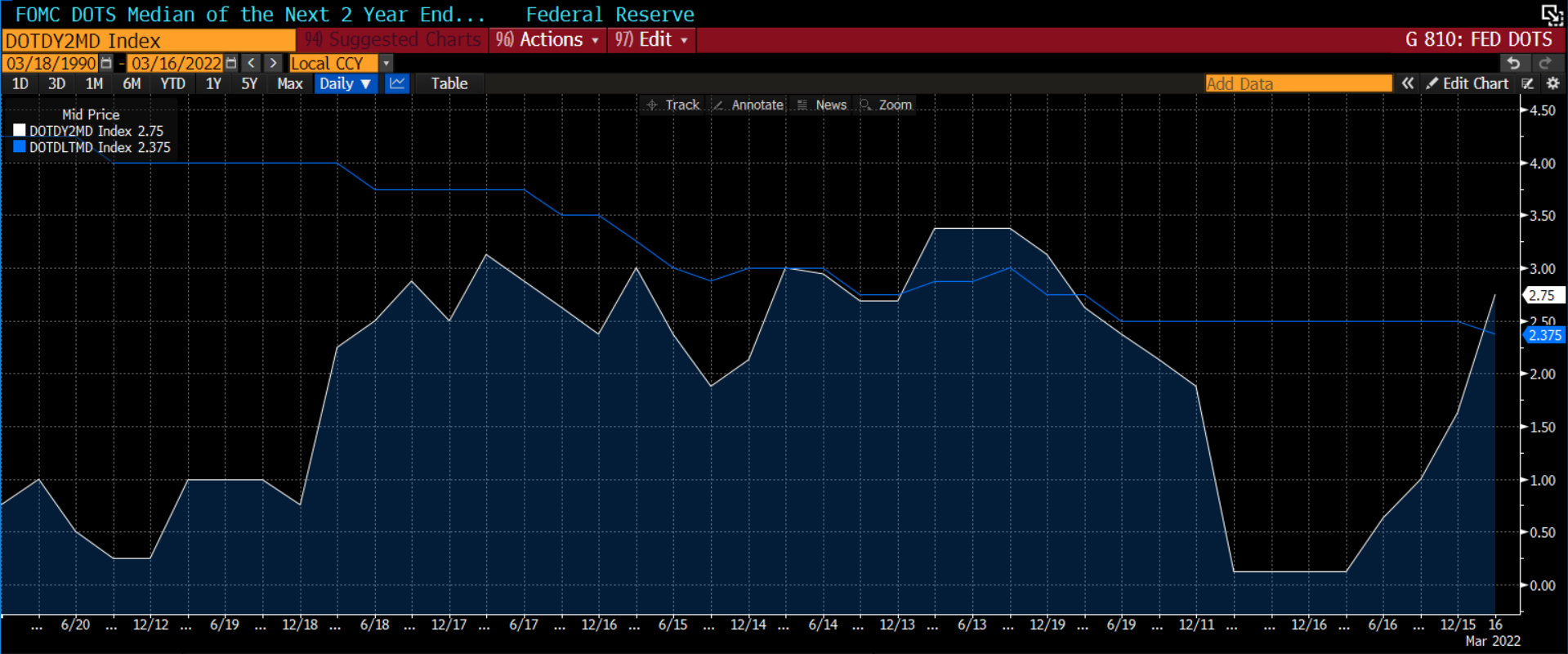

The FED thinks to do it without impacting growth but this will be difficult with the average of the next 2 years rate above neutrale rate (above the blue line is the long term dot plot).

MARKETS:

Hawkish central banks (this week also BOE hiked rate from 0.25% to 0.75%) mean higher rates in the govies bond markets. Curve around the worlds continue their flattening movement continuing to pricing the risk of “stagflation” or “lowgrowth-flation” despite the flat curve maybe impacted by the huge central banks purchases programs of the last years.

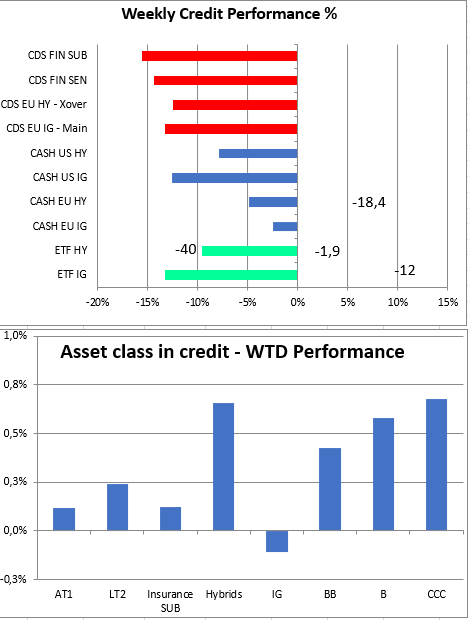

Stock markets rebounded all the loss suffered since the start of russian invasion in Ukraine and also credit markets had a great week (IG -2, HY -18bp this week) with all asset class less than IG having positive total returns.

To gauge the possible duration of the rebound in risky assets (equity and HY) I continue to monitor the impact of financial condition on credit and this week the ratio of IG to Govt (calculated using ETF) remained flat despite high rates (this is a good indicator).

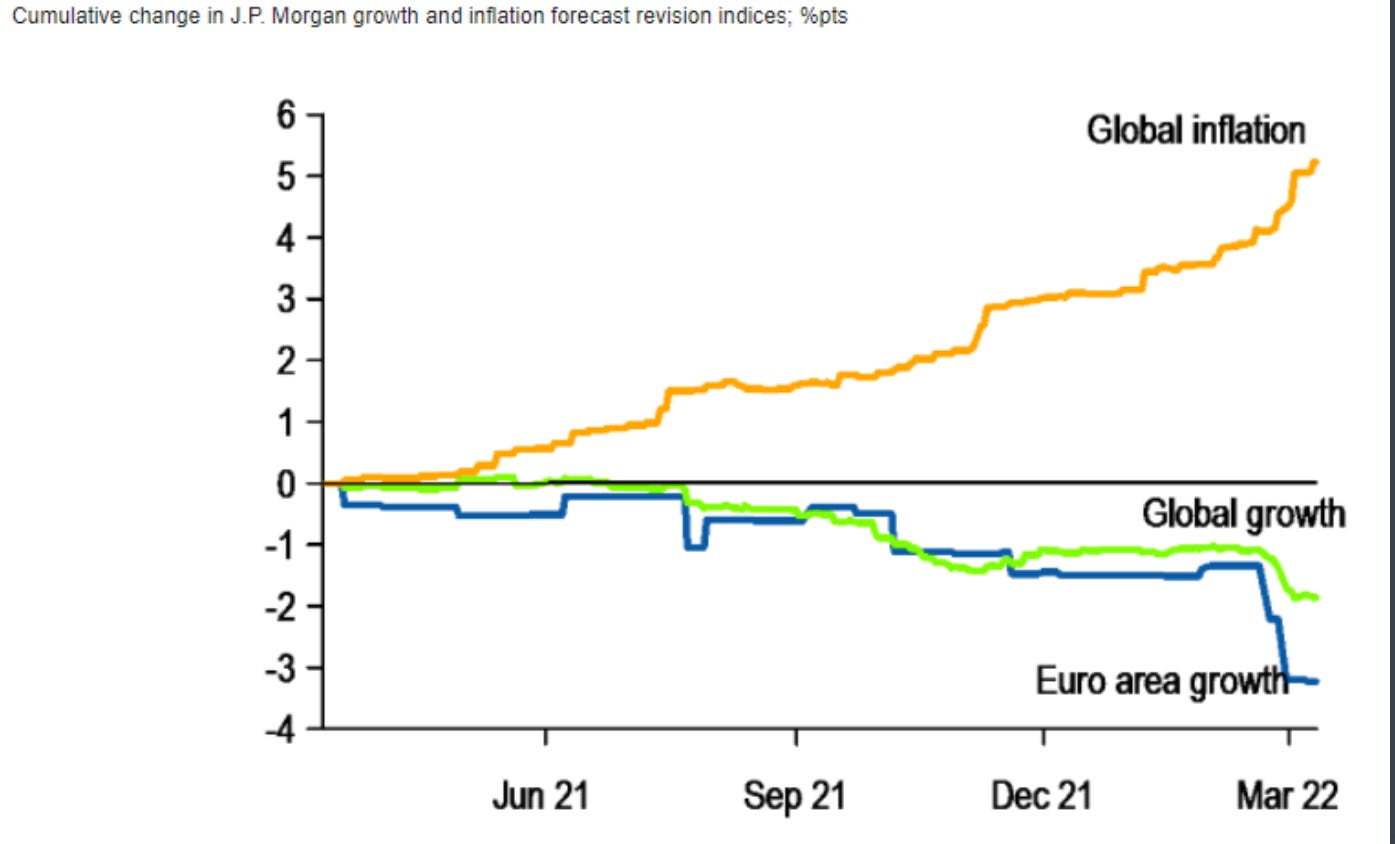

But financial conditions (driven by liquidity and credit impulse) continue to weight on possibile path of economy (below a chart from @AndreasSteno) and as showed above (with the ratio of HY to IG that remain at low level) HY is not taking it in consideration.

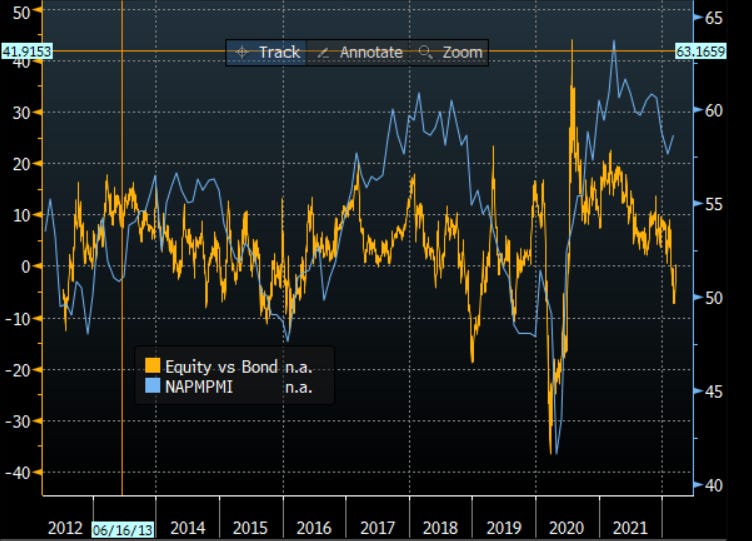

For this reason I continue to see only value in IG at the moment and in HY looking only at sectors with high margin, able to absorb high inflaction (remember that stagflation is one of the scenarios we have in front of us). The positive thing is that equity (above the SPX expressed as a ratio of performance vs govies) in yellow price a low level of ISM/PMI yet.

MICRO:

This week almost all the winners are linked to Ukraine/Russia war:

NAFTO/METINV/DTEREN russian or ukraine names (nothing to add);

PROGST (paper production come back online this week

KPERST continued the rebound after reassuring statement showing ability to pass the high costs

It’s all for today and for this week. Have a great weekend continuing to pray for peace!