Weekly Credit Market Review - Mar 25

Weekly Credit Market Review - Mar 25

A thread from macro to micro

Welcome back and thank you always to the new subscribers. Let’s go immediately at what happened this week!

MACRO/NARRATIVE:

There was little new news this week, so market continued to focus on hawkish central banks and on geopolitical risk around Russia/Ukraine conflict.

On the first point, some FED voters expressed that their most important goal is to bring down inflation. Bullard (an hawk) has pushed for 50bps in the next meeting and market give him green light.

At the same time some macro indicators: IFO in Germany (below) and consumer confidence in Eurozone started to show some pressure from war and high gasoline prices).

While on the geopolitical front Russian forces continue to loose momentum on their attack (after 1 month of “special operations” ) and today some news like this one:

RUSSIAN DEFENSE MINISTRY SAYS MAIN TARGETS OF FIRST PHASE OF #RUSSIA'S OPERATION IN UKRAINE ARE COMPLETE - TASS - RTRS

RUSSIAN DEFENCE MINISTRY SAYS WAS CONSIDERING TWO OPTIONS FOR ITS 'SPECIAL OPERATION', ONE WITHIN DONBAS SEPARATIST REPUBLICS OR OTHER ON WHOLE TERRITORY OF UKRAINE -IFAX

At the same time Putin started to ask payment on gas supply before in Ruble, in Euro, in gold or in Bitcoin for "FRIENDLY COUNTRIES".

MARKETS:

Rates markets continued to be more concerned with normalization of centrals banks policies amid higher inflation than with the war in Ukraine (and their impact of growth, based on historical relations 10% increase in oil has impact of 0.4% on inflation and -0.1%/0.2% on growth). This pushed 10y in US and on Bund respectively to 2.48% and 0.50%.

On commodities, energy is the big movers of the week, given:

geopolitical risks (some minute ago: Massive Fire at Aramco Facility in Saudi Arabia's Jeddah following reported missile strike);

Low inventories in US (and lack of production of diesel in Europe)

High demand given support on spending (tax cut on gasoline) by some countries

On equity risk-on prevailed this week, with S&P up 2.8% (is equity an inflation hedge despite higher rates?), Nikkey strong given weak yen and strong performance in commodities producers countries (Norway and Australia).

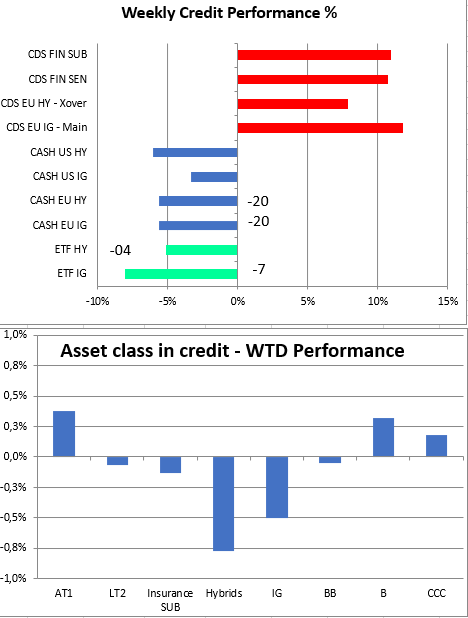

In credit markets were range-bound this week amid little new news. CDS widened for a roll effect and remained stable, while IG and HY in cash tightened 20bp thanks to solid technicals, with a lot of cash on sideline.

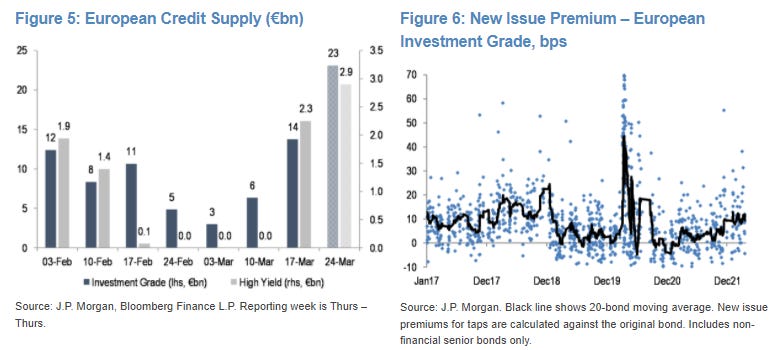

There was also a strong primary market with €8.5bn of supply (and a return of high beta name too, like the AT1 of Intesa). Demand was strong and issuer remained conservative with a good NIP.

MICRO:

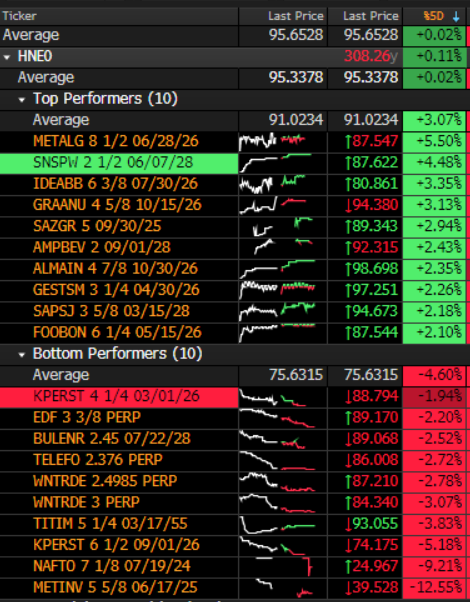

Some yo-yo market this week with loosers almost all linked to Ukraine/Russia war:

NAFTO/METINV russian or ukraine names (nothing to add);

KPERST some profit taking after rebound

TITIM due to long duration, downgrade by rating agencies and private equity confirmed interest on the name

In the winner camp we have:

GRAANU: after the business update for Q4/FY21 (y/y) showing total revenues +10% / +5% - Adj EBITDA +6% / +2.5% - Capex +€12m / +€10m - FCF (adj EBITDA - Capex) -€10m y/y / -€7m y/y - Pellet vol produced -42k ton / -0.15m ton - Pellet vol sold +68k / +0.19m

STADA (SAZGR): Stada FY21 results: - Group sales +8% y/y - Adj EBITDA +4% y/y - Adj EBITDA margin -80bps y/y - FCF +290.4m, net CF +260.5m (vs +60m FY20)

And other strong reporting name like ALMAVIVA (ALMAIN) and AMPBEV

It’s all for this week, respect the macro and investigate the micro!

Have a good weekend!