Weekly Credit Market Review - May 06

Weekly Credit Market Review - May 06

A thread from macro to micro

Welcome back and thanks to new readers. This week I have some problems with charts here in Substack so I’ll link some charts I posted on twitter. Sorry for the that!

This week the only game in town was central bank meeting, so let’s look at what happened!

MACRO/NARRATIVE:

This week we had the long awaited FOMC meeting. Powell and FED hiked 50bp in line with consensus (but talked down the potential 75bp hike, taken dovish by investors) while “confirming” other 50bp in each of the next 2 meeting (in June and July). There was also confirmation of the start of QT (reducing treasury and MBS on balance sheet) staring from 47.5bln at month and arriving at 95bln. I have no doubt that Powell it’s ready to kill economy to beat inflation. They will do it with tight financial condition. This mean a lower equity market to reduce wealth effect. Forget about FED PUT and welcome to a FED CALL environment (a return to pre-2000 world where central bank policy was driven by inflation).

This mean the end of the negative correlation between bond and equity and it’s not a case that risk parity funds and 60/40 theories borned and growned in popularity in that period.

There was also BOE meeting with 25bp hike (in line with consensus) but, while FED focus words was on “inflation” and strong job market, the Bank of England was more worried on potential growth impact in the future and on risk of stagflation.

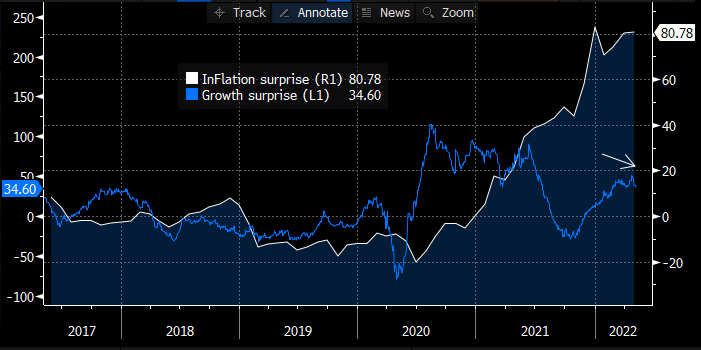

I think that in the next weeks there will be a continue battle between this two forces (growth/downside and inflation).

MARKETS:

While there was some volatility around FED meeting (rates down, equity up, dollar down) with market reading it as dovish in the first 24h, the next day the trends resumed as usual:

Rates up around the world (treasury 10y and bund 10y reached 3% and 1% respectively);

Credit market suffered both from high rates (IG widened 6/7bp) and from growth risks (HY cash widened 35bp) and undeperformed CDS;

Equity suffered from the negative trifecta of low liquidity, risk aversion and negative technicals (price action is weak, trend is lower, and breadth favour defensive/energy name vs cyclicals);

So overall some markets starting to look at growth risk and trying to balance it against the inflation risk.

MICRO:

From a micro point of view I’d like to talk also of the return of new issue on the HY market. Two issuers:

BIOFARMA GROUP MARGIN PRICE TALK: E+575bps. A B3 rated name with small scale and short track record with high exposure to Italy. The business model is defensive being a leader in uropean nutraceutical. LBO based transaction.

LA LIGA (which issuer is controlled by CVC Capital). Rated BB3 the main business is to organize and promote football competitions in Spain. The main revenues comes from sponsors and TV rights with low fixed cost (so a good visibility of cash flow).

Regarding secondary market the big losers are linked always on ADLER, the bonds of the group are -15% on average this week on more questions regarding loan disclosure. S&P downgrade the group and the operating company to CCC with negative outlook.

Other names with negative performance are CANPACK 27 and NVFVES 25 (two cyclical name with high impact from high commodity) but no specific news on both.

The list of winners is very short this week and I’ll pass writing on this.

Thanks for reading Credit from Macro to Micro! Subscribe for free to receive new posts and support my work.

Have a great weekend!

interesting post, the "Powell will kill the economy to beat inflation" is a bit of simplistic argument. In 3-6 months the Fed will be looking at an economy that has rapidly slowed. This has already happened even before the hikes. Growth and inflation will go hand in hand (the demand side of it) and in time rates start pricing rate cuts. BBB IGs, and defensive BBs are good adds here.