Weekly Credit Market Review - May 13

Weekly Credit Market Review - May 13

A thread from macro to micro

Welcome back and thanks to new readers. Just a not of service, if you like my recap please subscribe below and share it. We have a lot to talk so let’s go.

MACRO/NARRATIVE:

The most important event of the week was the CPI release of April in USA. A lot was written about this and how the market arrived at the event almost sure of a weaking of inflation print.

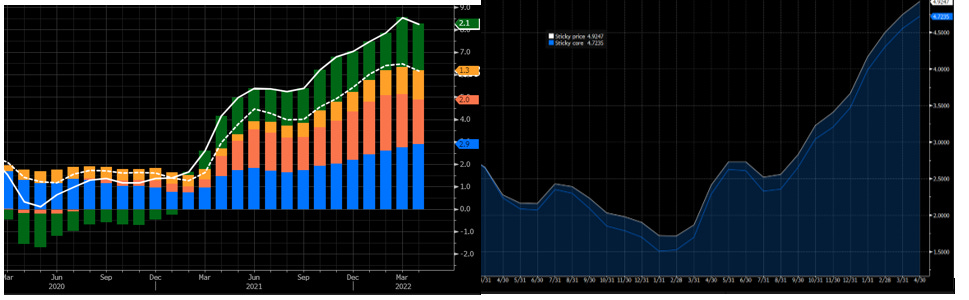

The April print was, effectively, below March (with YoY decreasing from 8.5% to 8.3% and MoM from 1.2% to 0.3%) but it was above expected.

Below the surface a big contribution arrived from services inflation (airfreight specifically) and from shelter (the equivalent rent). The increase of services is in line with expectation and a switch from goods to goods (after reopening due to covid).

Energy inflation decreased too (thanks to base effect of oil and gas prices) but a worry thing to consider is the increase in sticky prices (both in headline and in core). This part is the most difficult for central bank to reduce and that could increase the risk of wages/inflation spiral.

During the week various members of FED returned to talk :

Fed’s Bostic Says No Need to Move Faster Than Half-Point Hikes

Fed’s Barkin Declines to Take 75 Basis-Point Hike Off Table

Powell reaffirmed the Fed is likely to raise rates by a half point at each of its next two meetings and isn’t “actively considering” a 75 basis-point move.

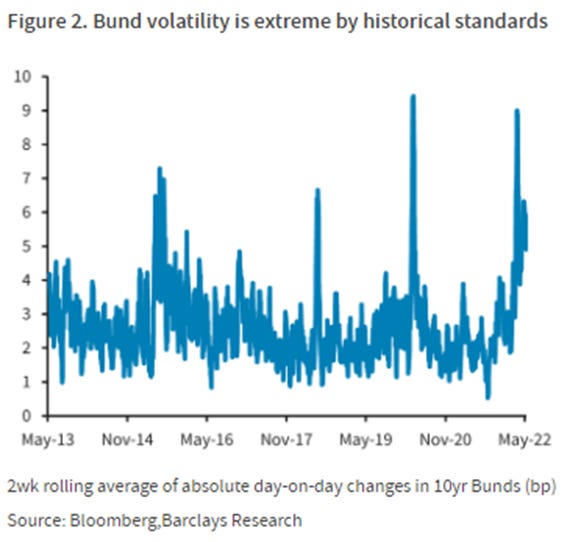

This doesn’t help to reduce volatility of the market, especially that one associated with rates market that remain high vs history and other markets too.

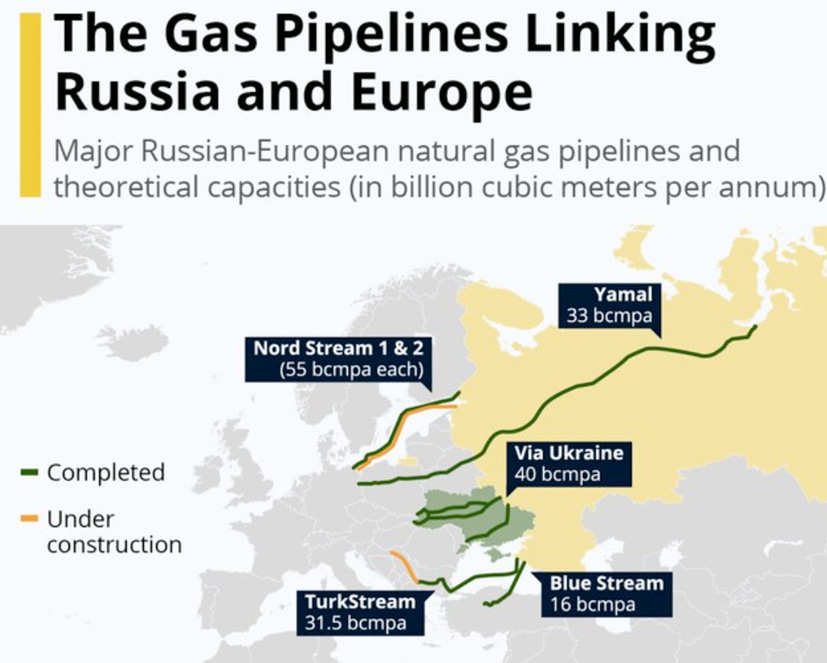

During the week, Ukrainian Transit Operator OGTSU annouced force majeure on gas deliveries from Russia to Slovakia due to damages of facilities in occupied territory which cannot be accessed for repairs. At the same time geopolitical risk continue to remain high with Finland trying to applying to enter NATO, and Russia has said it will be forced to take "retaliatory steps" (like weaponizing gas to Europe?)

H/T of chart below @BurggrabenH

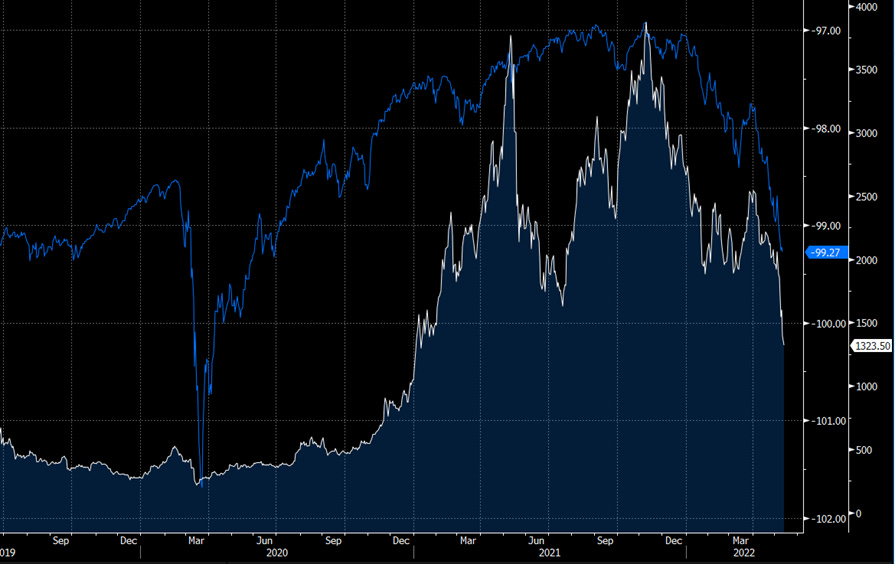

And finally we have the crypto bloodbath. What happen when total liquidity (that helped to increase value of any financials asset, that created bubbles and meme manias) start to decrease?

Easy to say looking at financial condition by GS Index (in blue) vs Crypto index (in white). It’s the same story on high growth companies, with investors happy to pay high multiples for futures cash flow, in a period of low rates.

MARKETS:

Market appears to be tipping from a high-inflation to a weaker-growth narrative. To be honest some piece of market were more worried about this:

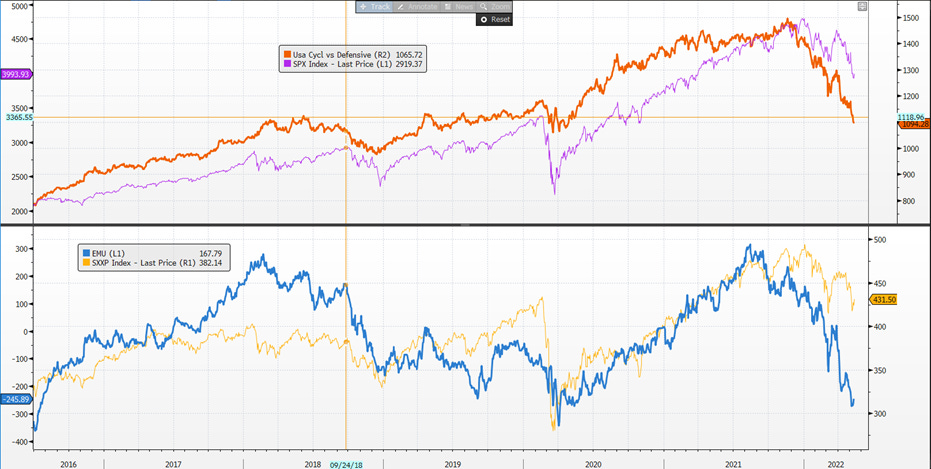

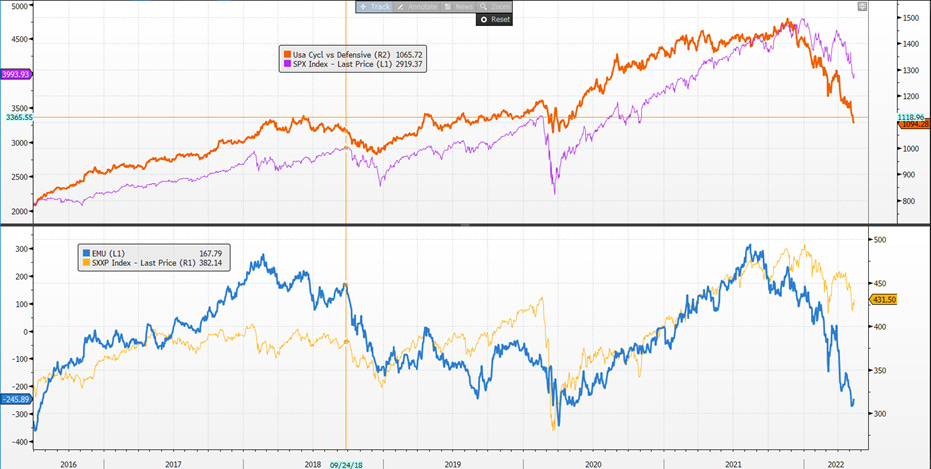

Internal of the equity market (with cyclical defensive going down);

Commodity market going down looking at Copper to Gold or Silver to Gold

Currencies more linked to global growth like AUD e WON

It was rates that diverged from other indicators (like banks to SPX) or surprise index

This week rates turned south with a decrease of 15/20bp on average and equity market trying some bounce (the typical bear market rally).

What changed this week was a return of the negative correlation between bond and equity (with market again looking at growth downside).

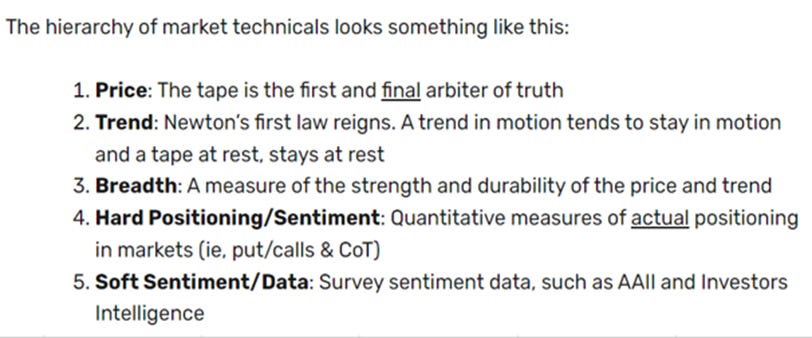

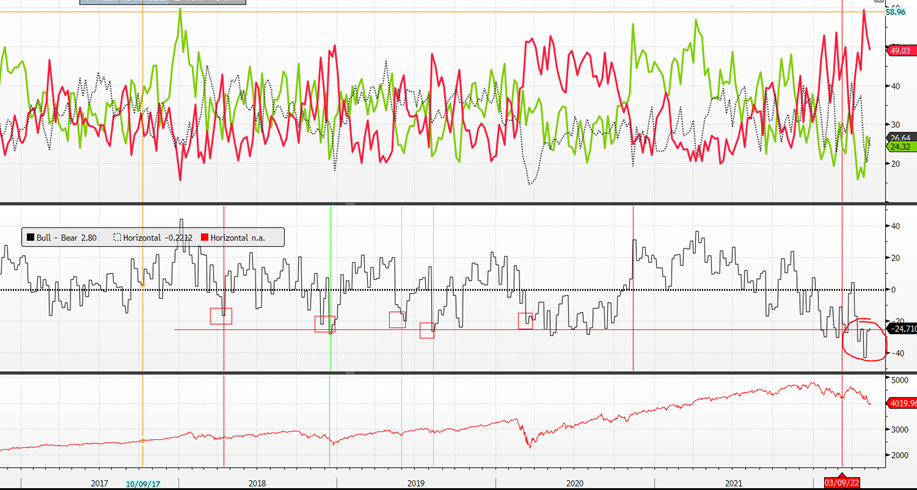

So fundamentals continue to remain weak, while from a techicals point of view the excess of pessimism (looking at AAII investor sentiment and other sentiment indicator) could help some short term rebound.

Below the hierarchy of technicals from @macroops and the sentiment indicator

In FX, given the envorinment, dollar continued to remain King.

On commodities the agriculture sector was the best sector after USDA lowered output forecast for Corn and Wheat, and expectation of Ukrainian crop 30% lower than expected.

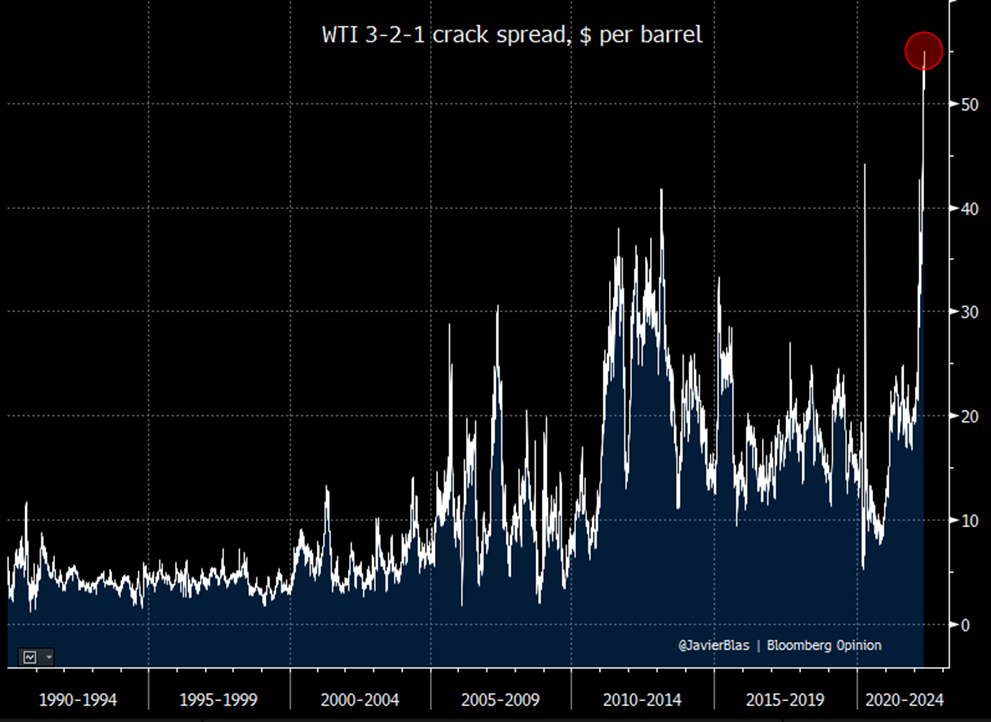

On energy sector continue the pain regarding gasoline and diesel, with low inventories of diesel on East Coast and continue record for crack spread (a proxy of refining margin) and diesel prices.

I wrote a tweet about this that you can find below, analyzing the causes. Remember consumers use refined products, not oil.

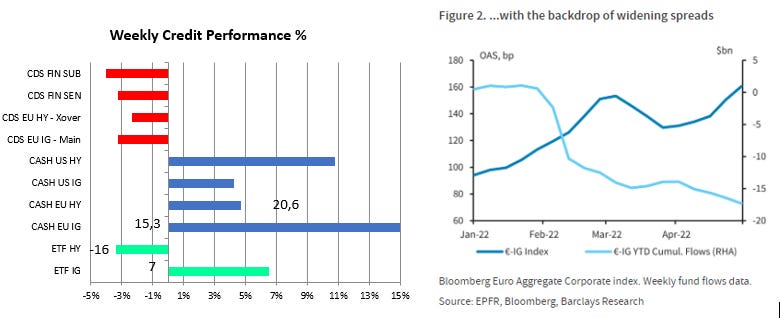

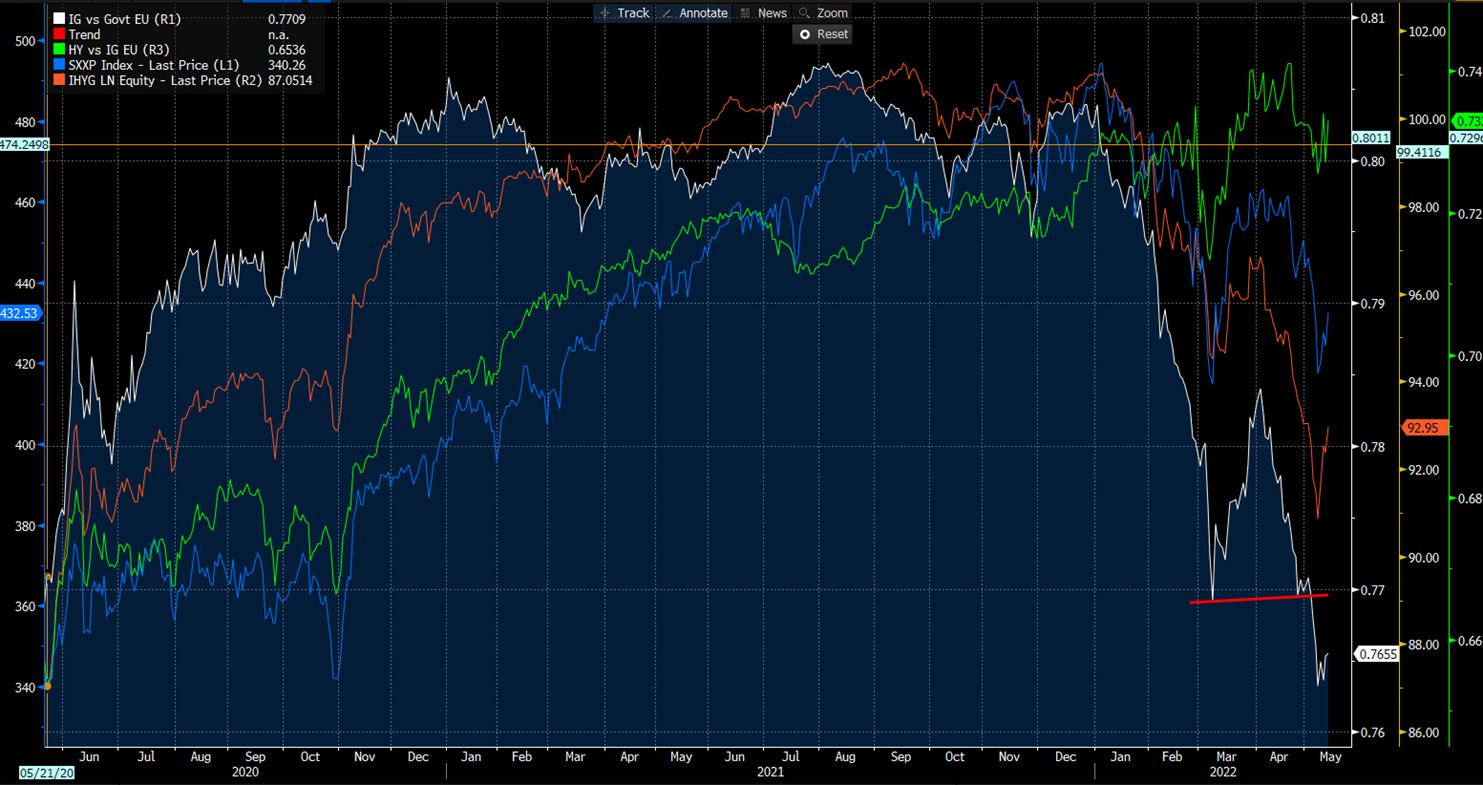

In credit, cash spread widened while syntethic tightened after excess fear. IG and HY ETF bounced in total return, and the ratio IG/Govt founded a bottom (in line with equity too).

The technicals continue to remain negative (outflow from funds given the high yield on govies, and cessation of net CSSP purchases).

MICRO:

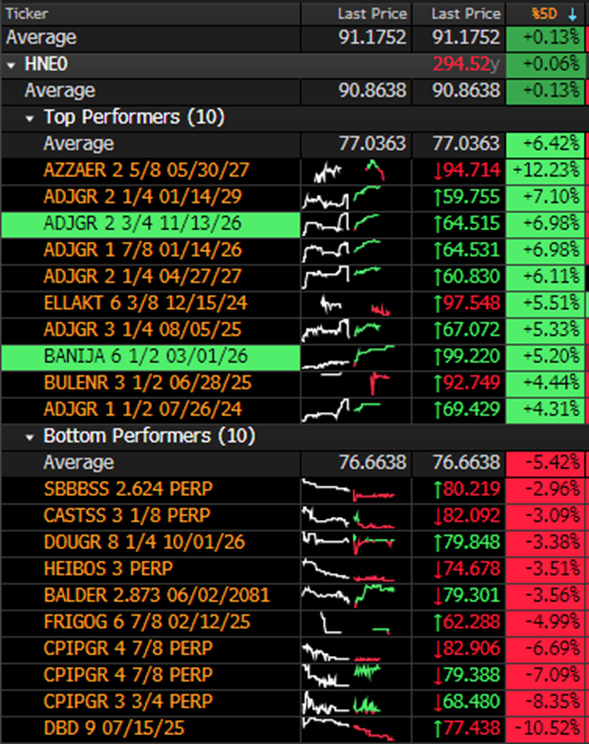

On single name I want to talk of some special situation that moved the market this week:

ELLAKTOR: together at some asset disposal Raggeborgh (the main shareholder) want to take private the company. This helped a strong rebound on the bond, on hope of a CoC;

BANIJAY: a SPAC of TIKEAU is looking to buy the company, in a deal worth 4.3bln

ONTEX: good turnaround of revenue in the report but the driver was the news that AIP could look to take over Ontex in order to merge this with an existing personal care business Attindas.

It’s all for today. Have a nice weekend!