Weekly Credit Market Review - May 20

Weekly Credit Market Review - May 20

A thread from macro to micro

Welcome back and thanks to all readers (we are arrived at 200 subscribers). If you like my recap please subscribe below and share it. Now let’s go to see what happened.

MACRO/NARRATIVE:

The week was characterized by a new weakening of global macro impulse. Surprise index were lower around the globe (especially in US). One of the most looked indicator was the “Retail sales” number that showed a beat from the past week but that was associated also with an increase in use of credit cards (not a great thing considering that strong consumer balance sheet was one of the strengths according to experts). Add also that real rates sales (adjusted for price increase) are in negative trend (below a chart of Macrobond and Andrea Steno) and with high gasoline/diesel price continue to pose the risk of demand destruction.

On the other hand we have hawkishness of central banks, that continue to be focused on the sticky inflation and high printed inflation data. ECB give a green light for hike in june/july now, maybe given the fear of weak euro impacting on inflation too.

But not all central banks are created equal. PBOC (the chinese central bank) lowered 5yr loan prime rate to support economy, to boost mortgage and loans amid property problems and covid lockdown.

We conclude with reporting season. There was a lot of talks about Walmart and Target (with Target equity down almost 25% on Wednesday, its largest decline since October 1987). The story here is linked to the fact that they were unable to pass high input cost to customers, impacting their margin (one of the biggest fear of investors some months ago).

MARKETS:

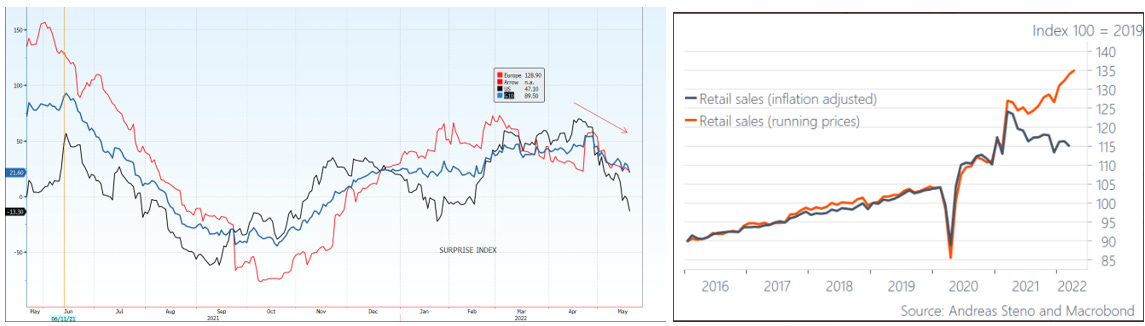

The weekly performance of equity was almost flat for SPX and SXXP but the volatility during the week was high. Rates in US and Eurozone followed risk-on/risk-off of equity, while the big winners remained commodities (with copper that after weeks of weakness gained due to the positive news coming from PBOC).

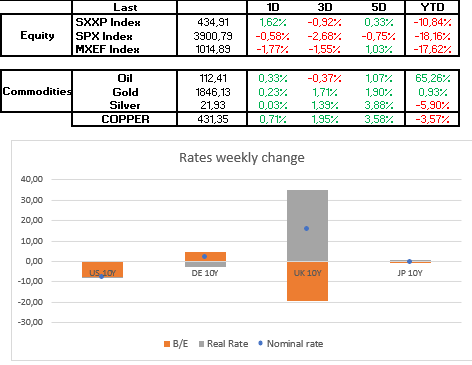

Remaining on rates (I use generally european assets, so germany 10y) I tried to investigate the different drivers (ECB policy rates using 1y1y eonia, breakeven rates, Surprise index and risk sentiment using SX5e). This illustrate the transition of market focus from inflation to a 'growth' problem (I call it the pendulum)!

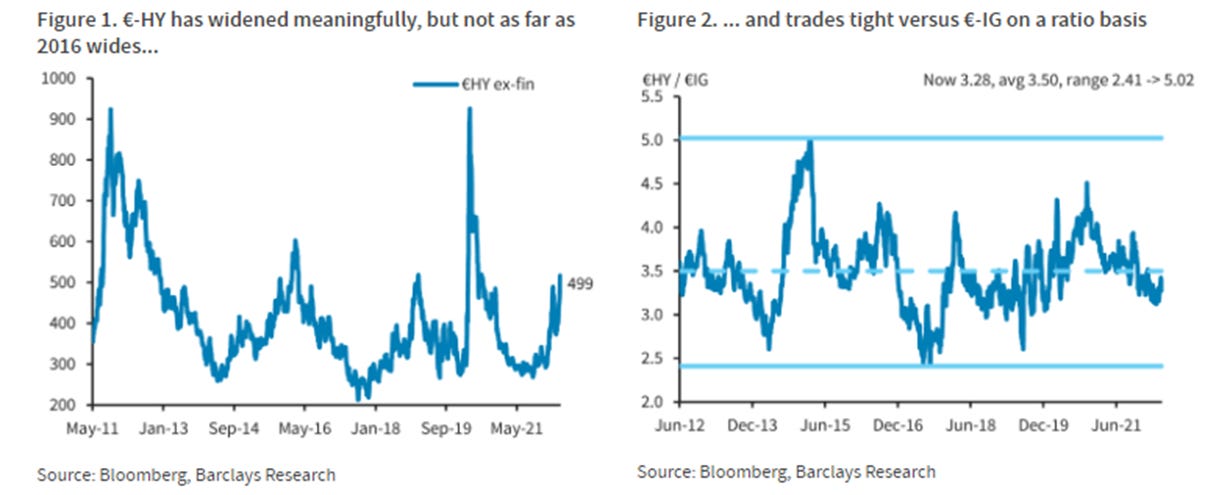

The same thing could be seen with the decompression of XOVER vs MAIN (in CSD credit index), but this remain tight versus historical wide (indicating that riskier credit doesn’t price all the growth risk we can have in the futures).

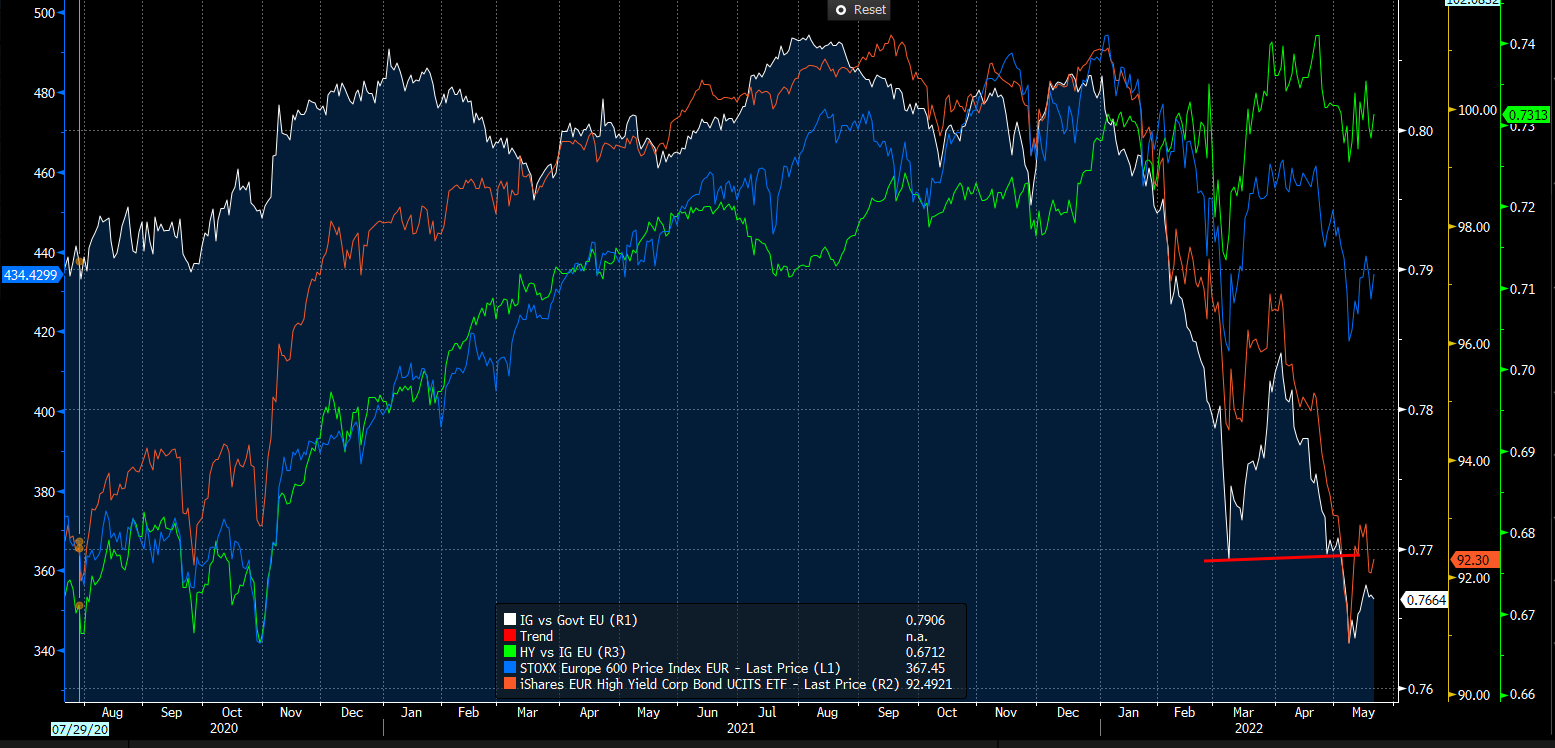

Remaining always on credit (I updated my volamix below) I noted that Vix and Vix curve (spot vs 3M) remained quite (with curve indicating no stress without inversion) but XOVER (HY index CDS) widened and followed the volatility of rates (MOVE Index).

A positive indicator here could be the fact that this could have reached a top. A stabilization in rates could be the first signal that could help to stabilize the credit (IG/govt ratio) and risky assets in general so here I am more positive on IG credit.

Regarding HY I continue to think that the risk ahead are high and market is not pricing correctly recession risk so I’ll remain cautious.

The same thing could be said for equity:

Fundamentals remain weak with low growth and low central bank liquidity;

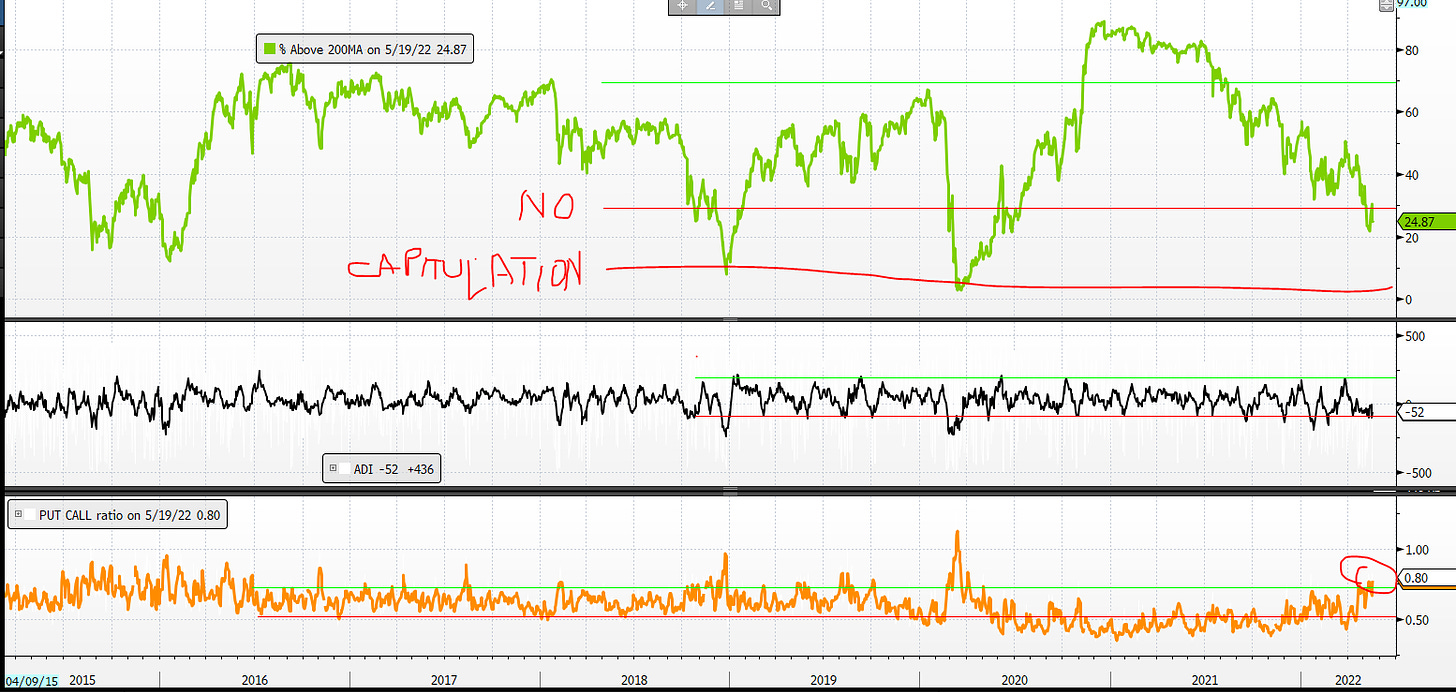

Technicals have a negative trend and price action, with an orrible breadth (below I used SPX % above 200day moving average, and ADI) but not at capitulation levels. The only positive indicator here are sentiment/positioning (below the high numbers of put vs call) that could add impetus to short term rebound.

MICRO:

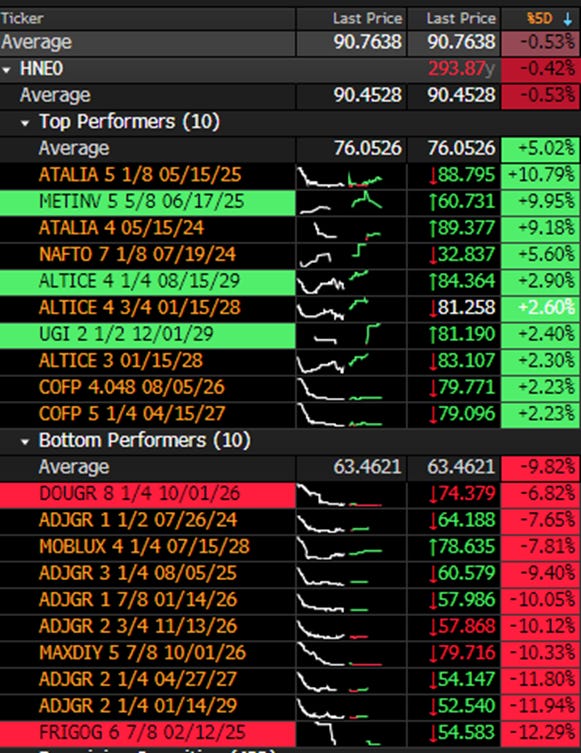

On the micro front dispersion remain low and the main driver of alfa comes from M&A or legal problems:

#ATALIAN bonds jumped +10pts after rumors of PE firm Clayton Dubilier & Rice (CD&R) was in talk to buy Servest (Atalian UK) & OCS group.

*ADLER GROUP KPMG WON'T BE AUDITOR FOR '22 FINL STATEMENT with bond down on average of -10pts

ORPEA (not on the HY index) but -10pts too on new allegations after Allegations Tied to Luxembourg Shell Company

It’s all for today. Have a great day and a great weekend!