Weekly Credit Market Review - May 27

Weekly Credit Market Review - May 27

A thread from macro to micro

Welcome back. I want only to thank you because today I reached 3k follower on my profile. If you like my job/analysis please subscribe below and share it. Now let’s go to see what happened.

MACRO/NARRATIVE:

An other week endend and narrative continue to be driven by:

high energy prices (with oil trending higher despite a chinese lockdown);

the war in Ukraine (with Russia gaining again in the south) and tension on grain exports;

the hawkishness of central banks, ready to lift rates to beat inflation (killing demand while this is a supply shock)

These started to shift the pendulum from “inflation to growth”, with the spectrum of “Stagflation” and the ’70 always around the corner. Effectively data momentum is not good (below the surprise index for US and EU).

All this consensus/narrative is explained well using last week Ackman’s tweet (no exactly a macro-man). So exactly when everyone tallks about it and panick about inflation, with the risk that central banks panick about inflation, maybe it’s the time to look at other narratives.

Ragarding monetary policy ECB published one new format: an ECB BLOG. Lagarde outlined a rationale for the ECB to turn away from a decade of aggressively dovish monetary policy and committed the bank to two interest rate hikes by September, which would bring its overnight interest rate back up to zero (effectively more hawkish, maybe trying to put a floor on EUR).

Always this week on FED Raphael Bostic, head of the Atlanta Fed, said that a pause after other two 50bp hike in rate might make sense (just to arriving at neutral rate) to have flexibilty to analyze new data and market. This represented the first hint in a dovish direction from the Fed in some months.

MARKETS:

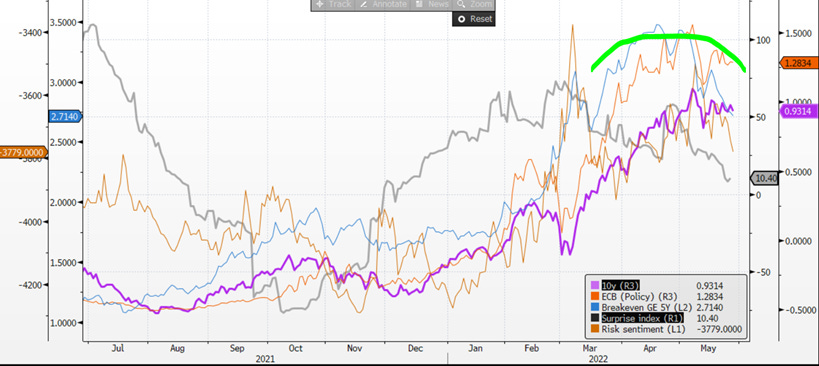

Starting from rates we had a stabilization in interest rates (both US and EU) maybe thanks to the dovish read of the FOMC minutes. I continued to look at the drivers of rates in germany and all (ECB expectation measured with 1y1y eonia, breakeven rates, surprise index) confirmed each others.

A stabilization of rates (together with a very negative sentiments) permitted a bounce in Equity (+4.5% on SPX and SXXP on average) that finded again a negative correlation bond-equity. Looking at these great chart of @aqrcapital maybe we passed from blue to sky in the bar below (from inflation to growth fear).

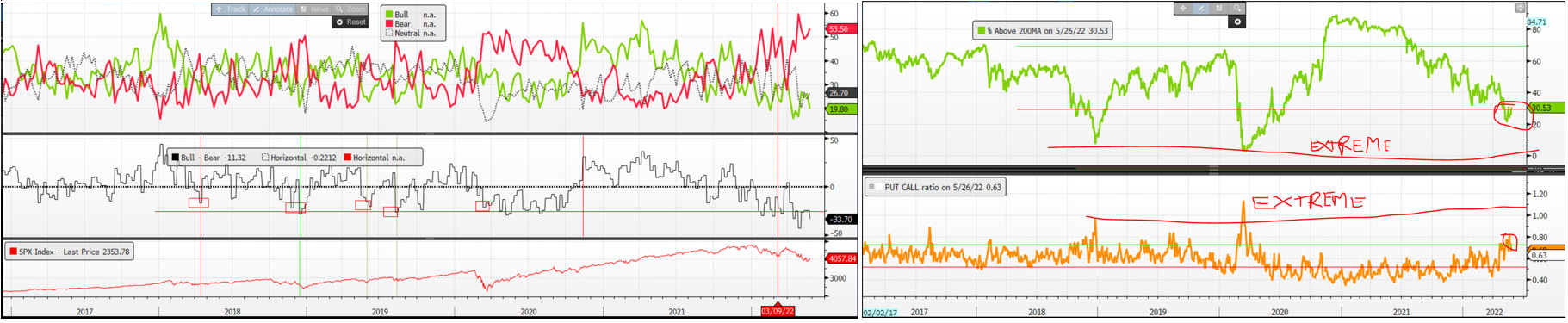

Below some sentiment indicators (AAII Bullish vs bearish, % above200day moving average, Put/Call ratio). All are negative, but not so extreme.

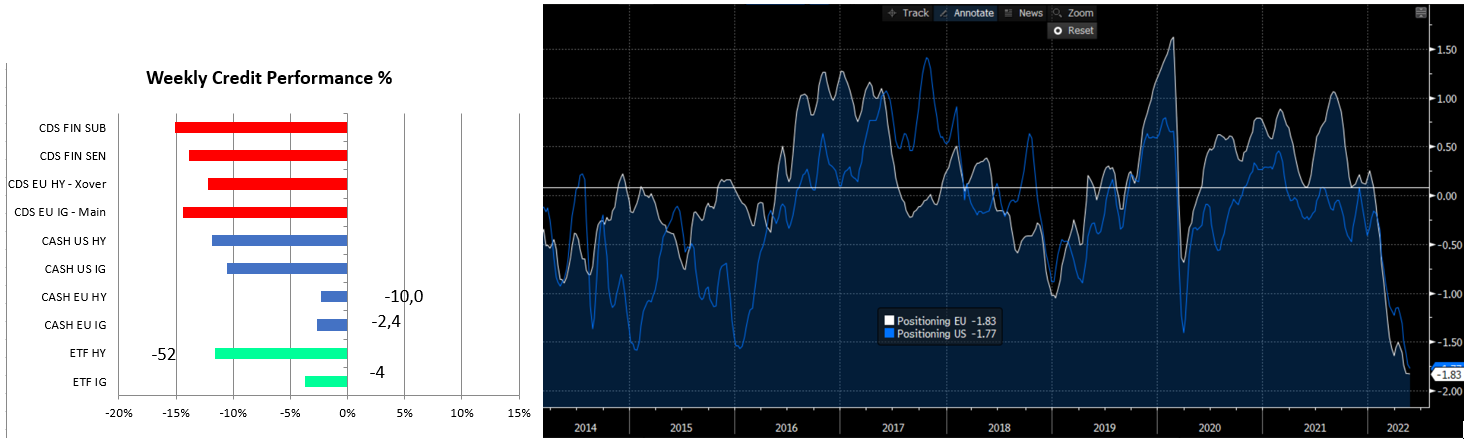

The rebound in equity, helped credit too, that had a good week with tightening in HY (15/20bp) and in IG too. Positinioning (on right the BNP index) is very short on credit (especially in syntetic) so the mix for a short term rebound (at least) was ready.

Rates and credit are the bread and butter of liquidity for market so in the short-mid term looking at internal of these give you a great info. Remember that usually bond traders (and not because I am one of them) are smarter than equity guys and once the two market diverge, in the 90% ofa cases the correction give reason to bonds.

As said before rates finded a top this week and IG/govt ratio rebounded too. Also HY ETF took part of the game (in white and orange below).

What continue to be not normal for me is the HY/IG ratio (in green below) that doesn’t follow the downside of risky asset in general and other ratio of cyclical/defensive ratio and it seems don’t price a growth risk.

Below I used HY/IG etf vs discretionary/healthcare ratio (I used a SPDR ETF for US).

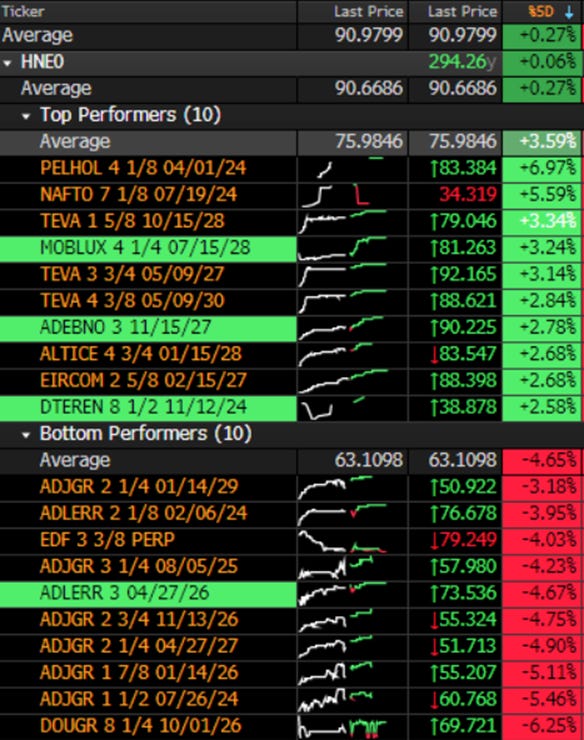

MICRO:

A good volatility this week on a great numbers of reporting (Edreams and CANPACK good for example).

LOSERS

#ADLERR #ADJGR down 4-5 pts again -- (BN) Adler Accounts Investigated by Prosecutors Over Real Estate Deal

DOUGLAS reported sales increase 30.7% yoy and EBITDA again positive to 25M in 2Q 21-2 but leverage remained elevated given ambitions on online

Winners

TEVA after opioid deal with West Virginia that removes some risks

ADEVINTA good results (EBITDA margin of 32.3%, up 70 bps vs Q4 2021, Strong cash flow generation profile, while Deleveraging priority balanced with opportunistic opportunities)

MOBLUX (Conforama), despite strong weakness of Maison du Monde equity that reduced FY forecast on expected consumer weakness (we have a very low consumer sentiment yet)

It’s all for this week. Thanks for reading, to follow me and to subscribe.

Have a great weekend, relax!