Weekly Credit Market Review - Oct 07

Weekly Credit Market Review - Oct 07

A thread from macro to micro

Welcome back at the weekly recap, as usual at the end of the week. As always if you like my job/analysis please subscribe below and share it and I remember you that I am also on twitter at @Credit_Junk. And now let’s see what happened this week.

MACRO/NARRATIVE:

This past week was quite in term of events, while from a macro data point of view we had some confirmation of weakness:

ISM manufacturing down from 52.8 to 50.9 in September (expectations for 52)

PMI Eurozone manufacturing slightly down from 48.5 to 48.4 but mixed in term of countries divergences

JOLTS (new job openings) falling but not enough to stop FED to continue tightening;

PPI in Europe for August up from 37.9% to 43.3% (yes above 40%)

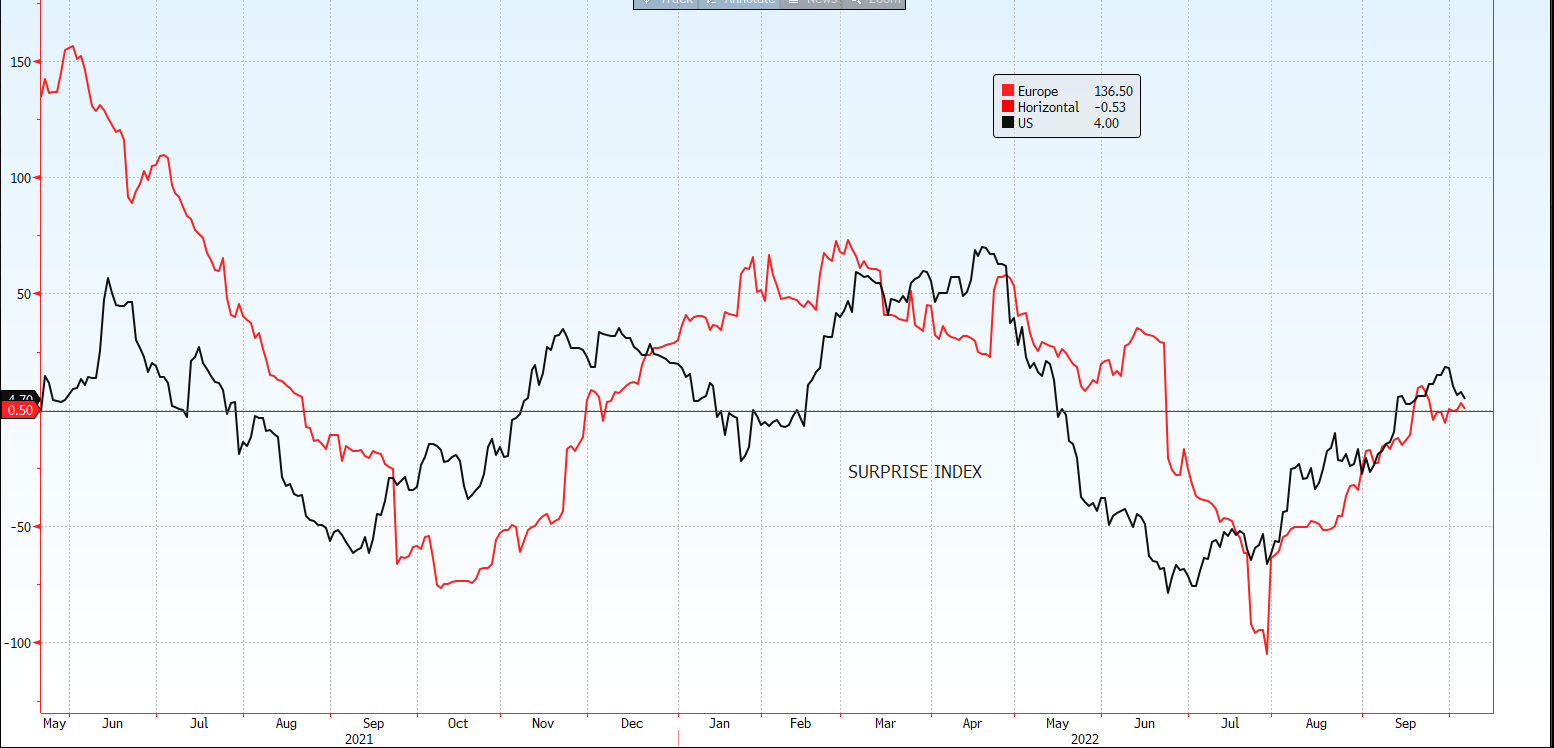

Surprise index for both area seems arrived at a local top here with renewed negative surprise ahead.

In term of newflow we had:

hopes for a central banks pivot after RBA (central bank of Australia) increasing rates only by 25bp and U.N. asking FED to slow hiking rates to not damage enough weak countries. I am not reading enough in the stop of RBA given their high weight of floater mortgage and the high link to China;

BOE lightened the buy of gilts at the long end. Attention will be next week (14th of October) when the extraordinary package will end;

OPEC+ that agreed a 2mln barrel per day cut. Given that some countries are not able to produce enough to satisfy the actual quotas (OPEC+ produce 1/1.5M bpd less than estimated), the actual cut in production could be around 880k bpd. This could be enough to balance the actual surplus of 700/800k bpd in the 3Q given the slow demand coming from China. Below the chart. This turns on the battle with US and Biden is now ready to release other oil from SPR, given the clear link between gasoline prices and Biden consensus (we have mid-term elections in 1 month).

today NFP in USA with an increase of 263k vs estimate of 255k, a decrease of unempleyment level from 3.7% to 3.5% and hourly wages at 5% in September. I think this put a stop to any hopeness of pivot of the FED.

MARKETS:

Market hopeness of a stop of central bank hike drove the market this week. Just an example below, using the twitter trend for “fed pivot” vs S&P 500 price, it’s clear how the last one is driven by central bank narrative. The market is closing the week with S&P at +2.8% and SXXP at 1.6%.

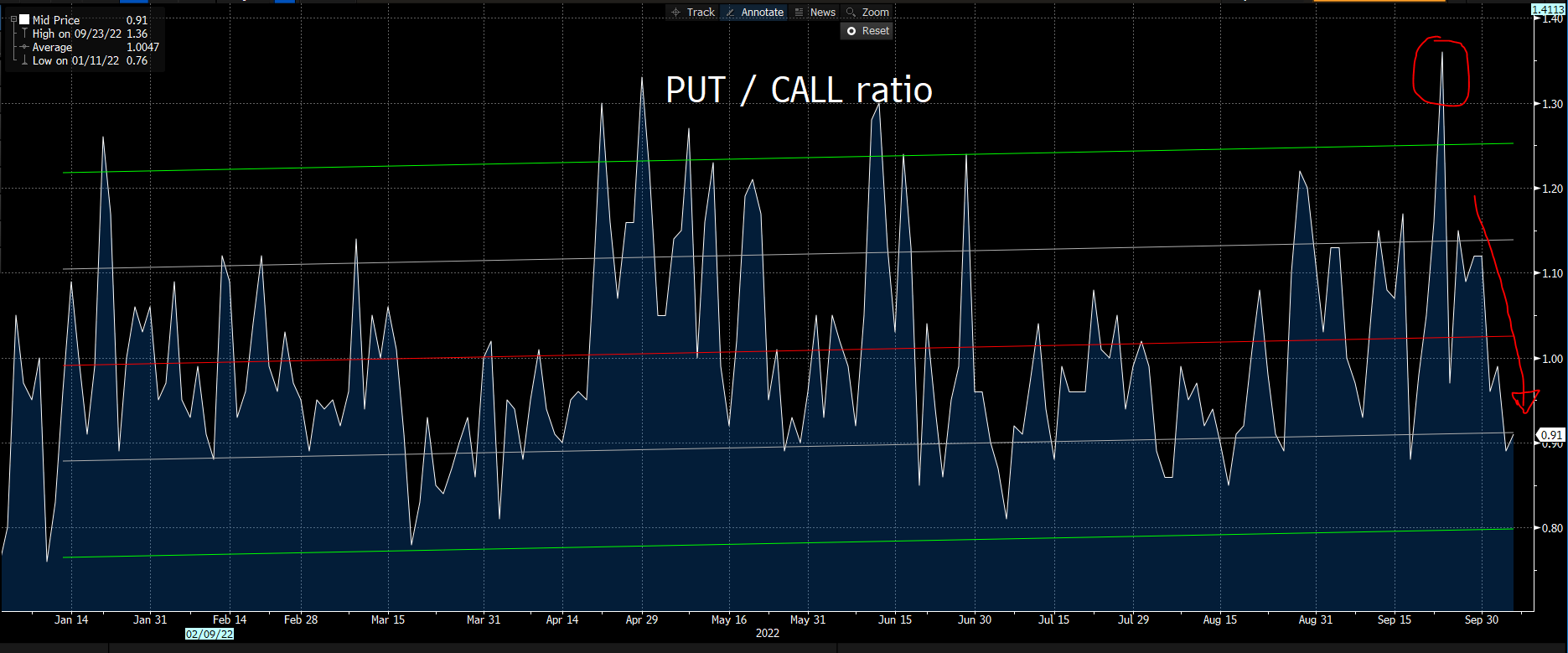

Going into the US payroll today Put/Call ratio decreased fast from a high level to a very low level (during this decrease I bought some protection via put again).

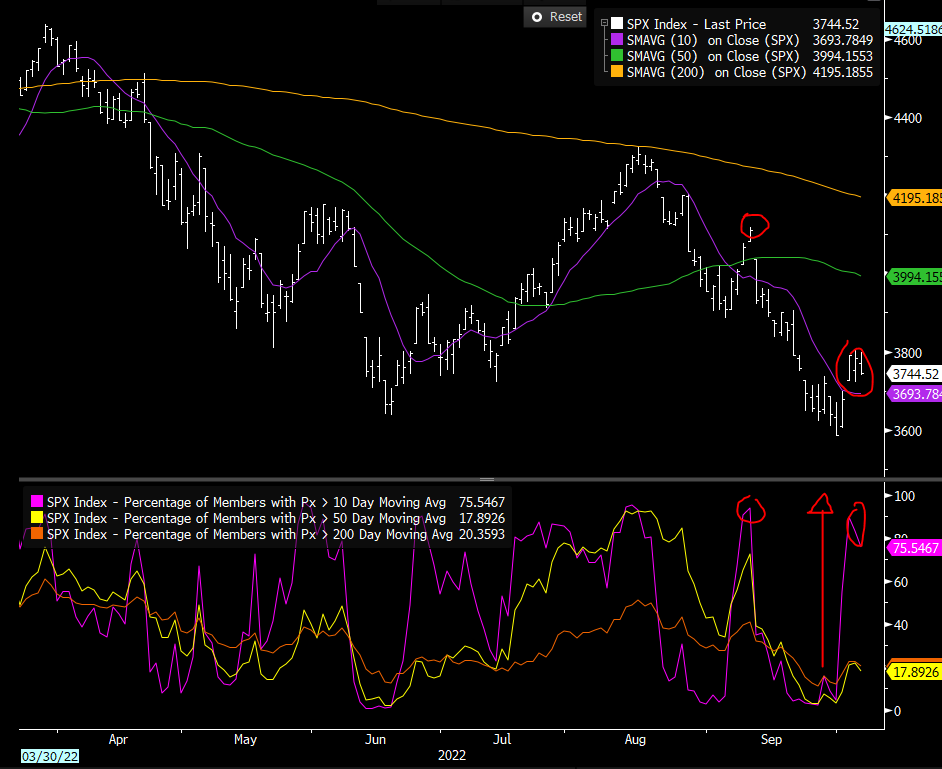

Passing at breadth, the long-term indicator is at a depressed level (% of stocks above 200d moving average, for S&P), while short term one (% of stocks above 10d moving average) reached a short term extreme level and it’s ready for an other leg down.

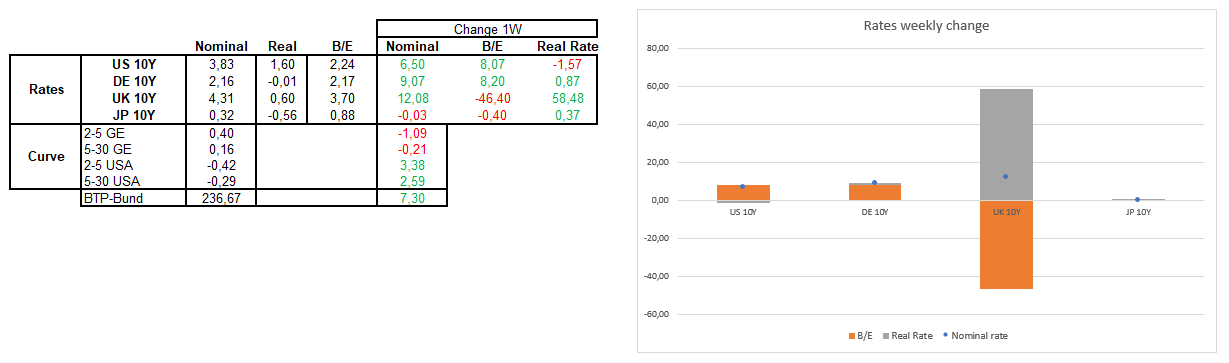

The rates market followed the same path of the “Pivot narrative” with rates down in the first part of the week, while returing to rise after OPEC+ and JOLT data. In fact in US and GER the rise is driven by breakeven, with a new flattening impulse in Eurozone, with frontloading of hike rates again on the table for ECB. The outliers is UK, with new pressure of long end rates due to BOE decision not to buying gilts this week.

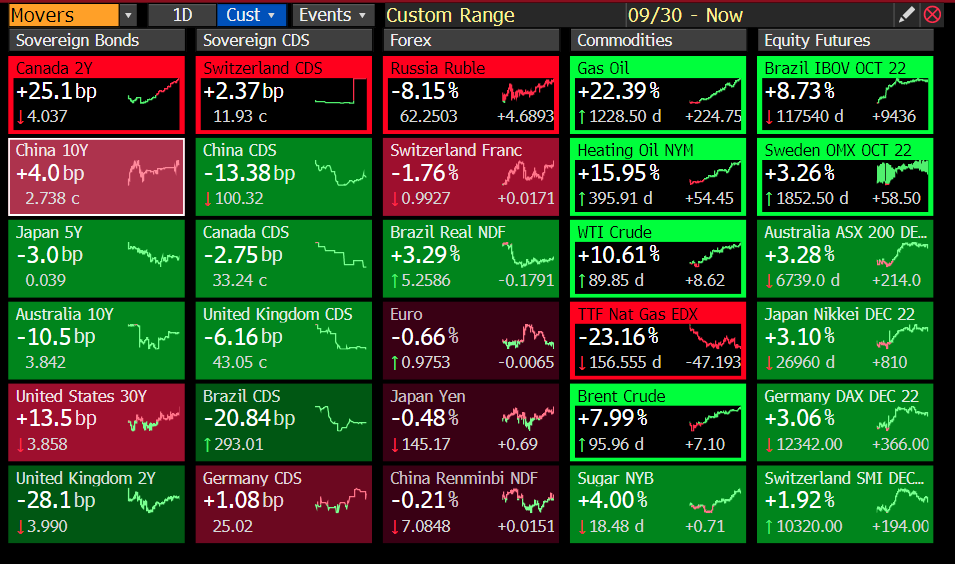

Credit market (as equity) closed the week with a positive tone with HY and IG cash tighter of 28bp and 7bp, in line with CDS, while ETF (more in line with the true trade on the market for cash) is more flat.

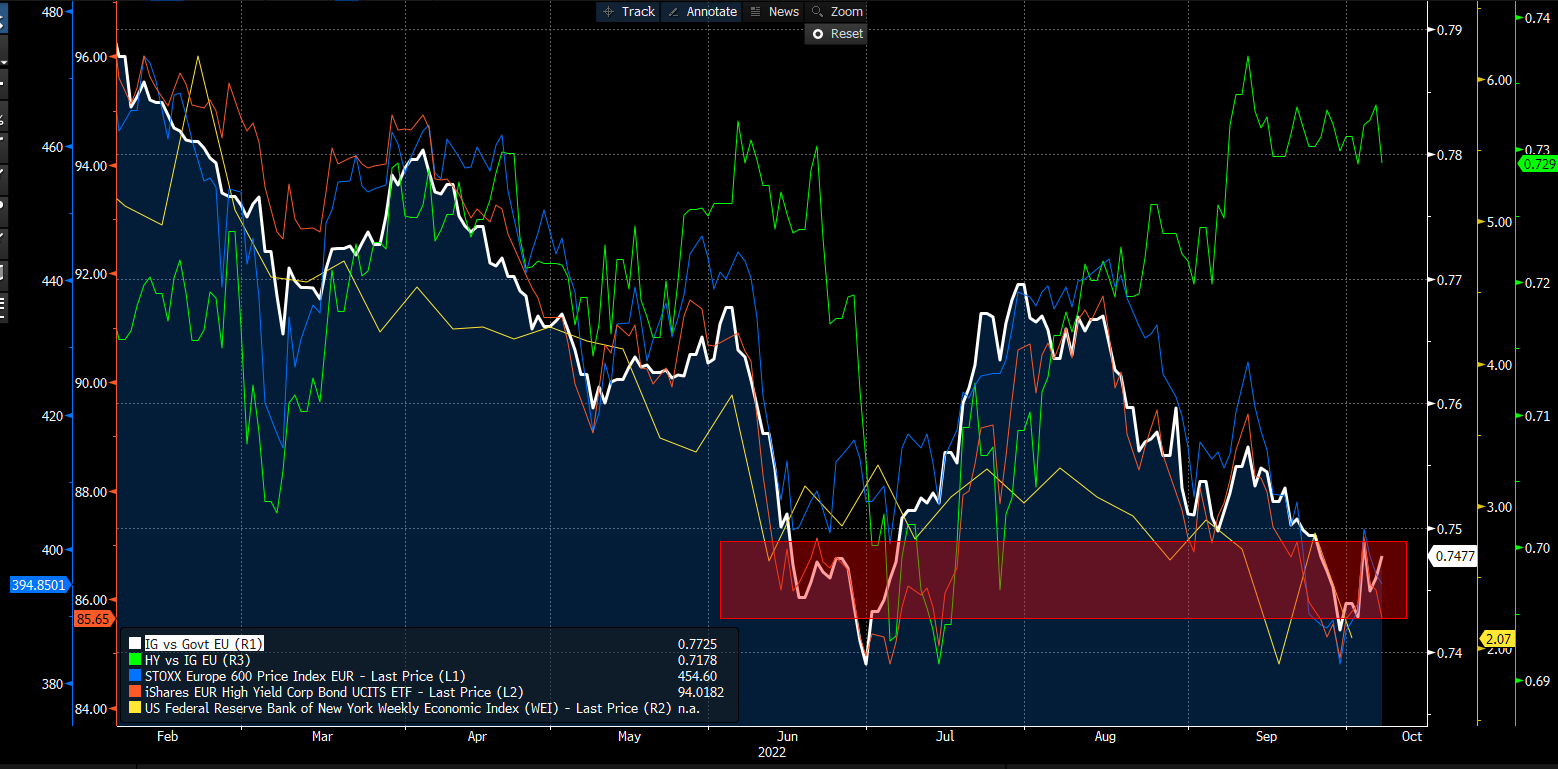

From an intermarket analysis, while HY ETF (in orange) and SXXP (in blue) are testing the low of June again, a positive note could come from the IG/Govt ratio (in whote) that stopped above the last bottom and started a mini-uptrend. If we assume that ECB stop rising rates mid-23 and rates does a top some months ago, we need a confirmation of that before having a tradable bottom in risky asset too.

While looking at HY/IG ratio something is moving on it and if macro data continue to deteriorate and narrative focus from “central bank fighting inflation” to “macro weakness” the ratio could fall rapidly, given also the expected weakness in EPS and an expected wave of downgrade.

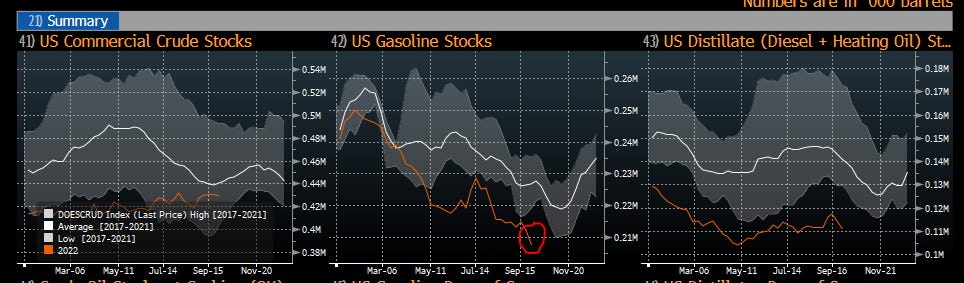

Some final words about commodities complex. While gas price in Europe continue to go down after the good filling of storage for this winter and the commitment for a price cap for gas, after OPEC+ cut Brent, Crude and products (gasoline and diesel) spiked again. I speaked above of this. The pressure on products is visible on:

the low level of inventories;

the crackspread margin returning to grow again;

timespread of Brent vs price (see the two charts below that one on timespread is from @MenthorQpro).

MICRO:

Regarding single name news that impacted market pricing for winners:

TEVA: reaches agreement with Arkansas to settle some claims

CASTELLUM: M2 asset management to sell 40M Castellum shares

Regardin loosers:

CCL (Carnival) reported EBITDA below consensus for guidance for lower negative EBITDA in Q4. Cumulative bookings and prices for Q4 are below historical ranges.

CONSOLIS (CMPCTB) after the downgrade (to B3 from Moody’s) last week continue to underperform

ADRBID: no particular news, only HS shorting via CDS (50MM CDS traded only from a bank yesterday) and news the founder Dragan Solak buying the local Sofia football club

It’s all for today, Have a nice weekend.

If you enjoyed my job/analysis feel free to forward it to friends/colleague and remember to subscribe to the newsletter.

Bye Bye!

Great!

Thanks for your weekly posts. What do you use for the IG/govt ratio?