Weekly Credit Market Review - Oct 14

Weekly Credit Market Review - Oct 14

A thread from macro to micro

Welcome back at the weekly recap, as usual at the end of the week. As always if you like my job/analysis please subscribe below and share it and I remember you that I am also on twitter at @Credit_Junk. And now let’s see what happened this week.

MACRO/NARRATIVE:

Let’s dive directly with the list of the main news driving my attention and market this week. We had a new strong inflation print in USA (and a list of new hawkish central banks following it) and a totally caos around BOE and UK.

The week started with BOE announcing new support plan with increasing size of gilt purchases operations until 14th October amd the launch of a special repo facility to help UK pension funds. The caos arrived Tuesday and Wednesday with BOE adding gilt-linkers to purchases operations and claiming funds had only 3 days to do the necessary rebalancing operations (so closing the door to an extension of the plan). During these 2 days several FT pieces announced an extension, eventually denied. A “pivot” (I hope you excuse me for the use of this word) arrived at government level where Liz Truss is going to announce a truly U-turn on their fiscal mini-budget, removing the tax-cut program. This is a victory for bond vigilantes. Liz Truss will announce the new details this afternoon, but a thing is one thing is certain, she removed Kwarteng as Chancellor to safe herself;

The week opened also with a news regarding Germany that backed the idea to issue joint debt for energy measure at EU level. Also this news was denied later;

And finally we had the CPI print in the USA. Market and experts arrived at the data with a softening of inflation that was disregarded.

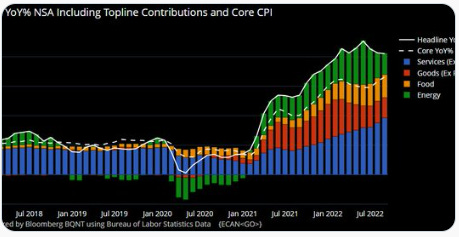

CPI headline yoy was +8.2% (expected at 8.1%), while core increased from 6.3% to 6.6% (above expectation too). Below the monthly change.

*US SEPT. CONSUMER PRICES INCREASE 0.4% M/M; EST. 0.2%

*US SEPT. CORE CONSUMER PRICES RISE 0.6% M/M; EST. 0.4%

Services continue to climb higher (contributing 3.9 percentage points) with the big impact of rent and housing related indicators but also core services like healthcare and transportations.

The worst part of the story is that the inside the goods the “sticky” part is now incrasing at the highest level in 40 years. This part is more related to wages and the job market.

MARKETS:

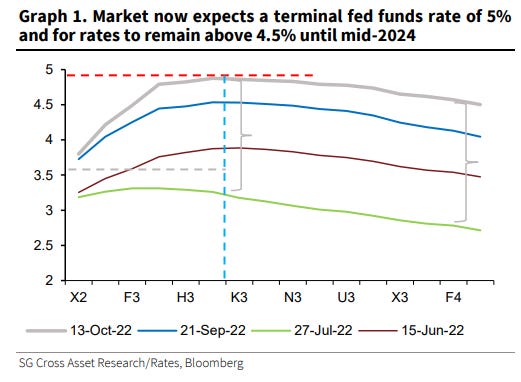

Given the fact that the inflation data was the most important data of the week is not a surprise that a strong data pushed the terminal rate for the FED rate near 5% with almost 125/150bp of hikes for the end of the year.

Below I report the “GMM” (Global macro movers") of bloomberg to have an idea of what happened during this week. Now let’s look to analyze each one in the details.

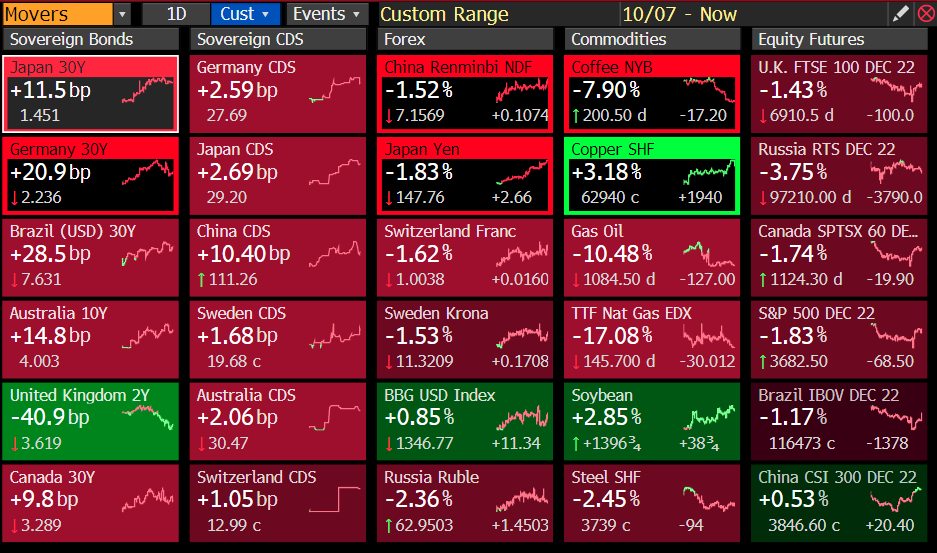

RATES: the above consensus CPI pushed yield higher with 10y treasury reaching 4% intraday and Germany bund near 2.40%. Both returned a bit lower from the peak but close the week higher. Being near a peak in hawkishness on terminal rate and with a big shift from monetary stimulus to fiscal stimulus, the curves had a steepening impulse. The only outlier is clearly UK, where gilts had a very volatile period and the U-turn (pivot) regarding the fiscal budget helped reducing the pressure on lont term rates.

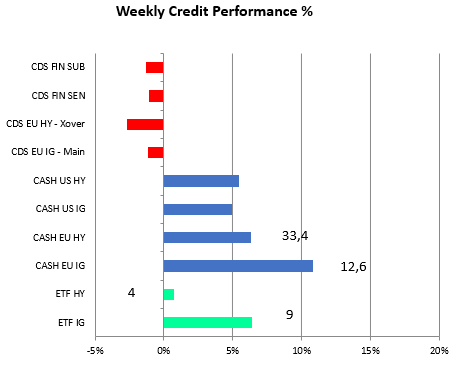

CREDITS: the credit week was quite with some widening in cash index level, not reflected completely on the ETF implicit spread. At the opposite the movement on syntetic products (all CDS instruments) was that on tightening. CDS is almost used to take fast position or to hedge core portfolio. Going into the CPI data of the week most player covered some position, and rushed to close that after the data.

Using BNP positioning indicator we can see that positioning in credit is short overall, so despite with the high inflation not changing nothing from a macro point of view (FED need always to hike and mantain rate elevated for a while), it’s logical that some protections were removed pushing some tightening there.

As usualy I look at intermarket analysis (usefull for risky asset from IG, to HY and Equity). We have a curious divergence in fixed income world. IG/Govt continue to be hit down, while HY/IG is performing very well (totally not caring macro momentum). My HP? IG and HY were driven for now only by rates and not by credit risk. Something need to happen. HY/IG is not paying enough for the risk we see in other markets. Given the link between PMI and EPS/rating I wait a EPS revision and a wave of downgrade too).

FX/CURRENCIES:

Given the uncertaintly DXY (dollar index) closed the week in green with a positive return but we in G10 also GBP rebounded with funds closing some abroad positions to cover margin call and thanks to the fiscal U-turn. JPY continued to break record after record, now well above 147. We are in the no-man land. BOJ Kuroda and finance minister Suzuki reiterated they will respond agains excessive moves.

EQUITY:

Price action in equity is counterintuitive at the first look. SPX and SXXP are closing -1.9% and +0.6% respectively. Below it’s the chart for Europe (Stoxx 50) but it’s similar for SPX too. Market arrived at the CPI event very weak and rebounded strongly after that. What are the drivers? I think the most important is technicals. SPX arrived intraday at 3500 (almost the 50% rebound from covid level) and a big rounded number. At the margin the news is not moving nothing, we know FED will rise at the point of breaking something.

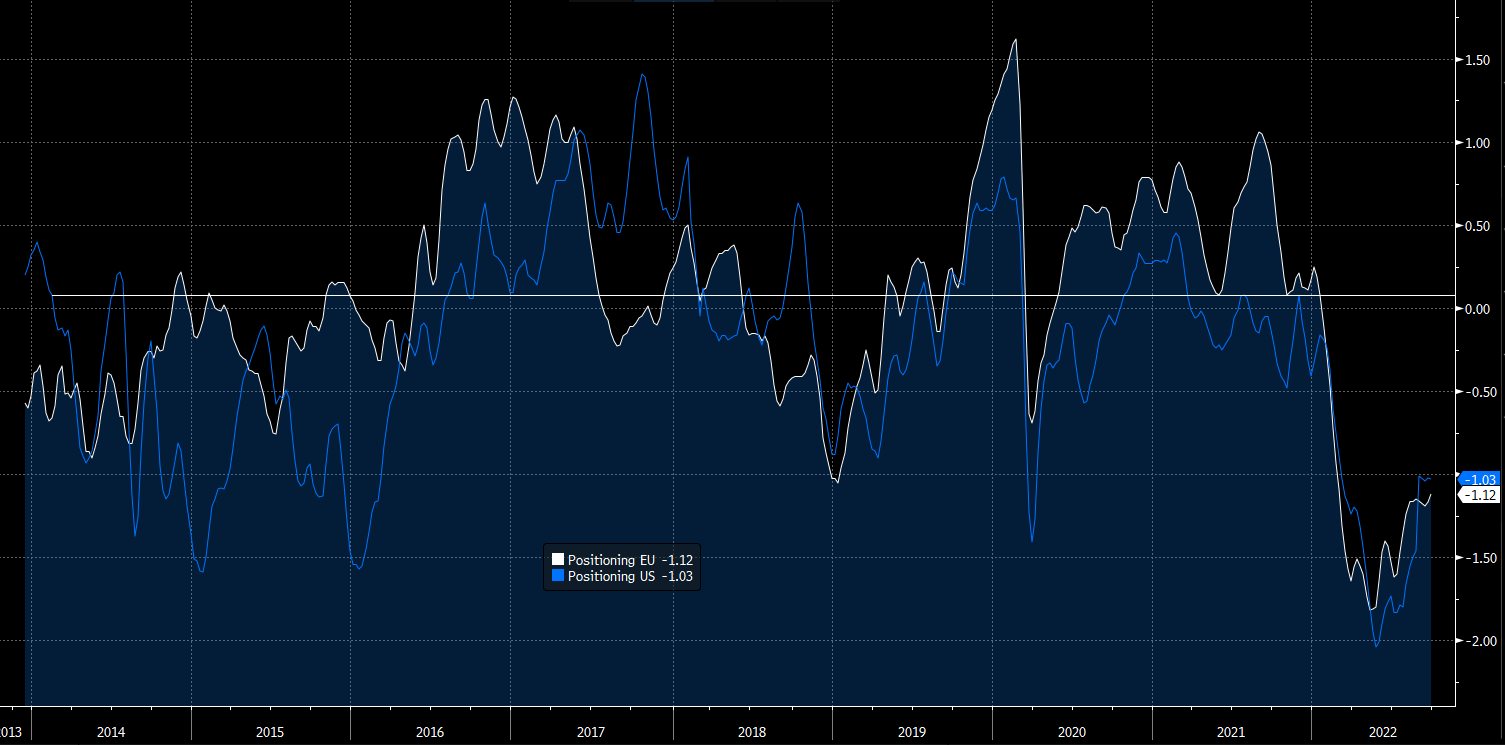

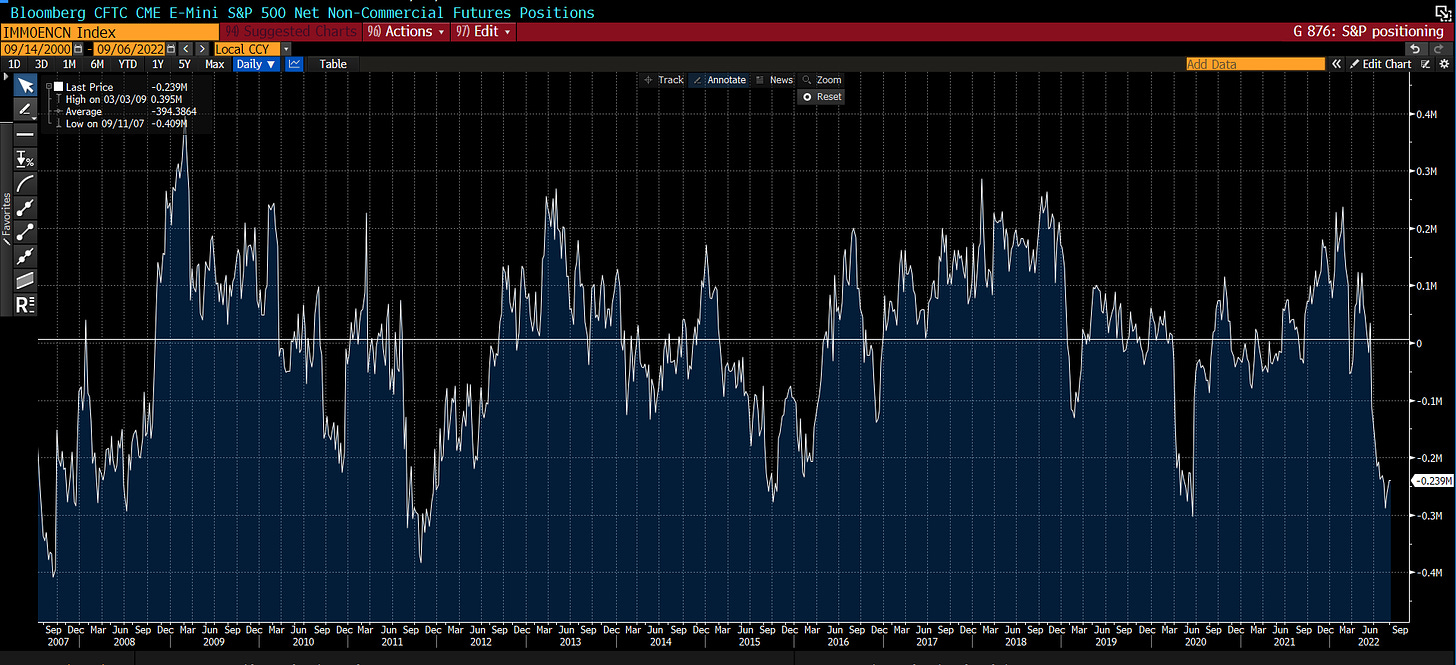

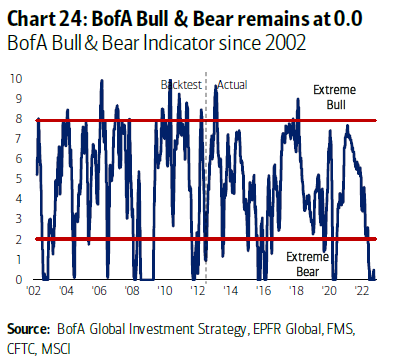

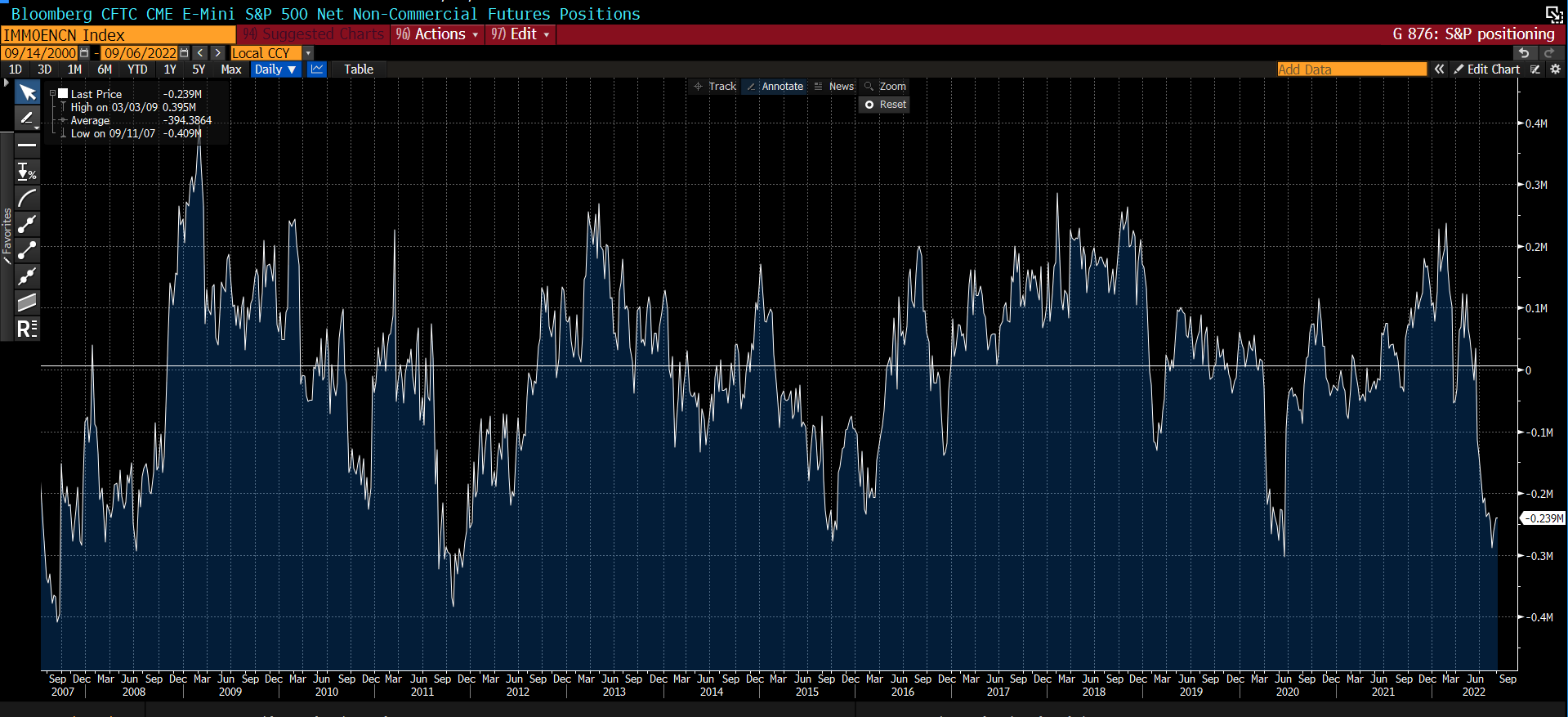

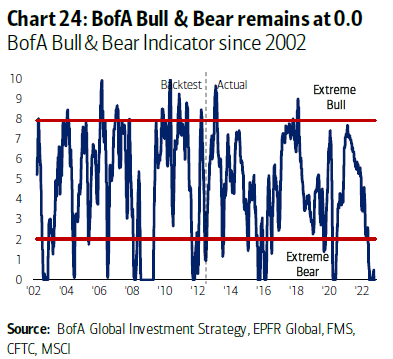

Positioning (below the CFTC data for E-mini S&P 500 as a proxy) and sentiment indicators (below the Bofa Bull & Bear) are very low so a short term rebound remain in the card.

I don’t want to be misunderstood, my fundamental view remain bearish (given the direction of liquidity and of various leading indicators like order, housing sectors, transportations, etc) but bear markets (and also bull markets) are not like a straight line.

COMMODITIES:

I will end with some words regarding commodities, one of the best spot to start to gauge the health state of the economy. Despite a tight products market in gasoline and diesel, energy futures markets declined this week with fear on growth and central banks tightening (WTI declined 6%, Brent 5%, Gasoline 4). The same fears impacted industrial metals (despite a strong copper that is up 2.5%). A most part of industrial metals has a very low level of inventories so is subject to spike risk in case of some reopening news coming from China. Precious metals (gold and silver) suffered from high dollar and high real rates, while only grains is up driven by uncertainty in Ukraine and the shipping corridor and weather impact on harvests.

MICRO:

Winners of the week are:

United Group (ADRBID) that hired Goldman Sachs to sell asset to reduce debt and leverage.

Playtech (PTECLN) were Moody’s affirmed Ba3 rating after the announcement of the company to use cash on balance sheet to pre-pay of the senior notes

Losers:

FOSUNI: continued risk related to China and real estate

CASINO: downgrade by S&P to CCC+ from B-. Inflationary is crushing profitability

Webuild (IPGIM): high volatility with bonds loosing over 10% after a BBG news affirming that cost on pre-covid contracts in Australia were materially higher than expected. Company in a presentation to analyst denied the news affirming that there is a easy passthrought of cost. The company has a low leverage and a big backlog of order. Just this week they winned a contract for construction of a breakwater at Genova port.

It’s all for today. I hope you enjoyed my job/analysis. Feel free to forward it to friends/colleague and remember to subscribe to the newsletter.

Have a great weekend, Bye Bye!

Thanks for the content, very insightful indeed. I have quick question: how is the HY vs IG index calculated in chart #8?

Thank you

Alessandro

thanks bud, appreciate, great take as always to wrap up the week ... have a good weekend!