Weekly Credit Market Review - Oct 21

Weekly Credit Market Review - Oct 21

A thread from macro to micro

Welcome back at the weekly recap, as usual at the end of the week. As always if you like my job/analysis please subscribe below and share it and I remember you that I am also on twitter at @Credit_Junk. And now let’s see what happened this week.

MACRO/NARRATIVE: In my handwritten notes for this week it was a quite week from a macro release point of view but an other true volatile politically one. We had:

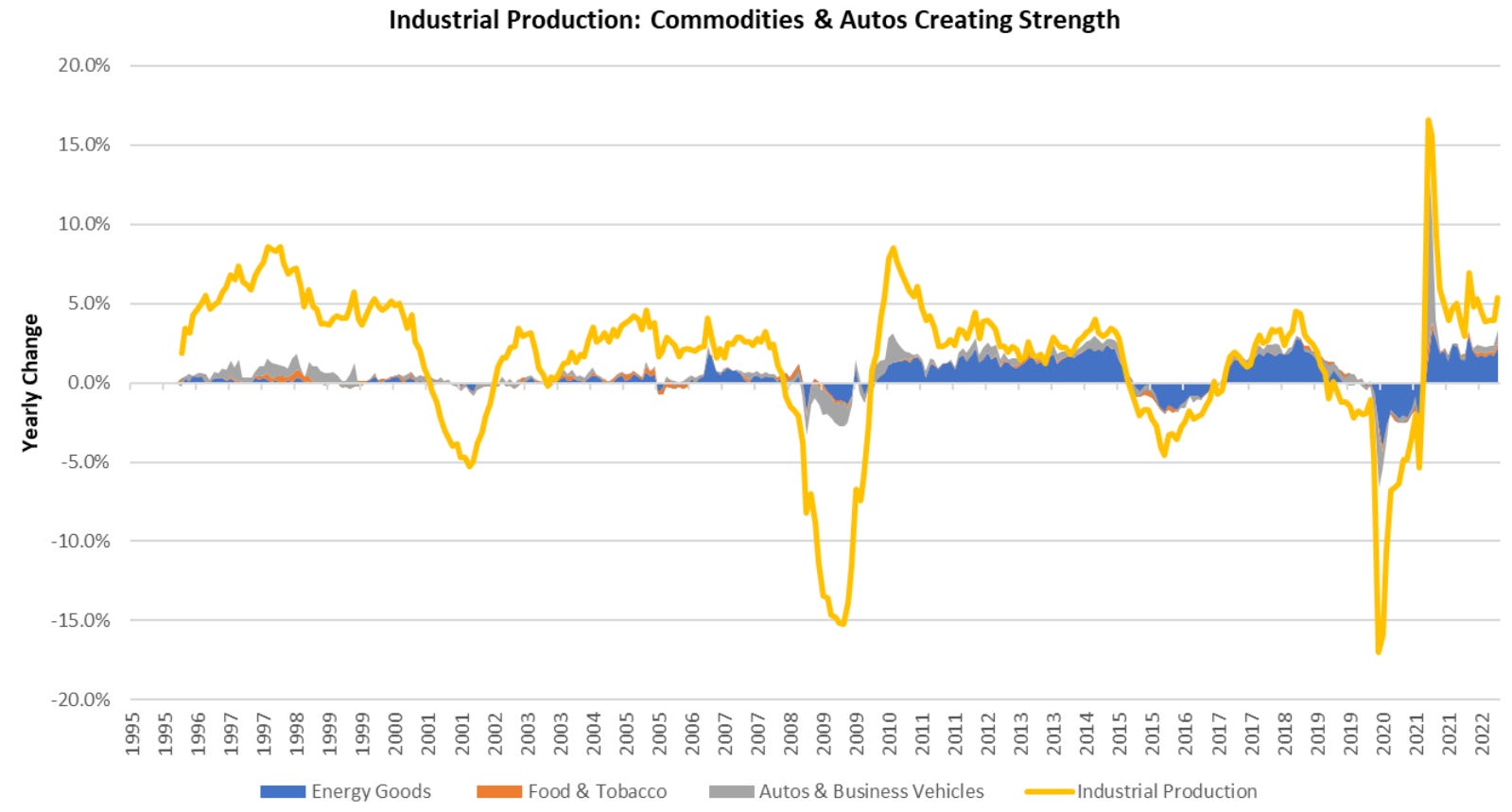

In USA the macro data showed a strong IP (industrial production data) with an increase of 0.4% in September (vs expectation of only 0.1%). As showed very well from @prometheusmacro this was driven almost by energy sector (supply constrained) and by autos (demand restricted, with an incrase in inventories).

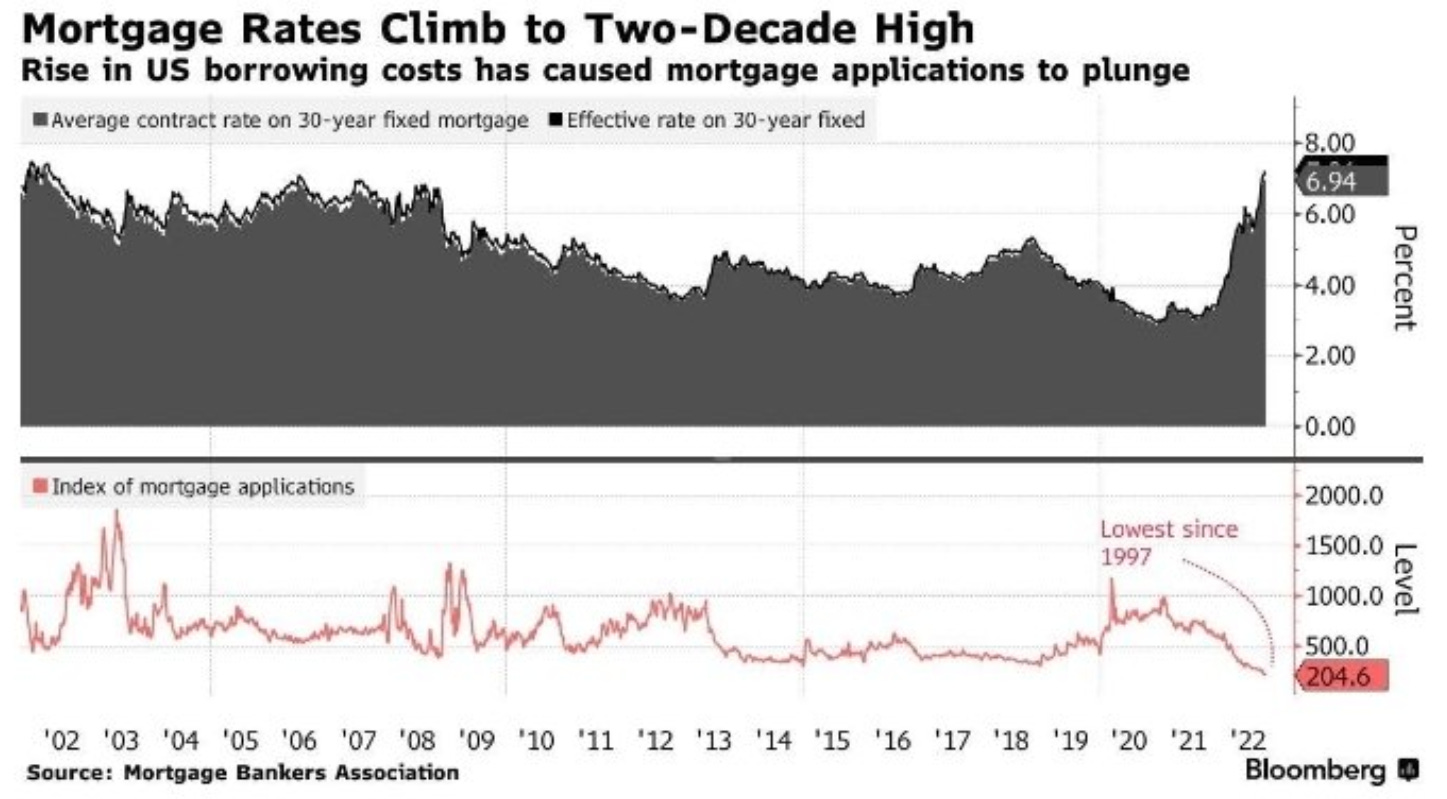

We had also some weak data from housing sector, impacted a lot from the rising rates environment (high rates for mortagages means lower transactions). A very bad indicator is, in fact, the low level of mortgage applications below.

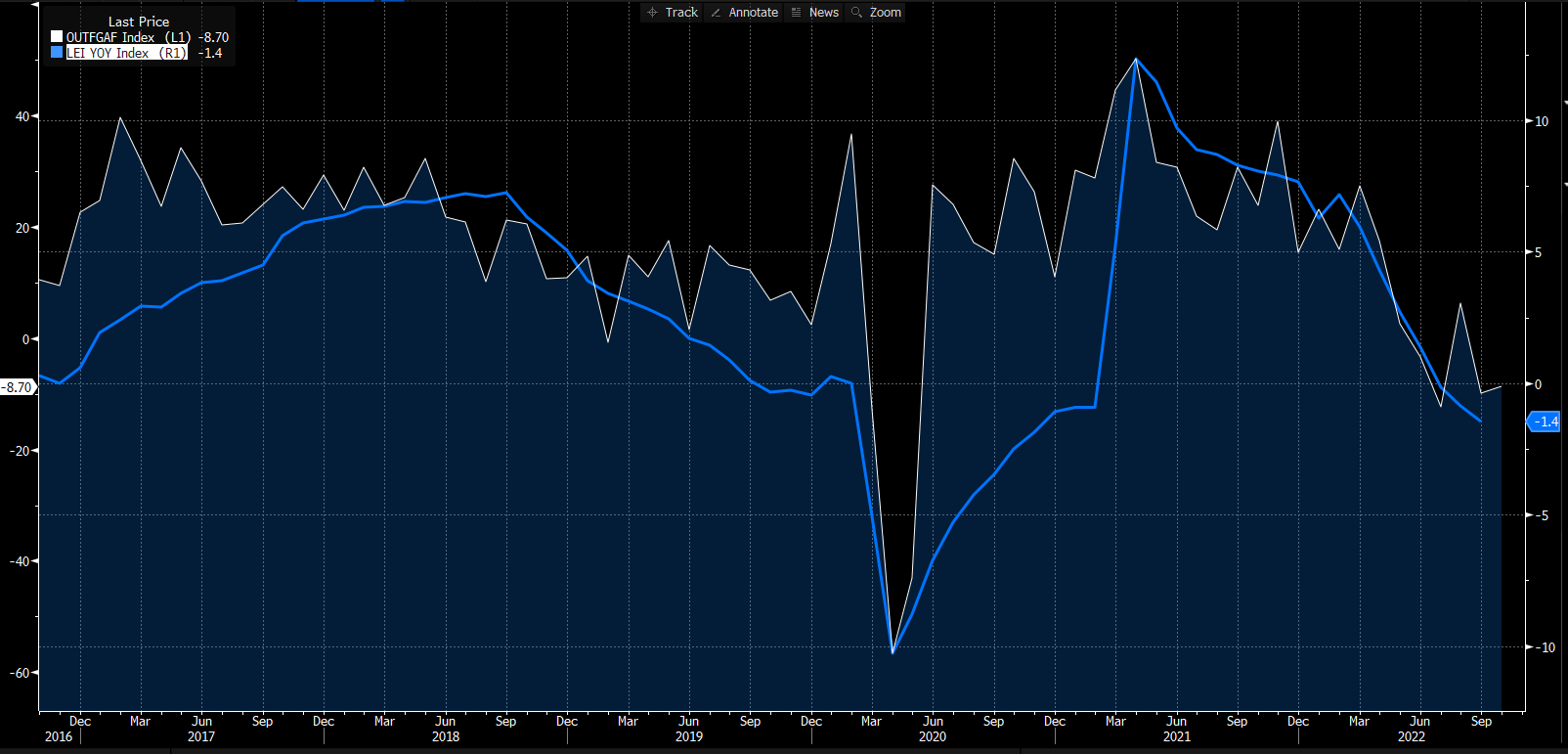

And at the end also some leading indicators that confirmed the deteriorating/weak macro outlook, with LEI for September and the Philadelphia Fed Business Outlook for October.

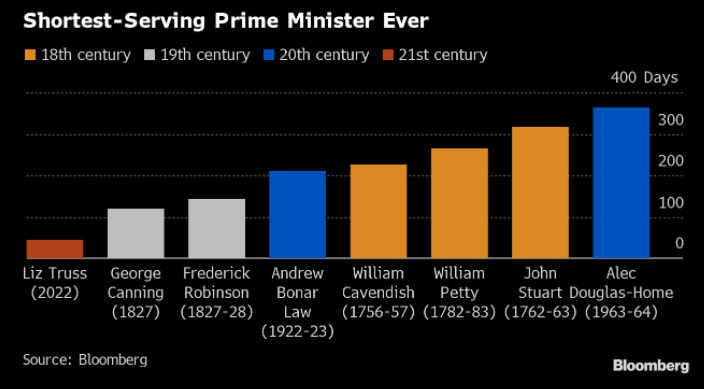

On the political side Liz Truss resigned after failing on budget approval and on high volatily on the market. She is the shortest-serving prime minister ever in the story of the country and she was not able to calm the market about her plan to increase deficit (with new debt) to cover the high energy cost the county is suffering.

While continue the battle between central banks with some FED speaker (as Harker of Philadelphia FEF) affirming that rates need to be higher and mantained higher for a while due to the persistent inflation. BOJ continue to diverge with other emergency bond buy operations, while BOE in a presentation of BOE at Imperial College affirmed that they don't see the need to hike as mkt price and that they will respond relatively promptly to news about fiscal policy.

MARKETS:

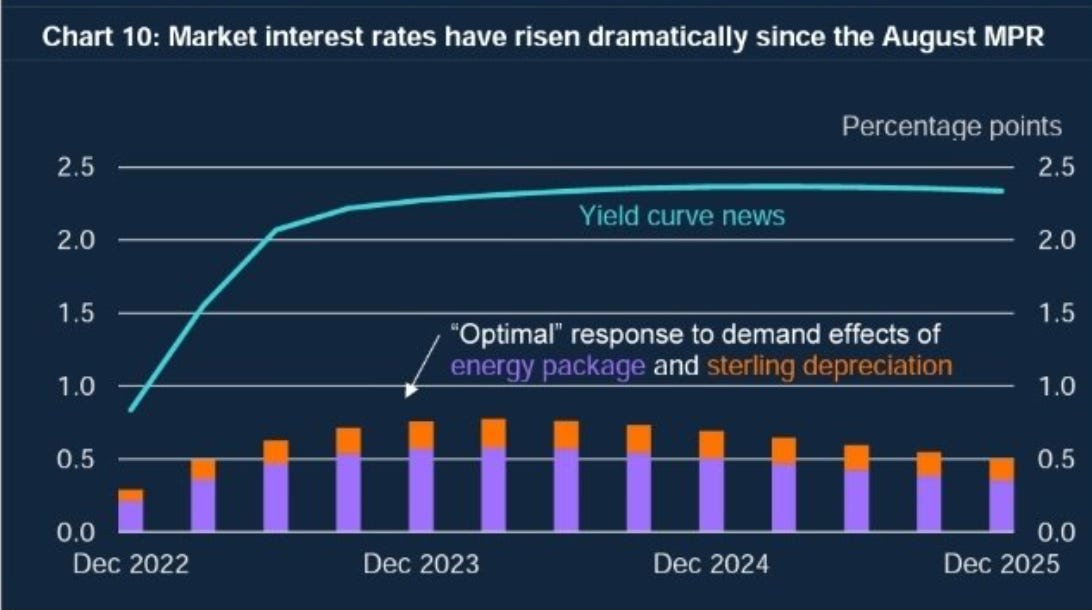

Starting with fixed income, interest rates continued their drift higher in US and Germany, with higher terminal rates (in the USA arrived at 5% for mid 2023). The only outlier was UK with the resignation of Truss and the hopes of a less funded budget. Passing now on credit IG underperfomed during the week with widening of 11 and 19bp for index and ETF-implied. HY move was quite, as that one of CDS, following more the rebound in risky asset. It continue to be a duration fear move for now.

Classical ratio of BB/BBB, usually widening in risk-off period, trade now near the tightest part of thei range (almost -2 standard deviations).

From an intermarket point of view the ratio of HY/IG (calculated using two ETF) is totally diverging from other asset class and liquidity indicators (as credit IG/Govt ratio). Equity rebounded this week due to the very bearish positioning and sentiment (so a technical rebound for me) while HY ETF and IG/Govt ratio. Remember this: give always credit to credit. Credit is life, credit is liquidity, credit is growth!

Some final words on FX and JPY. As said BOJ remains the outlier between the DM central banks and the pair with dollar broke the 150 level. There are not so much thing that BOJ could do to stop this, only to sell dollar and treasury (this impact viciously the treasury rate) to buy yen, but it’s only temporary without a global agreement. Basically with a so high level of debt internally and pension funds heavily invested in bonds BOJ want to avoid a UK scenario and need to mantain a low level of rates, impacting JPY. This has a cost in term of imports (needing to import energy products) but have also some advantage. News from yesterday: Taiwan semi to expand Chip production in Japan.

MICRO:

The winners of the weeks are:

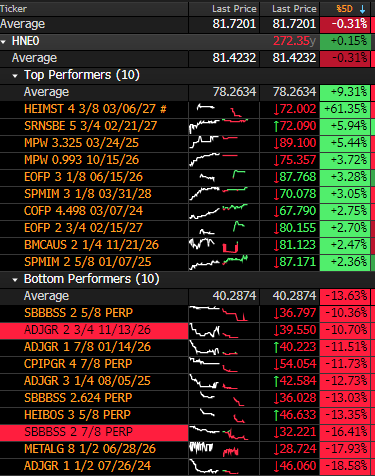

FAURECIA (EOFP) with a good reporting. Strong Q3 with a 31% rise in revenue and an increase in full year guidance.

Saipem (SPMIM) with the announce of a 4.5bln $ contract win

In the losers I see a lot of real estate name that remained volatile all the year like ADLER, SBB, CPI Property.

It’s all for today. I hope you enjoyed my job/analysis. Feel free to forward it to friends/colleague and remember to subscribe to the newsletter.

Have a great weekend, Bye Bye!

thank you, great take, cheers!