Weekly Credit Market Review - Sept 09

Weekly Credit Market Review - Sept 09

A thread from macro to micro

Welcome back at the weekly recap, as usual at the end of the week. As always if you like my job/analysis please subscribe below and share it and I remember you that I am also on twitter at @Credit_Junk. And now let’s see what happened this week.

MACRO/NARRATIVE:

The week started with the news that Russia closed indefinetely the gas flow throught Nordsteam 1. The tip-for-tat intensified after the commitment of Europe to increase efforts to reduce price pressure on gas and energy prices. An energy ministers meeting is planned for today in Europe with different target as reducing consumptions or put a price cap on imported gas. Also nationals government are trying to reduce the pressure on industry or consumers (Germany pledges a 65bln fuel cost aid), no matter if this means more deficits. At the same time Putin threatened to reduce the flow of food to western countries starting to use also food as a weapon. It’s a news of this morning that started to ban rapeseed exports.

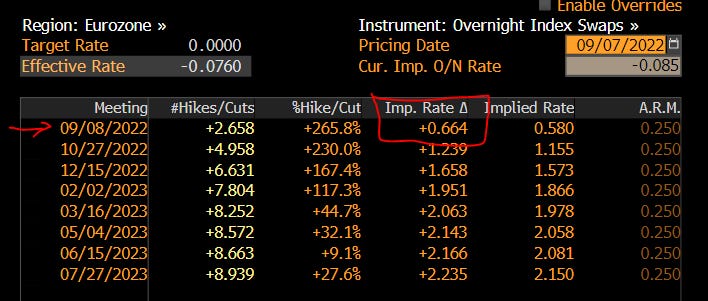

But the market mover news was the decision of ECB. Before talking of it we hade also RBA decision. The central bank of Australia increased rates of 50bp as expected but affirmed also that going forward the monetary tighening could slow (a dovish hike for them). “Au contrair” for ECB that decided to hike 75bp all the rates as expected by market going into the meeting. ECB appeared committed to fight inflation and bring it back to 2%, despite seeing some growth weakness ahead. Lagarde said that they don’t know where is neutral rate, but they prefer to frontload rates hike to be sure they win their battle. Just one hour after the meeting ECB members not-excluded a 75bp hike also for octobers.

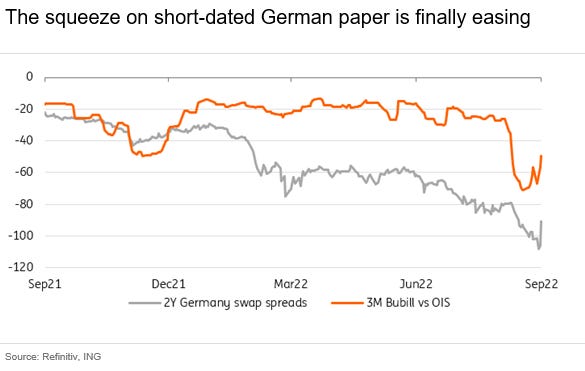

While on collateral issues (a problem not followed by more investors, traders or fintwitter) they decided to remove the tearing from current account, and given that now deposit facility will be remunerated 75bp this could remove some richness from short term bills (trading at the moment deeply negative vs OIS/swap curve).

MARKETS:

The comment of the market will start, given the circumstances, from rates.

RATES: FED, ECB and also BOE have an inflation problem (with ECB and BOE more risk related to energy than FED) and all central banks are committed to reduce inflation bringing up real rates above neutral rate. And it’s what happened here with rates up 15/20 up along the curve and a big move in flattening in Eurozone (given the ECB meeting this week).

CREDITS: Despite the total return on average is not always good due to the rates move, spread performance was impressive, with a tightening of 25bp in HY cash and 37bp in implicit ETF. IG move was less strong (-2bp) given the high sensitivity to duration. CDS performed better than cash in this environment.

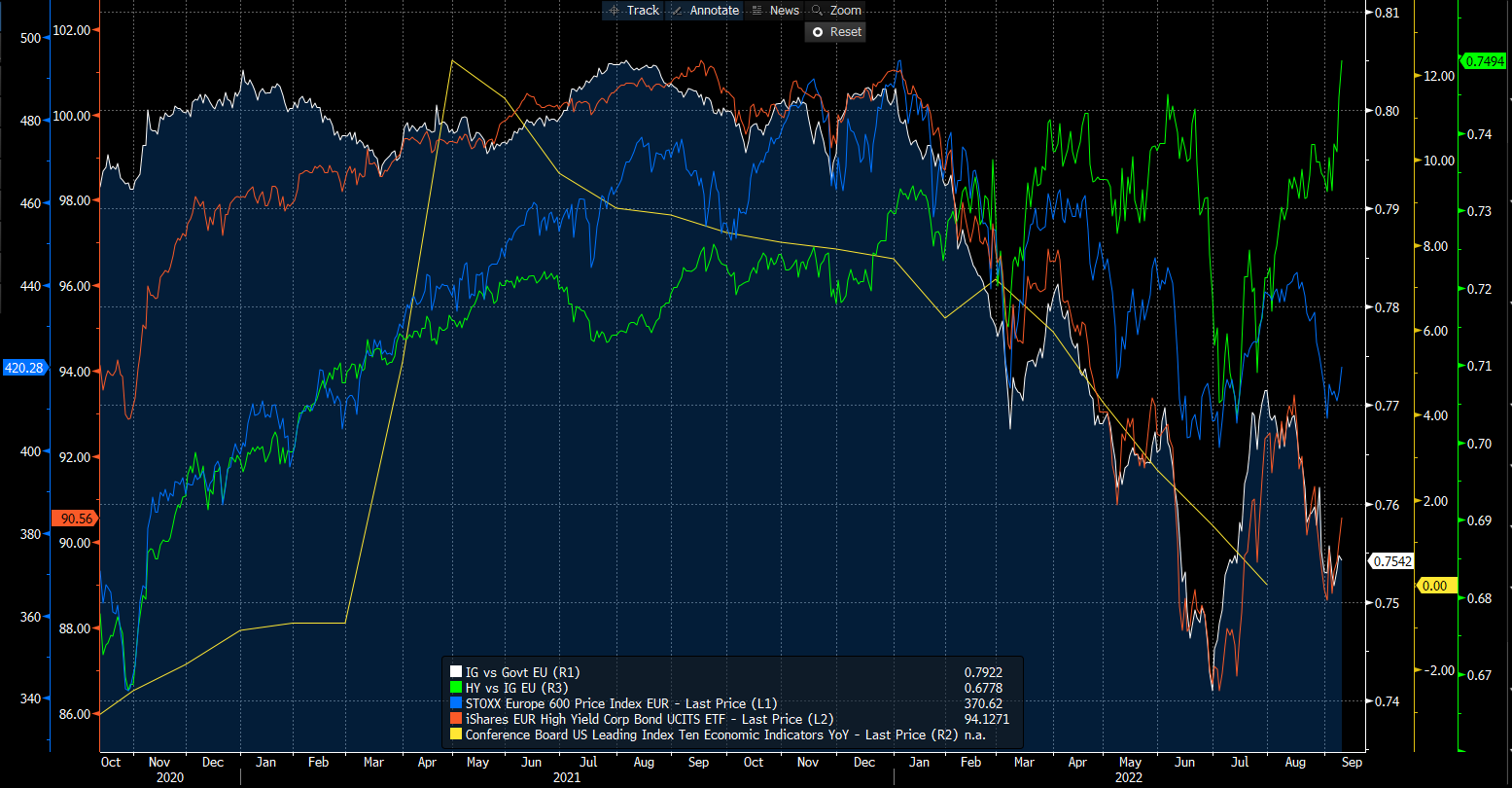

The rush to buy pushed the price of ETF at a premium to NAV (below the chart for EU HY ETF but it’s similar for IG too).

Looking finally at intermarket analysis it seems that IG to Govt ratio finded a bottom for now. Credit is a very important indicator to look, also if you trade equity. In fact is liquidity that moves markets. Liquidity is the demand of consumers to purchases goods and assets. This demand is driven by the tightening and easing of credit. HY ETF and equity (Stoxx Europe) bounced this week, with investors assessing if monetary tightening is almost entirely priced or not, but what it’s totally distorted for me is the HY to IG ratio, with HY not pricing at all any weakness in growth.

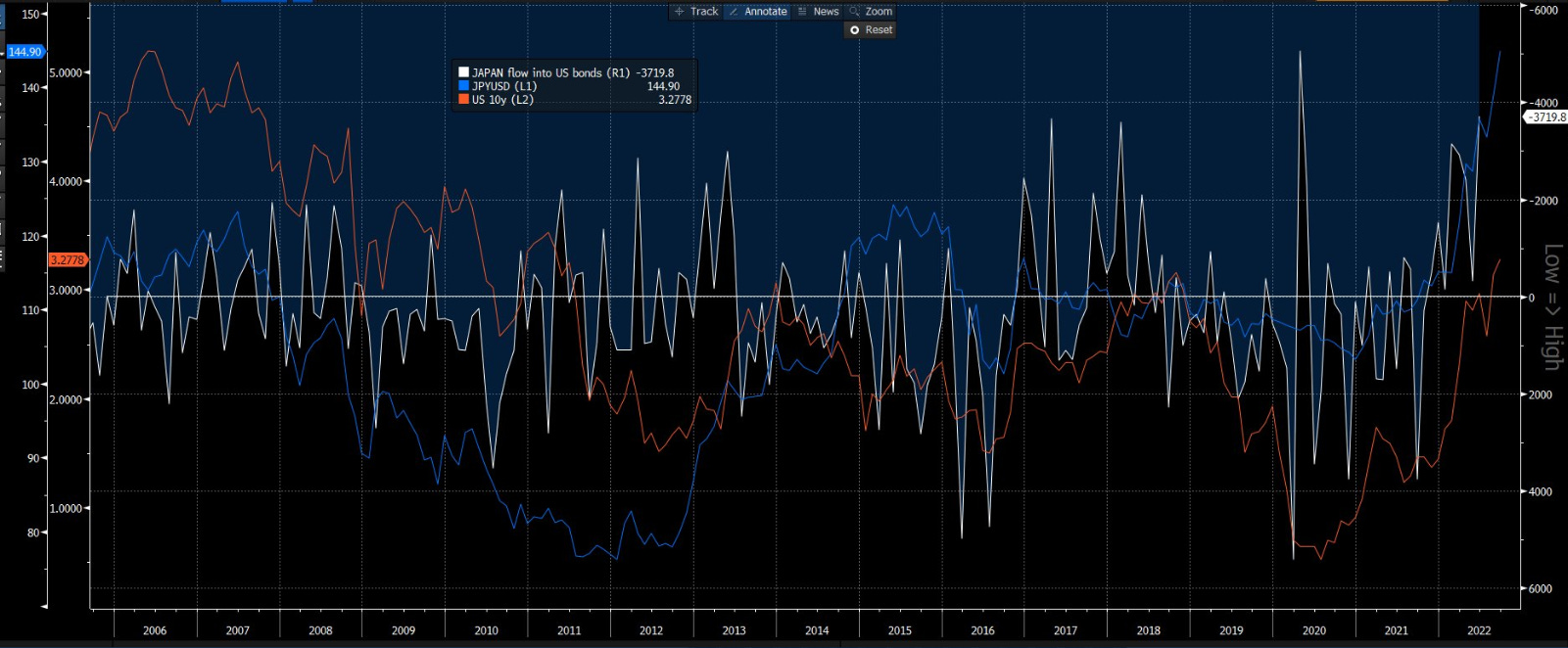

FX: Yen (JPY) continued to underperform in FX market due to the different path of BoJ vs other central banks. Boj is committed to mantaining dovish stance and JPY arrived at 145 vs dollar. After some worried word yesterday evening by central bank, the currency rebounded a bit but as showed in the chart below with Japan and China being the biggest holders of treasury, any weakening of the currency is weighting on treasury yield to (with investors selling investments abroad). This Yen weakness is also putting some pressure on others Asia currencies too (as Won and Yuan).

COMMODITIES: Commodities market was a mixed bag this week, with:

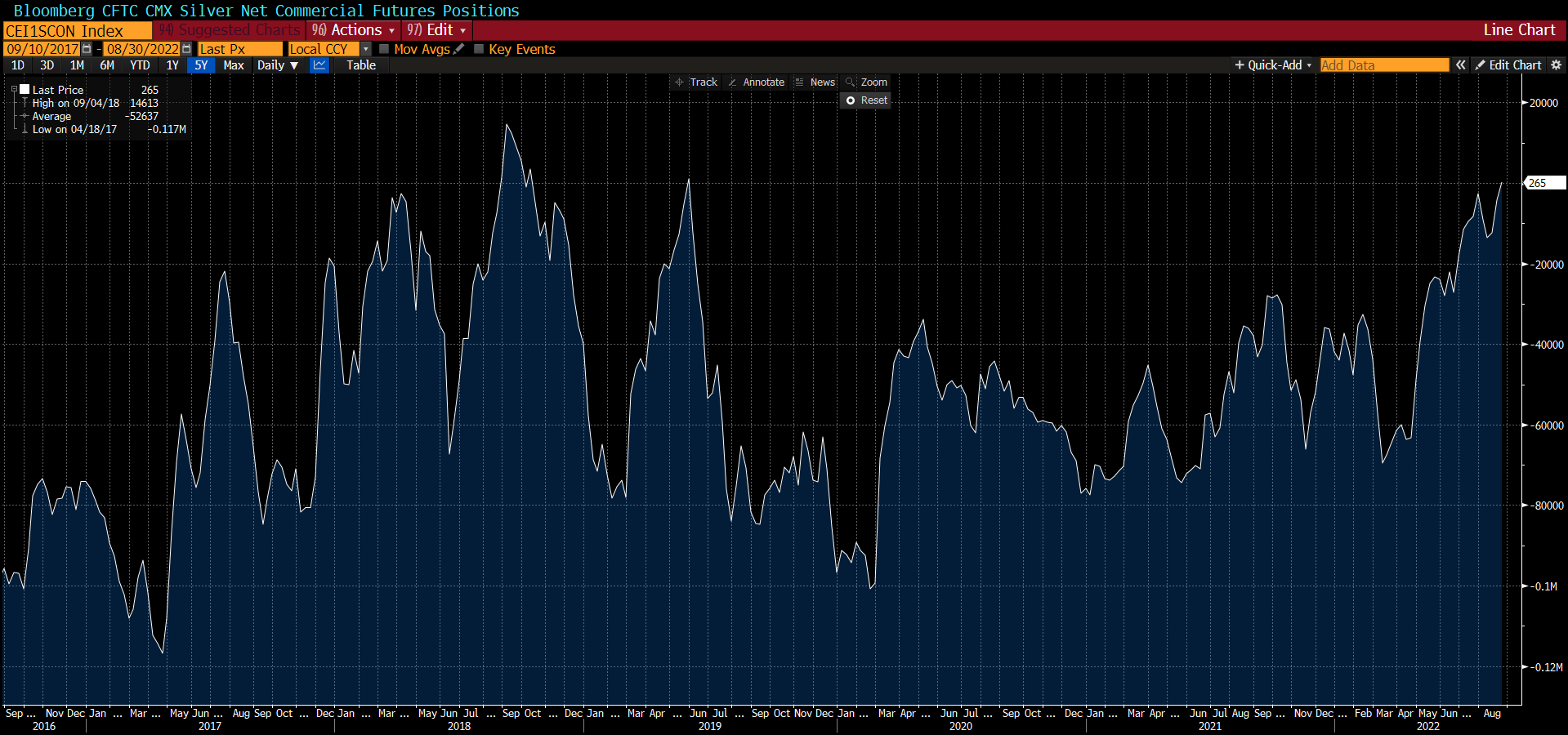

precious metals up (Gold +1.2%, Silver 5% given the extreme short position of speculators - below the long position of commercials that is the reverse of speculators)

industrial metals up (Copper +5%, Steel +6%, given the very low level of inventories and despite the continued pressure of the covid lock-down in China) up this week.

energy sectors weak, with oil impacted by growth fears and continued SPR release while gas in Europe down thanks to hope of a positive action by european governments

MICRO:

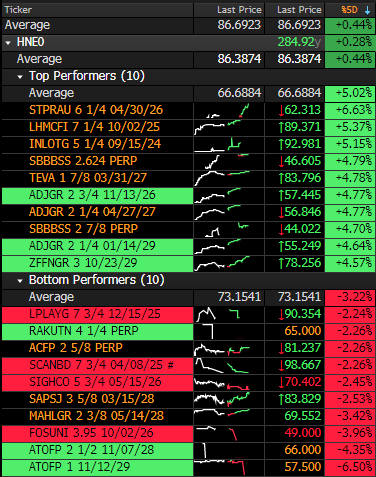

Winners of the weak are usually more beta names (like CCC or very low price bonds) while to comment I look at:

TEVA: Studies Show Effectiveness of AJOVY®▼ (fremanezumab) for Treatment of Migraine in Patients With Co-morbid Depression

SBB: signed a letter of intent to divest a property portfolio at an agreed property

Losers

ATOS: Equity drops a lot after GS cuts to Sell

FOSUNI: continued weakness of real estate market in China

MAHLE: 5th of September reported disappointing H1 2022 results, in terms of margins and cash generation. Moody's 'Ba1' rating (negative outlook) at risk.

I came across your blog and I must say I am really impressed. I must confess that I am also a newcomer to the credit market. I have a few questions regarding the weekly credit performance and the yen.

1) What does it mean if the spread of IG or HY is tightening? To which counterpart does the spread relates to? Whats the difference between Cash HY and the ETF HY? Am I correct that CDS on the HY/IG is the cost of insurance of these assets in case of default?

2) Regarding the question in the Yen-section I´m a little bit confused about the the part of treasury holders and the implications on the treasury yield a weakening of the currency has. China and Japan are the biggest holders of US Treasuries in US dollars. So do you mean that if their currency is weakening against the USD, than they are incentivized to sell their treasuries because the lose value?

I would appreciate it a lot if you could help me understand these questions.

Cheers

Nice summary of credit markets. Very insightful ..credit is key to watch in this cycle and I don't keep track of it as much as I used to. Thanks for sharing.