Weekly Credit Market Review - Sept 30

A thread from macro to micro

Welcome back at the weekly recap, as usual at the end of the week. As always if you like my job/analysis please subscribe below and share it and I remember you that I am also on twitter at @Credit_Junk. And now let’s see what happened this week.

MACRO/NARRATIVE:

There was a lot of events this week and most of them (after last week focused on central banks) are related to geopolitcal events. Let see them:

there was a referendum in the Ukrainian zones occupied by Russia for annexation to Russia. These zones (Donetsk, Lugansk, a Zaporizhzhia e a Kherson) had a majoirity of russian speaking population and, despite the referendum was questionable in methods, a percentage higher than 95% voted to be annexed to Russia. Kremlin said that strikes against these new territories, incorporated in Russia will be considered act of aggression against Russia and so they are ready to use any weapons to defend it (including atomic bomb);

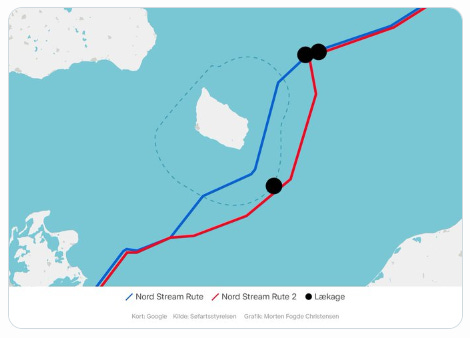

there was also a series of explosion on Nordstream 1 and 2 gas pipelines. These happened near the Danish Island of Bornhom, close to Russian territory and almost near the Baltic Pipe running gas from Norway to Poland and also the timing is suspect (the same day there was the inauguration). First newsflow claim that is a act of sabotage (3-4 explosions in one day?). The exchange of accusation between Russia and west countries is high (why to sabotage a 0-flowing pipe from a Russia point of view if not to put pressure on others pipeline risks, why not to execute the talked plan of US as talked in TV some months ago?). It doesn’t matter, for me the risks are that one of an other escalation, so pay attention to it;

in the weekend we had elections in Italy. Partecipation rate was low and a far right government (leaded by Giorgia Meloni) taked power. For the moment spread remained contained, with the leader of “Fratelli D’Italia” reassuring the market going into the election, affirming intention to remain linked to west value and with no risk to have increased deficit in the next financial plan;

and finally we had the new UK government mini-budget, with tax cuts and risk of high supply. With LBI investors and pension funds heavily invested in gilts and leveraged using repo or swaps the spike in yield caused significant volatilitym prompting BOE to intervene buying unlimited size of long term gilts to calm the market. This is not a change of monetary policy but only a stabilization act.

Today we had also the Eurozone inflation print for September (Headline +10% and Core up to 4.78%). If you want a detailed analysis read my thread on it:

MARKETS:

Let’s start from RATES MARKET. It’s here that we had the bulk of volatility during the week. The week started with the usual rise in interest rates (treasury above 3.90% and bund above 2.30%). The movement was estreme (above 2 sigma move). The driver, in G10 was always a drift higher in real rate, while breakeven inflation continued to decline due to low pressure coming from oil and industrial commodities (with fear of recession). As talked above the BOE entered the market trying to stop the excess volatility on gilts and GBP and changed the trend of the week an all the market. Due to new announced government plan (not only UK but also Germany announced a 200bl plan to reduce cost for business and consumers) we started to see a good steepening move along the curve, but until we see central bank frontloading interest rate hike it’s difficult not seeing again a flattening.

On risky assets let’s start with CREDIT MARKET. Credit spread feeled the pressure coming from higher rates with euro cash IG widening 14bo and HY of 58bp. Borrowing it’s a the core of economic cycle. Central bank creates liquidity but it’s credit creation of banks that create economic growth. It’s for this that’s is extremly usefull to look at credit as a canary of the health state of economy (and of the market).

My usual framework is too look at intermarket relations. In september IG underperfomed govies (look at white line) and the ratio returned to the low of June. Economic indicators continue to go down and until we don’t have a stop in central banks we can’t have a bottom in bonds. This is needed to have a tradable bottom in risky assets too (IG, HY or equity). HY etf and STOXX equity followed down liquidity and returned to the bottom of the year. Remaining in credit land the ratio of HY to IG (in green) started to wake up, not pricing enough the risks of growth and downgrade we have ahead.

On EQUITY (given that fundamentals are the some of risky assets in general) I want to look on some technicals. We have the BofA Bull & Bear indicator that remain extremely bearish and in the second chart we have the AAII bull-bear at capitulation level too. Usually these levels are followed by some rebound.

I want to continue with some breadth indicators (% above 200moving average in SPX and numbers of advancers vs decliners). Clearly very bearish also here. Finally the Put/Call ratio at extended level.

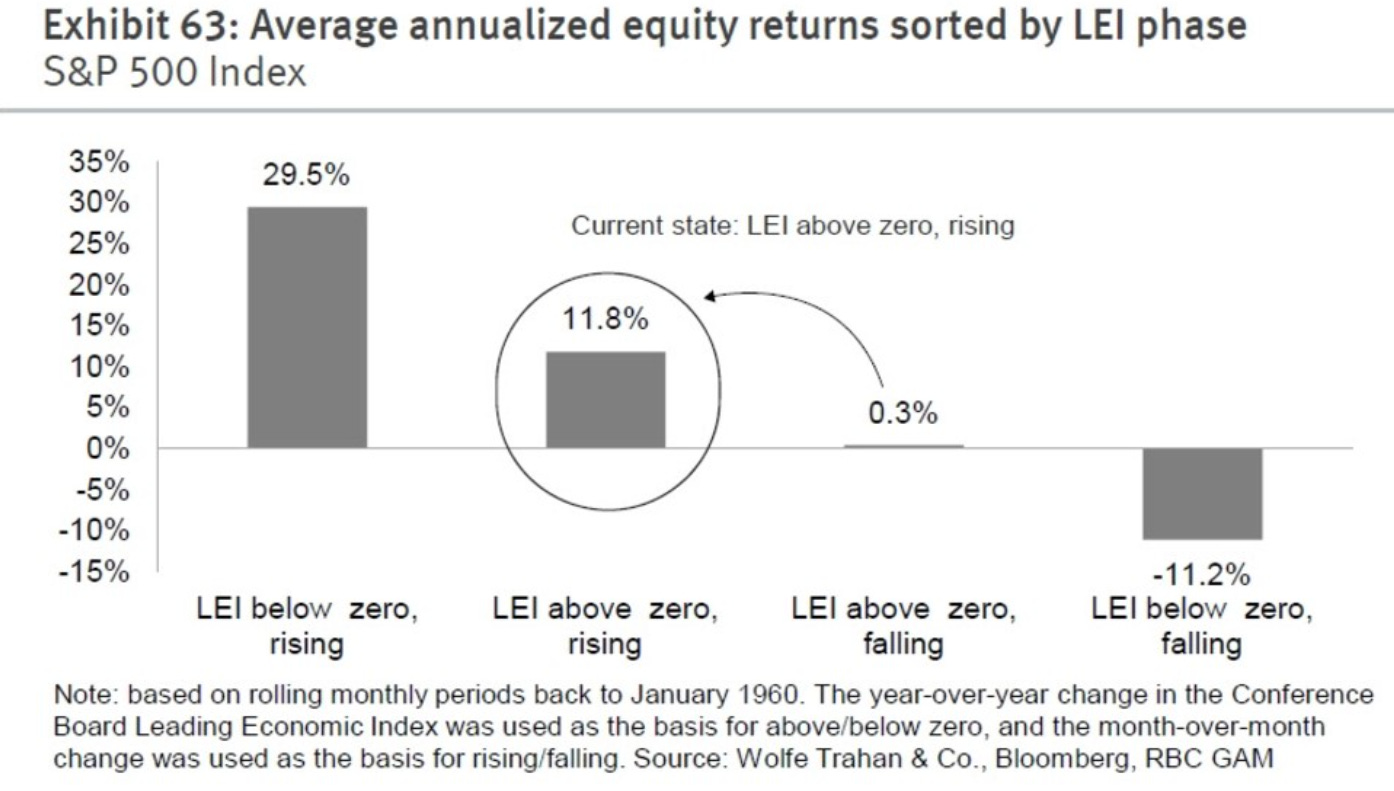

So despite sentiment/positioning is depressed (allowing some rebound as today, given it’s monthly and quarted end to) the driver of market direction remain liquidity (the most important fundamental). I calculate it as FED assets (will go down with QT) less TGA and RRP). Liquidity drives macro data, with LEI one of the different leading indicator now below 0 and declining. If you like to invest with market regime, it’s not a good one (chart from @macroops and RBC).

On CURRENCY dollar index stopped the uptrend this week thanks to some more active response by some central banks (this week we had BOE, following BOJ last week and PBOC). Until we have a coordinated actions by central banks the movements will remain short live, as JPY that returned near the top of weakness. As readed I read in an interesting piece of @johnauthers

“Central banks don't have enough ammunition. In 85-87 FX daily turnover was 200bln $, now it's 8.3trln $ per day. G10 FX reserves are 2.8trln $.”

MICRO:

Passing now on the micro, event driven or idiosincratic events we have:

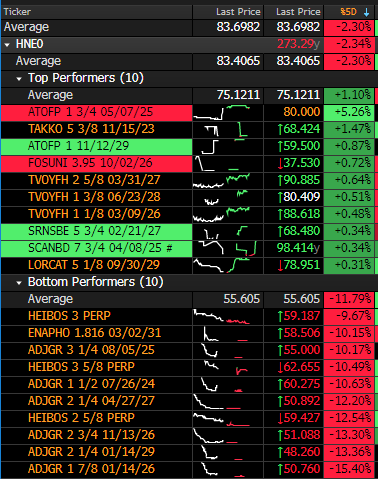

an other fall of ADLER/ADJGR bonds after the company took write down the value of Consus real estate after rising rates triggered pression across all Germany real estate;

ATOFP (ATOS) rebounded this week after receiving offer from ICG for EVIDIAN, but rejected it this morning;

TAKKO: despite higher cost impacted profit the bond remained resilient;

YULCN (Synthometer): bond dropped 4/5 after profit warning (EBITDA is seen 10/15% below the last announced). Inventories of medical gloves remain high with low demand. Weak GBP impacted also given bond and liabilities denominated in EUR/USD.

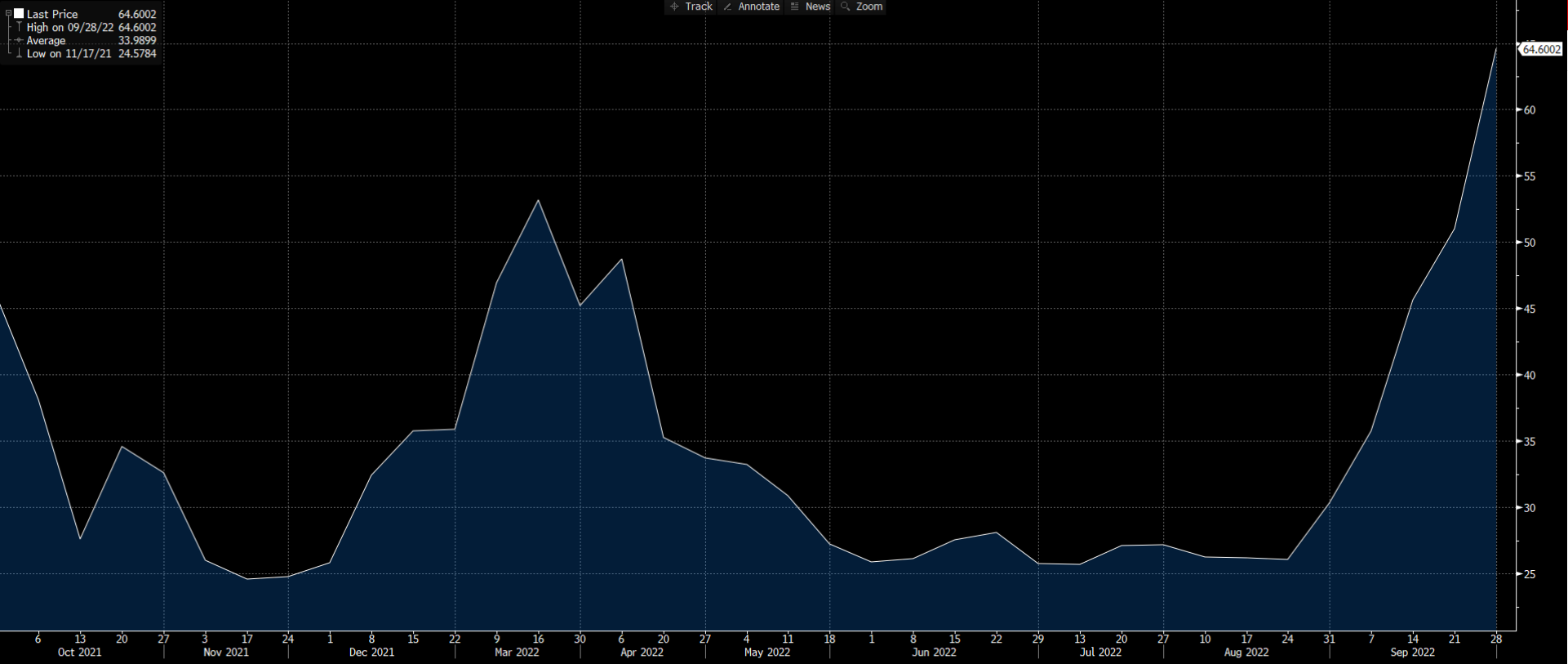

It’s all for this week. Given the environment the best strategy is to remain defensive and most liquid. Before to go. Do you remember the Rhine barge crisis (the low level of water not allowing barge to navigate)? Now the same arrived in USA on the Mississipi. This below is the rent price of barge almost used to ship corn and soybeans accounting for more than half of shipments bound for the world market:

Have a nice weekend.

If you enjoyed my job/analysis feel free to forward it to friends/colleague and remember to subscribe to the newsletter.

Bye Bye!

Great weekly recap before the next week, thank you!