Weekly Credit Market Review - Sept 16

Weekly Credit Market Review - Sept 16

A thread from macro to micro

Welcome back at the weekly recap, as usual at the end of the week. As always if you like my job/analysis please subscribe below and share it and I remember you that I am also on twitter at @Credit_Junk. And now let’s see what happened this week.

MACRO/NARRATIVE:

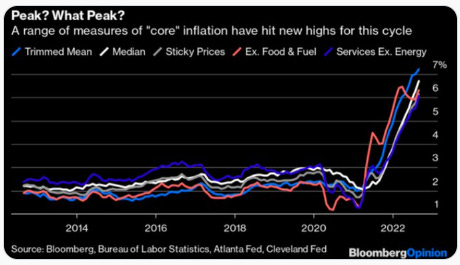

Without doubt the most important event of the week was the US CPI release (published the 13th of September) regarding the month of August. There was a lot of dovish expectation arriving at the data, with a lot of player expecting a sequential lower print. Here the results:

The headline data decreased from 8.1% to 8.3% (but above expectation for a 8.1%) while core inflation (ex energy and food) increased from 5.9% to 6.1%. On a monthly basis the CPI increased 0.1% vs the August data (after a weak data in July). Looking at contribution we have again a negative impact of energy, but a strong effect of services and goods. In service the big weight come from shelter and rent equivalent as usual. There is a big talk of the link of that part with house prices and the 18-24 months lag.

What matters at the moment is that all core inflation series (trimmed, sticky, etc) continued to go up and remain sticky (difficult to go down) and usually this part is more linked with wages, so less manageable by FED.

In the meantime in Europe the EU agreed on a plan to tackle the high energy prices but without an effective cap on imported gas price (difficult to apply). This plan, still to be approved, includes:

a cap (at 180 euro at MWH) on electricy prices for fuels like renewable and nuclear;

a levy tax on extra profit of oil/gas operator to help consumers

a plan to reduce consumption by 10/15% with mini-blackout in peak hours

Together with European plan the various governements in the meantime go alone:

This week Italy approved a new aid plan for 13.5bln for consumers and businesses

So, if we have a scenario of lower sequential growth going forward (we talked several times of various leading indicators like PMI, ISM, etc), from a policies point of view we have:

DM central banks that increased their hawkishness. They are determined to low inflation and are frontloading their moves;

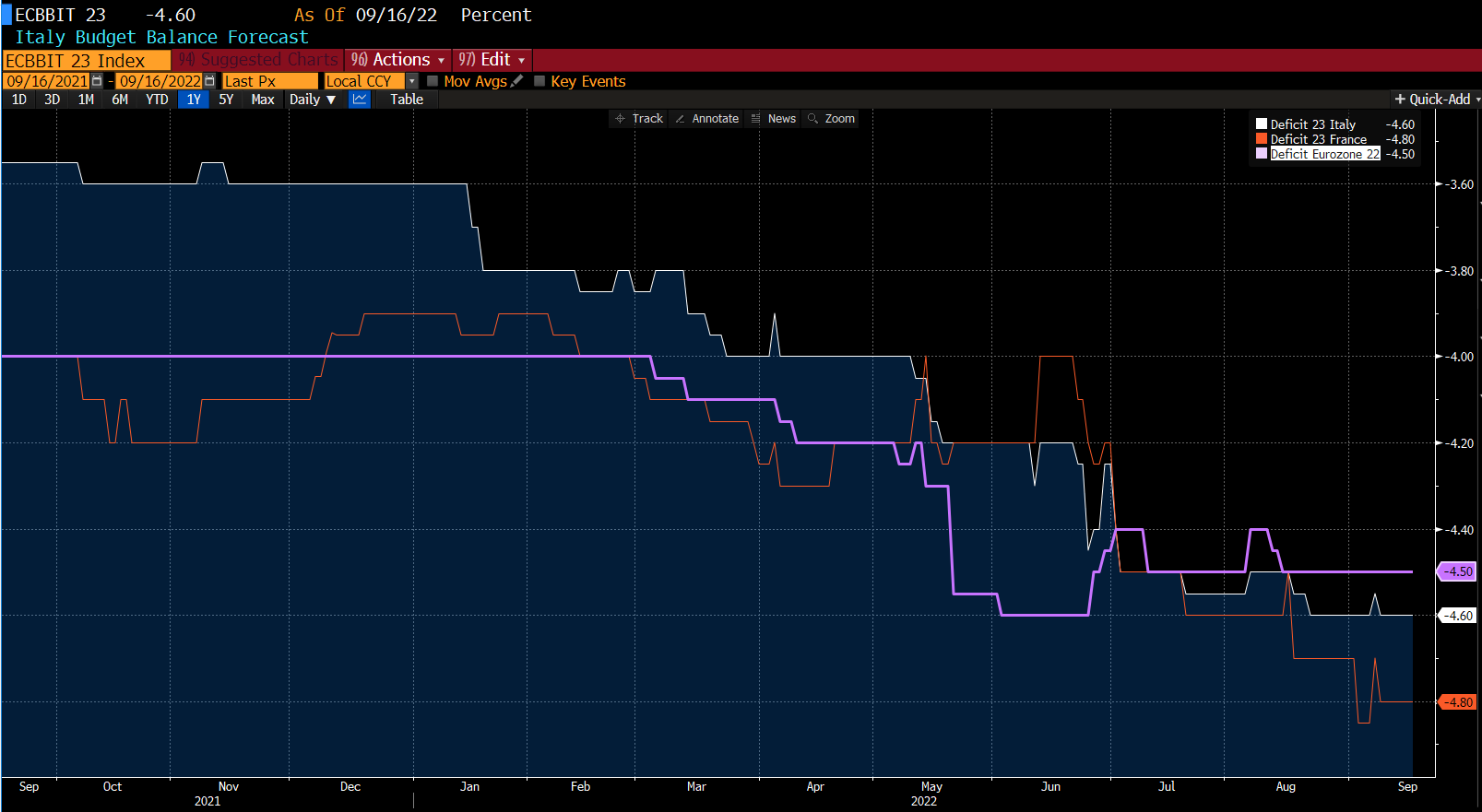

Government that increased the spent at support of consumers (especially in Europe). The budget deficit, that in Europe is at -4.5% this year will increase in some countries also in 2023. Below the path of Italy and France for 2023. This doesn’t help to reduce quickly the inflation problem.

MARKETS:

The first market to investigate is clearly the rates market. Below there are the bund and the treasury futures. Given the higher than expected CPI, rates increased with TY returning to the low of June.

The move was driven in United Stated almost by an increase in real rates, while in Germany also by an increase in inflation expectation given the stimulus we talked above.

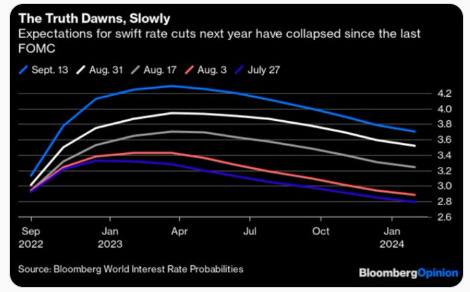

The expectation of frontloading on FED increased the terminal rates (now above 4% for next year). This is the same also for ECB, with a strong flattening move on both curves.

I want now to spend some words on FX. The weakest currency of G10 is clearly JPY, that arrived at 145 vs USD. The driver is clearly the divergent monetary policies between FED (very aggressive) and BOJ (very dovish continuing to do YCC). But this week BOJ conducted "rate checks" (so a verbal intervention) meaning asking to traders some prices. This stopped the move at 145, signaling at the market where is their put.

That won’t work for long but it’s interesting. If you want to know more about BOJ and FX, have a look at this thread:

BOJ conducts "rate checks" - Nikkei. The way intervention works (in Japan, and often in other places) is first they start talking about the level of the asset. That is "jawboning" or "verbal intervention" ("口先介入"). In Japan, this has been going on since March-ish.日銀が「レートチェック」 為替介入の準備か https://t.co/0vM9g8GhUb

BOJ conducts "rate checks" - Nikkei. The way intervention works (in Japan, and often in other places) is first they start talking about the level of the asset. That is "jawboning" or "verbal intervention" ("口先介入"). In Japan, this has been going on since March-ish.日銀が「レートチェック」 為替介入の準備か https://t.co/0vM9g8GhUb 日本経済新聞 電子版(日経電子版) @nikkei

日本経済新聞 電子版(日経電子版) @nikkeiAlways this week, the yean sinked below 7 per dollar, weigheted by the strong dollar but also from the very weak environment of other asian currency (JPY and Won).

On equity this stagflationary regime (of high inflation and declining growth) together to rising rates and high correlation of bonds vs equity produced a very negative performance (with S&P arriving at -3% and Nasdaq at -5%). Clearly equity was pricing a “peak inflation” scenario and a pivot by FED.

So, despite the very light positioning of fast money (below the positioning of CTA/HF on S&P futures), what drives market is always liquidity.

Below my intermarket analysis of govies/credit/and equity (here on european assets) showing than the IG/govt ratio (in white) returned to go down, putting pressure clearly on HY and Equity.

Investing (especially in fixed income) is a relative value game, so with rates incresing, some assets appear better than other and also giving money to central banks is not so bad). The decreses of IG to Govt show exactly this, with investors that prefer government bond to corporate bonds (why buy a BBB when you can have a 1.5% buying a german bund with 2y maturity).

In credit land as I feared the HY/IG started to fall, despite remaining extremely high and, for me, not compensating enough for recession risk. Looking at spread on the week we see a bearish price action with cash and CDS widening (IG and HY cash index widened 3/4bp). But the the true widening is visible looking at ETF (here HY spread widened 40bp and IG 7bp) as showed by the fall in the HY/IG above (that use ETF).

MICRO:

Looking finally at movements on bonds on the winner side:

METINV/ENAPHO are two ukraine stressed name. The rebound maybe related to the better news coming from the country, with Ukraine army advancing on the east.

On the looser camp we have:

FOSUNI: the situation deteriorated further. China asked banks and SOE to report their exposure to the conglomerate and this week S&P downgraded the issuer to BB- on narrowing liquidity and shortening of debt maturies

ZFFNGR and INEGRP: both names had the worst drop in 6 months but without a clear newflow and while for INEOS there is the risk related to gas price and the fall of GBP, during this week Moody’s affirmed ZF Ba1 rating, and upgraded outlook from negative to stable.

It’s all for this week. Given the environment the best strategy is to remain defensive and most liquid. Remember that bear market has 3/4 stage. The risk is to confuse the rebound for a new bull market.

Have a nice weekend.

If you enjoyed my job/analysis feel free to forward it to friends/colleague and remember to subscribe to the newsletter.

Bye Bye!