Weekly Credit Market Review - Sept 02

Weekly Credit Market Review - Sept 02

A thread from macro to micro

Welcome back to all readers. We passed the threshold of 800 subscribers for this newsletter and the twitter profile (@Credit_Junk) is now above 4.100 followers.

Before starting I want to show you a twitter account and their associated substack (@pav_chartbook) that each day collects a lot of charts from markets and sellside banks.

As always if you like my job/analysis please subscribe below and share it.

I returned yesterday from my holidays (I promise you that it’s all for this summer) so this weekly edition will be slighlty different from usual (I was not here to follow all what happened) and will be focused on what I looked once returned at my terminal.

NARRATIVE and MARKET UPDATE:

All the week passed under the shadow of what happened Friday at Jackson Hole with Powell confirming their intention to going deep to fight inflation and suggesting us to prepare for lower growth and high market volatility. Payroll today was robust enough to give greenlight to an other 75bp by the FED with high partecipation rate and high unemployment rate (from 3.5% to 3.7%) but at the end of the day we need to wait also the August CPI (September 13th) to undestand better the path of inflation and if we reached the top or not.

Liquidity:

The first chart to look is liquidity conditions.

Earnings don't move the overall market; it's the Federal Reserve Board... focus on the central banks, and focus on the movement of liquidity... most people in the market are looking for earnings and conventional measures. It's liquidity that moves markets. (Stanley Druckenmiller)

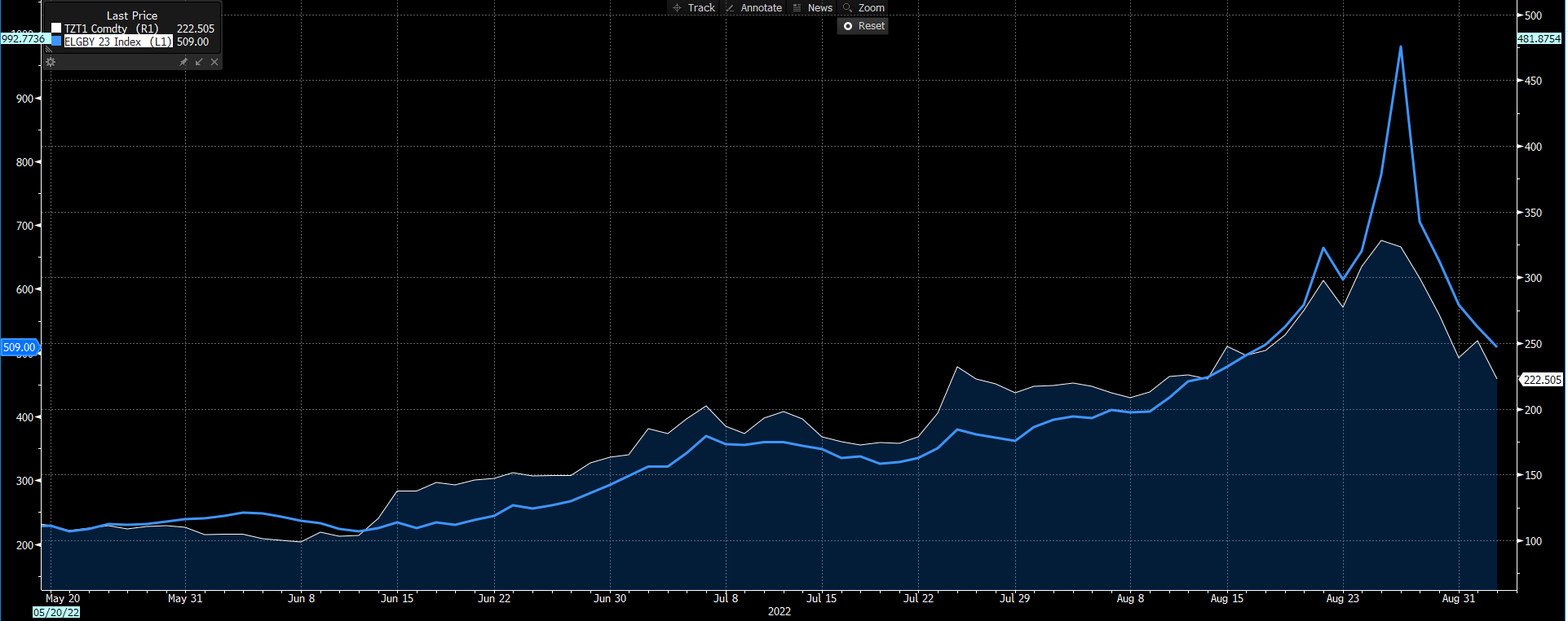

From mid-august HY ETF dropped and CCC OAS widened returing at their max level above 10%. Credit is one of the most important part of liquidity, so following it help you to undestand direction of travel.

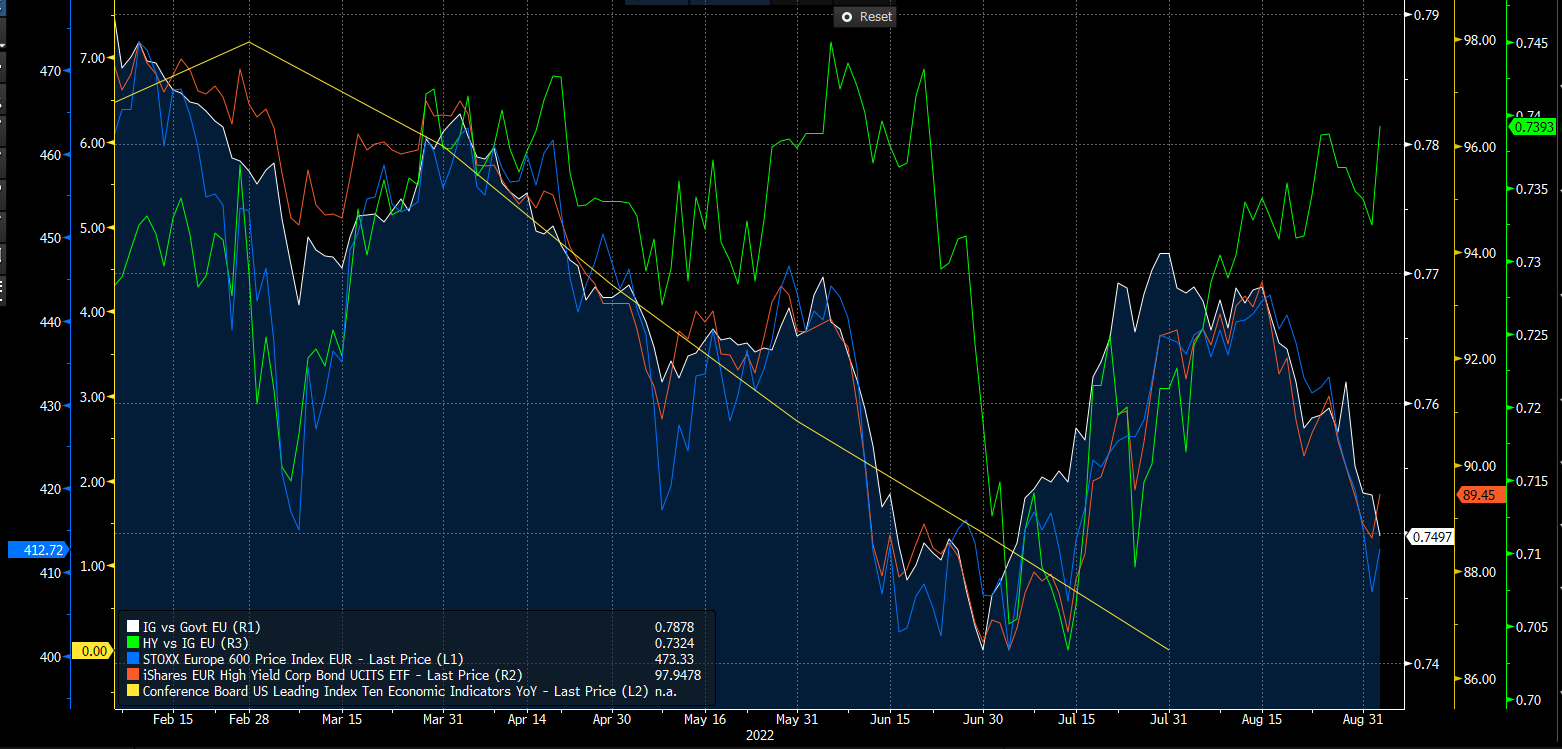

The same happened at the estimate of FED liquidity where assets decreased and RRP-repo increased (reducing liquidity too). LEI (a blend of ten economic indicators calculated by Conference Board) is at 0%. If it continue to fall (and I expect so) the environment for stocks is one of the worst.

Rates Market:

With central banks need to restore market confidence on their ability to fight inflation, terminal rates for FED and ECB returned to rise with 75bp almost priced for both at the September meeting. Long term rates for US and GER returned above 3% and near 1.5% respectively, remaining in their 6 months lateral range.

Commodities:

Despite the good news regarding new stimulus in China the country continue to remain in lockdown environment (Shenzhen, Guangzhou and Dalian are under restrictions again) and this put pressure again on industrial metals and energy too.

Oil remains in a tight range (Brent between 90 and 103). Liquidity in futures market remains tight so exacerbating price move, but I think fundamentals on physical remain tight. Below a thread I wrote about spare capacity of Saudi Arabia summarasing the view of Goehring & Rozencwajg.

We need to talk also of gas price in Europe and electricy prices. Despite flow from Russia via NS1 are again at 0 (yes a new maintenance period) the TTF gas price fell from 330 euro for MWh to 225 and power price followed the same path. What moved the price was a statement from Ursula von der Leyen saying EU is preparing a power market emergency intervention. We will see what EU is preparing but I doubt could change a lot.

Clearly a better calculation of power prices (and the merit order) with less link to nat gas (the price setter) could help. The move is exacerbated by the illiquidity in the market and the closing of hedged position by energy traders. Here a simple chart of how the Merit order works in determing the electricity price If there is enough renewable generation is used before but electricity price is settled using the marginal power plant (and their cost).

Credit markets:

I’ll comment the move of ITRAX XOVER (CDS for HY european market) but the idea is the same for all segments almost. After the bottom at 450 at mid-august, the new narrative after Jackson Hole was for a hakwish central bank again and spread widened until 600bp. Today after payroll data (seen as a goldilock from market given the solid job growth and the low wage pressure) spread returned to tight (only today -20bp).

Positioning in credit market remain light and this (like in the equity market) can explain the movement of today, typical of short covering.

And finally looking at intermarket relations IG/Govt (white line below) returned to suffer (typical in a rising rate environment), confirming the weakness in HY and equity too.

The only part that doesn’t fit is the outperformance of HY vs IG (the green light below) but in June too we had a similar movement with IG more sensitive to rate immediately. HY, more sensitive to growth, woke-up later after realizing the impact of high rates on growth.

Equity markets:

ES1 in August is like a page of the typical technical analysis book. After the rally that started in mid-june with a lot of people started to call a new bull market, the index touched the 200 days moving average and returned to fall again.

After a small rebound in sentiment (I use AAII) that returned near 0 the delta in bull vs bear returned negative, but not extreme like in June.

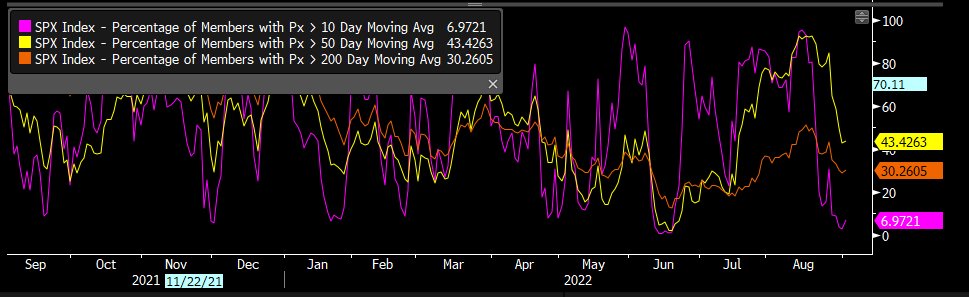

Positioning in equity is a mixed bag (with futures net positioning very low, while flow in funds and ETF continuing to remain solid) while breadth is very weak again with % of stocks above 50 days moving again back from the high.

FX:

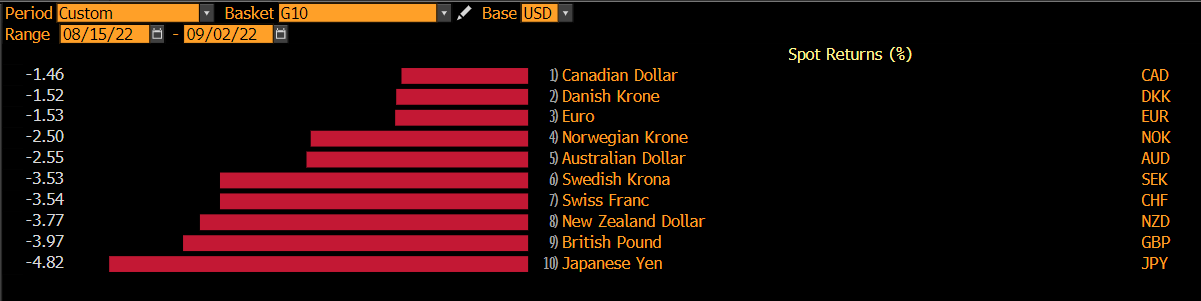

Dollar was the king again with FED hiking draining liquidity globally and weighting so on EM currencies. DXY broke past high.

Looking across G10 GBP and JPY were the clearly losers with UK fighting with high inflation while Japan suffering from “relatively” dovish central bank and a high energy bill on their import (trade surplus wiped out).

Note of service:

From next week I’ll return to the usual format looking at narrative-market and micro view on credit market. As explained above I returned from holidays today after a 2 weeks break and I thinked could be usufull to look at market from the top to have a better picture of the direction. It’s exactly my routine I hope could be usefull for someone too.

If you enjoyed my job/analysis feel free to forward it to friends/colleague and remember to subscribe to the newsletter.

Bye Bye!

Great work as usual!