Weekly Market Review - 03 Mar

Weekly Market Review - 03 Mar

A thread from macro to micro

Welcome back at the weekly recap, as usual at the end of the week. As always if you like my job/analysis please subscribe below and share it and I remember you that I am also on twitter at @Credit_Junk. And now let’s see what happened this week.

MACRO/NARRATIVE: This week macro reinforced, again, the narrative of stronger than expected economy (no-land) but with high inflation (reflation) with some leading indicators for February in the same direction of better hard data as retails sales.

In US the ISM Manufacturing remained stable at 47.7 (slightly lower than exp. 48) but orders and price bounced back, pointing to persistent price pressures).

Today ISM Services was almost flat passing from 55.1 to 55.2 (better than expected at 54.5), and price pressure of price paid continue to recede. But some others forward looking indicators: employment (strong) and new orders (rebounding) project an economy strong but with a job market that remain tight (aka risks of wages pressures).

We had also the PMI for eurozone countries, that showed a weakness for central economies (France and Germany), while peripheral countries as Italy and Spain moved to expansionary. The manufcaturing indicator remained flat in February (always below 50) while the services indicator contracted slighlty but remained in expansionary territory.

But the biggest positve news arrived from China, where the PMI (for manufacturing and services) had the biggest improvement in the last decade. Manufacturing improved from 50.1 to 52.6 (exp. 50.6),, services from 54.4 to 56.3 (exp. 54.9) while composite from 52.9 to 56.4. This was the first data after Covid restriction were removed and confirm that recovery is broadbased and economy is in a better shape.

But a strong economy, despite central banks removing liquidity and hiking rates, has an other side of the story: higher price pressures. Preliminary Eurozone inflation for February confirmed it, with higher and stickier inflation (after the stronger than expected print in Spain and Germany last week).

a headline inflation falling from 8.6% to 8.5% (higher than 8.3% expected)

a core inflation increasing from 5.3% to 5.6% (expected at 5.3%);

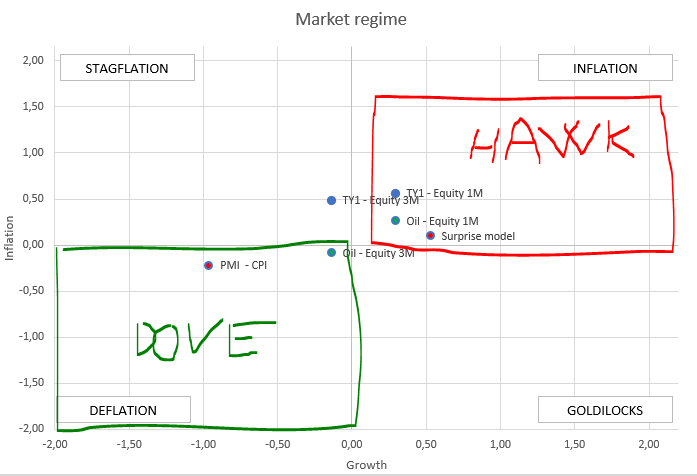

In a quadrant regime investing framework a posive growth with positive inflation we should fit the “Inflation” quadrant and on average it’s in line with price action (of treasury, oil and equity). Each quadrant requires a different response by central banks and this one is for a “hawkish” one.

This week we had:

Lagarde (ECB): “more tightening is needed if fiscal cooperation is absent”;

Bostic (FED): “continued rate hikes are needed, above 5%”;

Kashkari (FED): “much of indications CN hikes not slowing into services”

Wunsch (ECB): “if we don’t get clear signals that core decline, looking at 4% terminal rate would not be excluded”

Bostic #2 (FED) :”FED is in a position to pause rates hike after summer”, with this one maybe a correction maneuver, correcting on the dovish side

MARKETS:

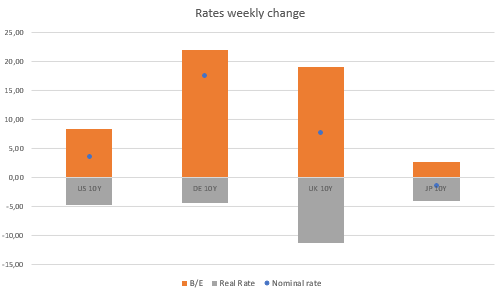

The "hawkish” tilt by central banks continued to reprice the terminal rate with 3.88% for ECB and 5.42% for FED pushing interest rates higher on both sides of Atlantic.

US 10y treasury returned near 4%, while Germany 10y arrived touching 2.75%. For both, but especially for euro area, the big driver was a repricing higher of expected inflation (breakeven).

The performance of credit market was mixed, with synthetic (CDS) and HY, performing well and following growth driver, while cash following the drift higher in interest rates (due to higher duration sensitivity).

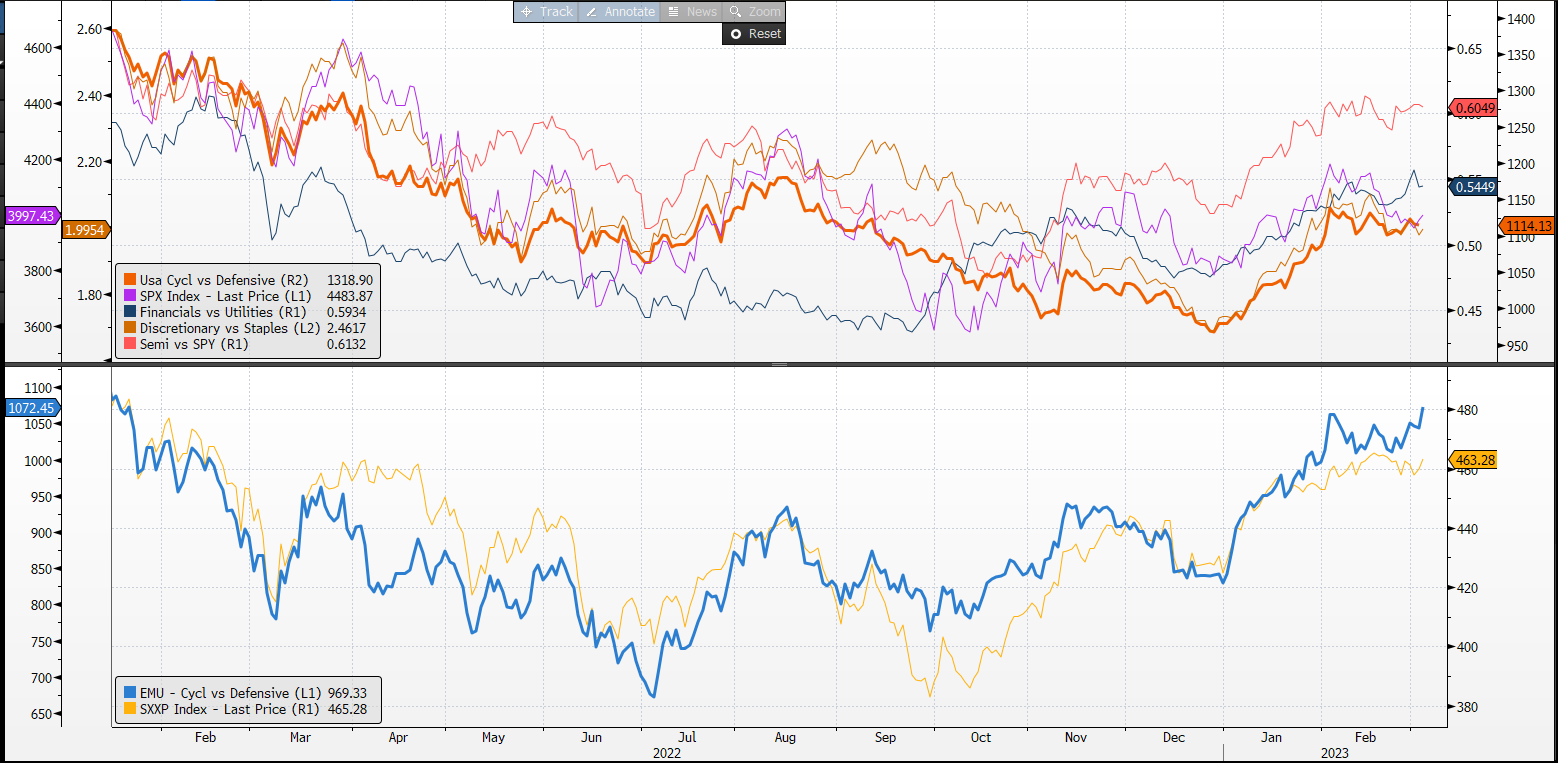

Also equity market performance was good this week (SXXP +1.2%, SPX flat) and volatility (VIX, V2x, SKEW) that continued to compress. Positioning is sure a an explanation, but not only. Various internal indicators (Cycl vs defen, discretionary vs staples, Financ vs Utilites and semi vs spy) remain strong and don't confirm the weakening of SPX of last week. European cyclical vs defensive is particularly strong and driven by the big weight (and big performance of European banks, supported by the high level of profitability in their banking book).

As said by Druckenmiller, the best economist is inside the market (a reason to look at internal indicators and breadth of the market). Do you want further clues? Look at Cyclical/Defensive vs ISM.

MICRO:

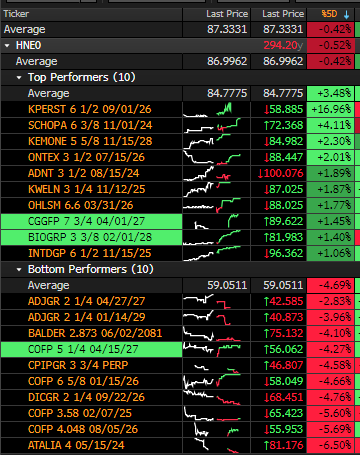

ATALIA (La Financiere Atalian): the big movement on the 2024 bond was related to fund managers selling the bond, with some player buying the 2025, with investors assuming an extension of corporate action to the 25s.

Two companies reported good results and performed well:

KPERST: (Kloeckner Pentaplast): reported results this week with EBITDA at 66M (up 45%) and sales up 6%. Net leverage down to 6.7x.

ONTEX: reported good 4q and FY 22 results, with revenue +24% and EBITDA up 31%. Good volumes of sales and cost reduction strategy

It’s all for today. I hope you enjoyed my job/analysis. Feel free to forward it to friends/colleague and remember to subscribe to the newsletter.

Grazie

Macro - especially - is like one big jigsaw puzzle.