Weekly Market Review - 10 Feb

Weekly Market Review - 10 Feb

A thread from macro to micro

Welcome back at the weekly recap, as usual at the end of the week. As always if you like my job/analysis please subscribe below and share it and I remember you that I am also on twitter at @Credit_Junk. And now let’s see what happened this week.

MACRO/NARRATIVE: after last week, where we had an intense central banks schedules (with FED/ECB and BOE) and the stong NFP print (that confirms a scenario of stronger than expected H1), this one was more quite in term of newsflow.

Despite this, the central banks, through verbal interventions, have tried to return to a more hawkish rhetoric:

BOSTIC (FED): “we could rise rates higher than expected”

POWELL: “more hike needed if job market remain strong”

but Powell missed also the opportunity to go against the easing of financial conditions, highlighting also that disinflation began (he used 17 times the world “disinflation” in his speech).

So going into next week where all the focus will be on the US CPI number for January (with surveys pointing to a new drop to 6.2% yoy from 6.5%) just today BLS revised up all the previous months (December from -0.1% to 0.1% MoM, November from 0.1% to 0.2%, etc) questioning so the narrative of deflation.

Always next week the government will nominate the news BOJ Governor. Local newspaper in Japan point to Kazuo Ueda, an academic professor ex BOJ member, as a new governor. While market initially thinked it as a hawkish choice, not being in the list of possible candidates, in several occasions Ueda confirmed that could be risky to rising rates to early given the economic situation. It is important to remember that he was on the board between 1995-2005, so he is one of the fathers of the ultralow rates interest rates policy.

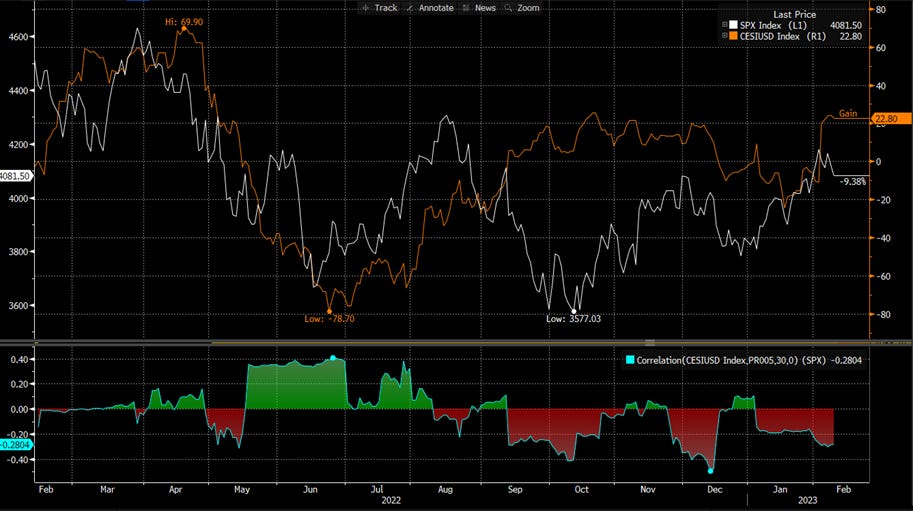

A interesting point (that I read in a Citi quantitative research) was the analysis of surprise index (up recently thanks to strong job market and ISM services) vs stock market. Here we can see that correlation is negative, so basically we can read it as “good news is bad news”, with market realizing that a too hot economic scenario could force the hand of central bank (the FED) to go ahead with their hiking path.

Some closing words about geopolitical risk (yes it remains, despite nobody prices it now). This week USA imposed a 200% tariff on aluminum produced in Russia, while on oil, Russia announced to cut production by 500k barrels a day, retaliating against sanctions. Actually Russia produce 11M barrel per day.

MARKETS:

Given this oil is trying to bounce from the 80$ per barrel level (look at prompt time spread returing in backwardation too).

The impact on interest rate was a return of traders adding back bp to the terminal rate with FED fund now back to 5.25% in June/July (below), while ECB depo rate near 3.5% for September.

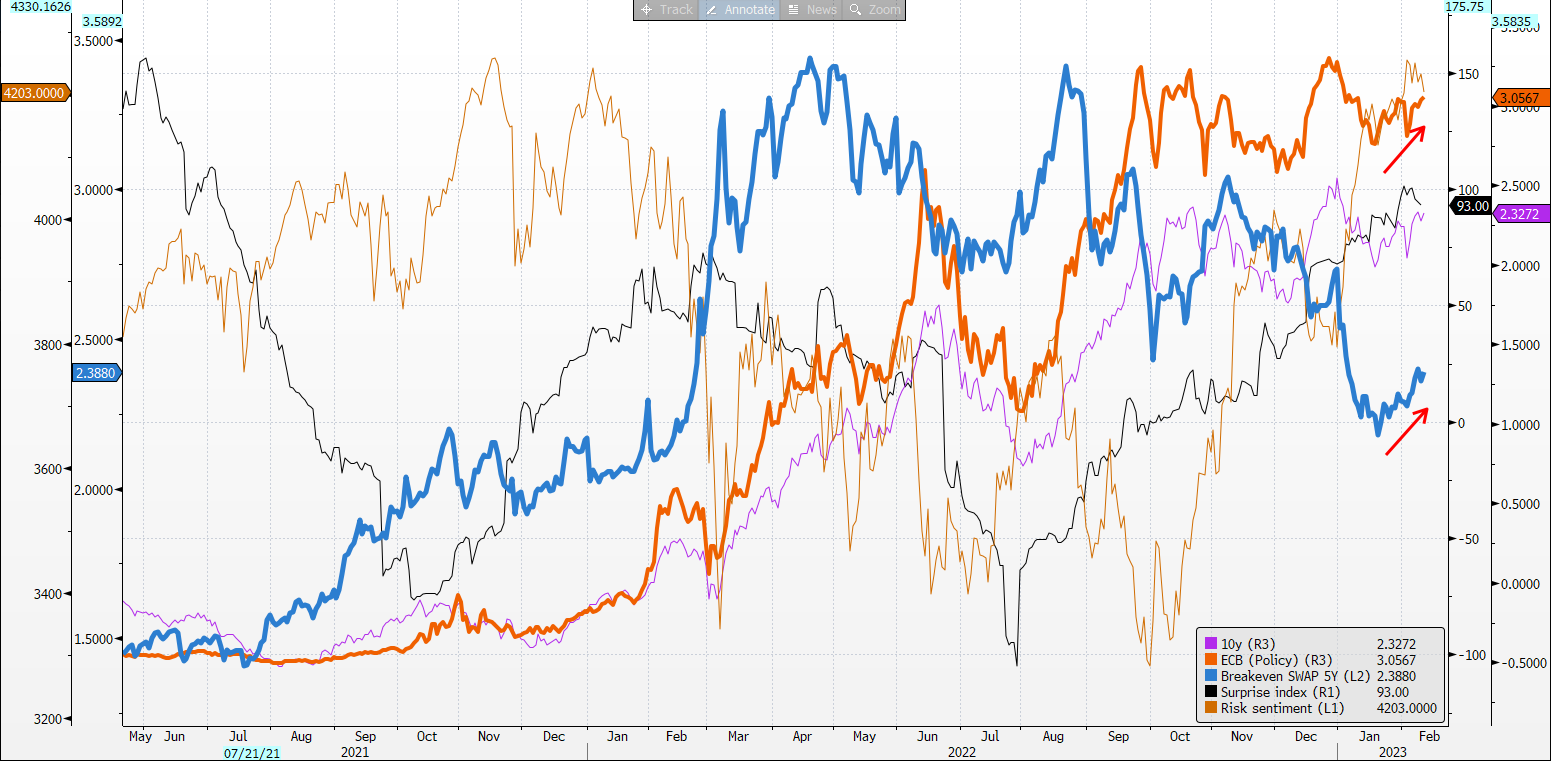

On the 10Y bund rate (that I use to read the drivers of the movements and below in pink) it is clear a rebound in breakeven inflation (below in blue the 5Y ZC infl. swap) and in policy rates (in orange the 1y1y eonia). The week close with 10y USA at 3.60% and 10y Germany at 2.30%, with a return of flattening for short term curves (2-5), while the long term (10-30 and 5-10 more stable and with a bias to steep).

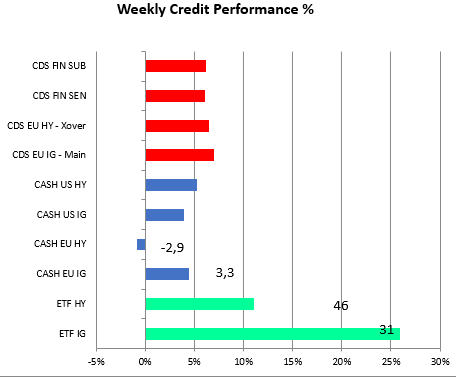

With pressure on rates credit we started to see new pressure on credit again (rates and credit are the first source of liquidity). IG, more related to duration risk, widened 3/4bp but the true widening could be seen in ETF where the widening was of 46bp for HY and 31bp for IG. Also CDS widened, an indicator that 70bp for Main and 400bp for XOVER are too tight given the risks that remain.

Using now the IG/Govt ratio as a proxy for liquidity there is no divergence with equity market (below I use Stoxx Europe) but the movement maybe too extended in the short term.

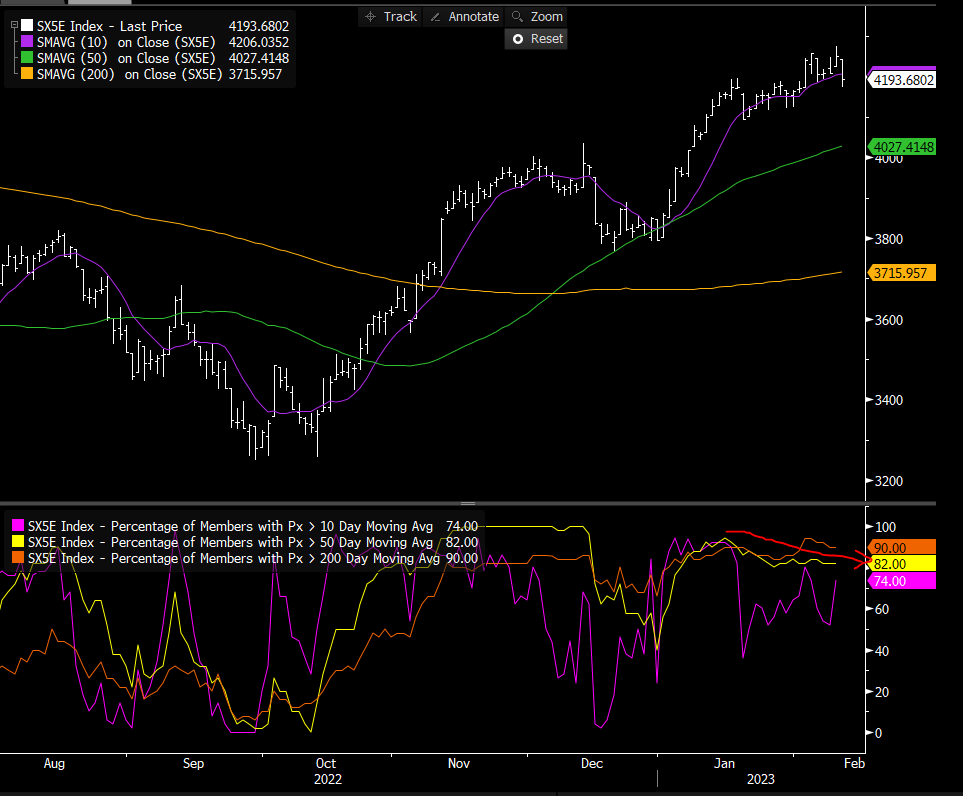

Looking also at some breadth indicators, (in the technical tools) the percentage of stocks trading above 50 day moving average, started to decline from 90% confirming the short term overbought, but positioning on equity in general is not yet long, despite no more short as in the past.

Market entered the year short positioned on risky assets (with the fear of a recession in H1) and given the better than expected data started to cover the shorts (below the AAII Bull and Bear) and the Citi Macro risk index (more a short term indicator).

MICRO:

On the micro part I want to focus on some big movement and special situation stories:

HNDLIN (NOVELIS) a metal and mining company specialized in flat rolling of aluminum and aluminum base alloy was impacted by the news of 200% tariff on aluminum but especially by reporting season with company missing 3q earnings. Despite sales are up +5.75 yoy, the higher cost impacted margin, with EBITDA down 48% yoy

TEVA: reached an agreement with Florida to settle an old claim regarding price settle, paying 6.73M$.

CTLT (CATALENT) despite a mixed Q2 earning results (with revenue decresing 6% yoy and EBITDA down from 310M to 283M and margin at 25%). The good news are the extended partnership with Moderna supporting the productions of multiple products and the interest of Danaher for a takeover of the company.

It’s all for today. I hope you enjoyed my job/analysis. Feel free to forward it to friends/colleague and remember to subscribe to the newsletter.

On my twitter profile I created a list dedicated to credit. Great accounts there.

🙏