Weekly Market Review - 10 Mar

Weekly Market Review - 10 Mar

A thread from macro to micro

Welcome back at the weekly recap, as usual at the end of the week. As always if you like my job/analysis please subscribe below and share it and I remember you that I am also on twitter at @Credit_Junk. And now let’s see what happened this week.

MACRO/NARRATIVE: Looking at what happened this week we can divide it in some homogeneous groups:

Growth:

Regarding growth we had the end of the China Congress that revised down the goal of growth to 5% with policymakers unlikely to employ any large scale stimulus as in the past with a focus more on consumptions- This will have for sure an impact on the future path of commodites (with less support for industial commodities like iron-ore and copper if not strictly linked to the “green energy transition”;

US job market: US consumers are the other big demand driver, with China. Job opening printed slighlty down this month but remains at high level. Taking a chart of MI2 Partners is interesting to note that quit rate declined recently. The direction is right but job market remains tight.

US job market (2): Today NFP showed +311K new job (strong) but average hourly earnings MoM slightly lower than expectation at +0.2% MoM with unemployment rising from 6.6% to 6.8% and pertecipation rate rising. The report is mixed with robust labor demand (tight job market) but better capacity to fill it with supply.

Central banks:

RBA (Australia central bank): Central bank hiked by 25bp as expected but in forward guidance they started to talk of a possible timing to stop their action, considering cumulative path and the impact on real estate prices.

BOC (Bank of Canada): as expected Bank of Canada mantained rate on hold at 4.5%, saying that job market remain tight, inflation easing is slow and they are prepared to hike again if needed. Just remember that BOC started the hiking cycle before FED this time.

FED: Powell appeared in front of Congress this week confirming that officals are ready to speed up their pace of tightening (from 25bp to 50bp again) if data remain strong enough, despite not yet decided it. If inflation will remain high they could take rate higher than initially expected (to 6% ??) and that disinflation road will be bumpy, at least.

Banking System:

This week SVB (Silicon Valley Bank) was under big stress. The bank is VC focused bank, taking deposits from VC new companies and make loans as a traditional bank. The big inversion of US rates curve, together with the difficulty of the technology sector created an environment of reduction of deposits, with the bank forced to liquidiate a 21bln treasury position held in A-F-S (available for sale), taking a loss of 1.8bln. The bank was so forced to announce a 2.25bln capital increase. The company lost 60% of capitalization in one day, with KRE (the ETF of the small regional banks strongly underperforming the market). I would not consider this as a systemic phenomenon, rather idiosyncratic, as the regulation for small banks is totally different from systemic banks, despite the so inverted yield curve puts business model of traditional banks in difficulty, which finance themselves in the short term and make long-term loans.

MARKETS: Below the market dashboard for the week.

The move of the week is without any doubt of risk-off with equity loss across countries (SXXP -2%, SPX -1.5% and EM 2%). Bonds yield went down strongly in in the US (-15bp) and in Gemany (-20bp) driven totally by breakeven, with market betting against the ability of central banks to hike rates as initially feared. Terminal rate declined from 5.75% to 5.40% for the FED and from above 4% to 3.8% for ECB.

From a cross asset point of view, looking at my “All in 1” chart, let’s look at what the various asset classes have to say:

Commodities: Silver/Gold and Copper/Gold down;

FX: KRW (Korean Won), a proxy of global growth down;

Bonds: IG to Govt (both US based) down, not so much but some stress in credit;

Equity: Banks to Utilites down;

Different asset classes but 1 signal: less growth ahead

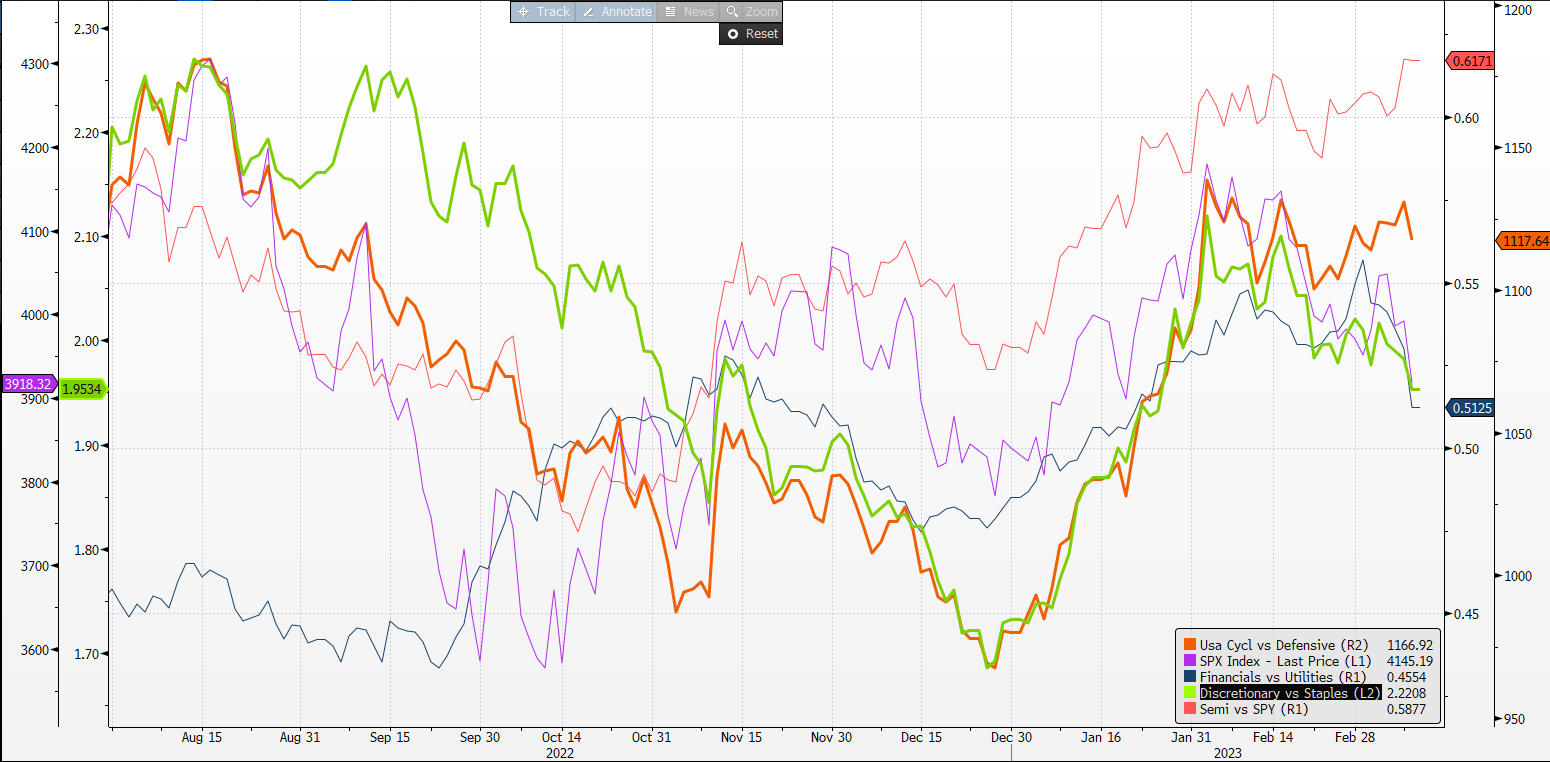

Remaining on equity and on the internal forces of the SPX, the various indicators are weak (discretionary vs staples add to financial vs utilities saw above), despite cyclicals vs defensive and Semi vs SPY don’t confirm totally the weakness.

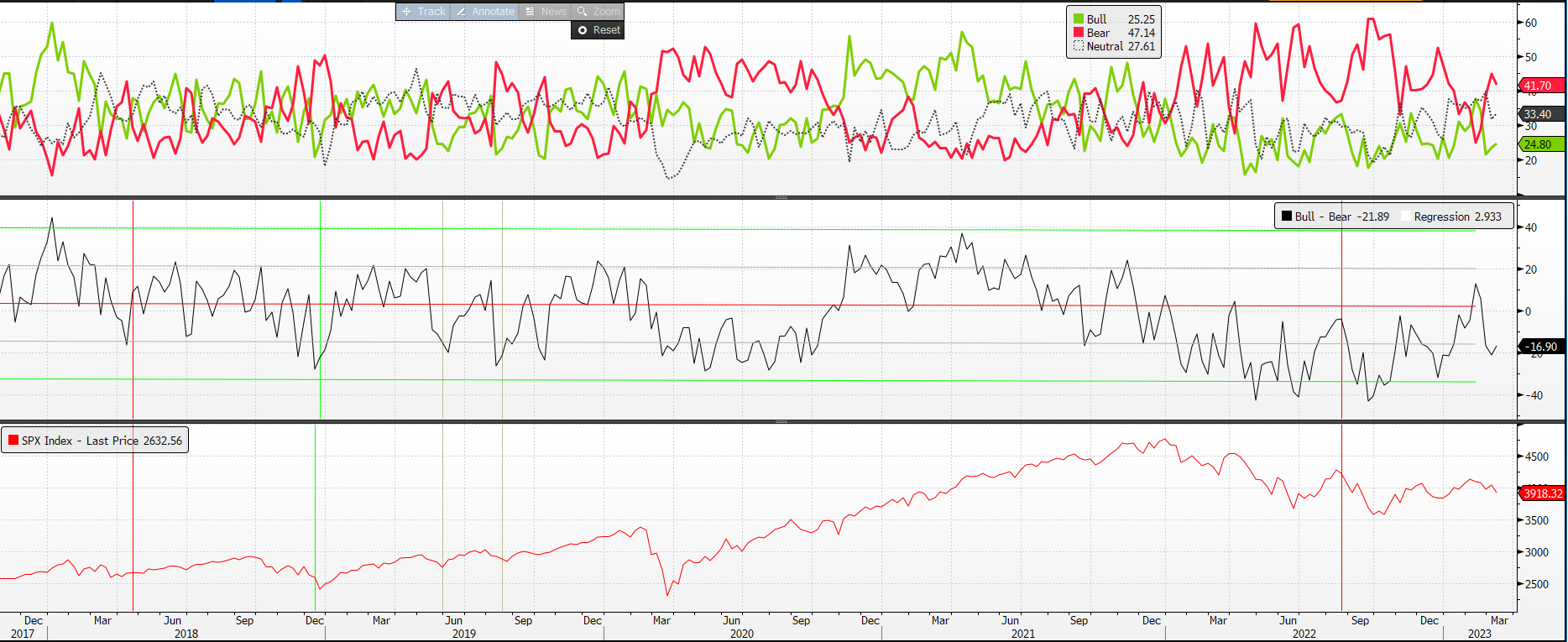

Sentiment is mixed, with PUT/CALL ratio bouncing from a bottom and usually a bearish indicator (as I learned from my friend @ExcellRichard) while in second chart below the AAII Bull-Bear returned in bearish land.

Passing on credit now the fear regarding the banking system impacted the spreads with widening of 16bp and 2bp on EU HY and IG. The true stress is visible more looking at the widening in implied spread of ETF with HY widening by 60bp and IG by 33bp.

Looking more inside credit we can see IG continuing to underperform govies (in white) a canary for HY (in orange) and equity (in blue).

Interesting also the decompression between HY and IG (in green), a first indicator of growth risk.

MICRO: we conclude as usual with micro/idiosyncratic news moving single bonds.

COFP (Casino): companies missed the trading profit for FY2022 estimated by analyst with a strong deterioration in operating performance. FY EBIT is at 1.12bl (below 1.2bln estimates) while 2H down -6.8% YoY. Margin stable while FCF remain negative and leverage remain high. Very negative price action also after the company announced plan to merge French stores with Teract SA. Very weak price action;

EGBLFN (EG Global): the report was not strong (with EBITDA -9% yoy) but the boost on bond arrived by the news of 1.5$ bln sale and leaseback of some stores (415 US stores);

CLNXSM (Cellnex): results confirmed good fundamentals with revenue and EBITDA higher than expectations. FCF generation remains storng. They confirmed their focus to grow organically and the delevaraging plan to achieve the IG rating in 2024 by S&P.

It’s all for today. I hope you enjoyed my job/analysis. Feel free to forward it to friends/colleague and remember to subscribe to the newsletter.

great coverage, thank you!