Weekly Market Review - 17 Feb

Weekly Market Review - 17 Feb

A thread from macro to micro

Welcome back at the weekly recap, as usual at the end of the week. As always if you like my job/analysis please subscribe below and share it and I remember you that I am also on twitter at @Credit_Junk. And now let’s see what happened this week.

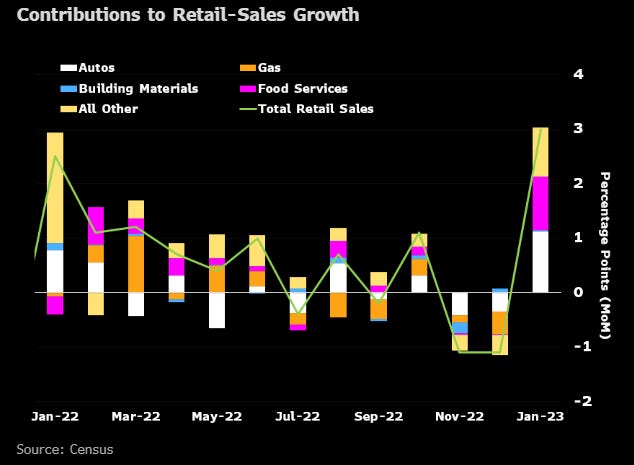

MACRO/NARRATIVE: This was another week of macroeconomic data further push back recession risks, with better-than-expected growth data from the US. We had, in fact, a strong print of retail sales (+3% in January MoM vs expectations of +2%; ex auto +2.3% vs expectations of +0.9%). Despite the autos contribution is due to some forced buying after a bad weather in December, the overall figure is strong for sure.

An other strong figure was related to manufacturing production (up 1% in January and higher than expected). But the true driver of sentiment was the US CPI print, that came slightly higher than consensus (+6.4% yoy vs +6.2% expected and core at +5.6% vs 5.5% expected). A bad confirmation of inflation stickier than most expected. Supply chain pressures (measured by NY FED Global supply chain pressure) decreased a lot, driving down the core goods inflation, but the core service inflation remain high. especially the shelter and housing related one. This part is, in fact, more related to job market, that continue to remain tight.

The “pendulum of the narrative” so rapidly shifted in less than one months from recession and high disinflation to strong growth and sticky inflation. This shifted also the central bankers attitude into more hawkish speeches with a return on the table of 50bp hike. Federal Reserve Bank of Cleveland President Loretta Mester said she had seen a “compelling economic case” for rolling out another 50 basis-point hike, and St. Louis President James Bullard said he would not rule out supporting a half-percentage-point increase at the March meeting.

MARKETS: The market impact of all these was dramatic, with a fast repricing up of the FED terminal rate (now seen at 5.3% in July, and higher than median FED DOTS for 2023 that is at 5.125%) and also for ECB (now seen at 3.60%).

Taking into account this, and the better surprise index momentum for US vs EU (below in green the difference between the two), helps to explain also the widening of intercontinental spread (10Y USA vs 10Y Germany) and the strong dollar (below in orange the Dollar index).

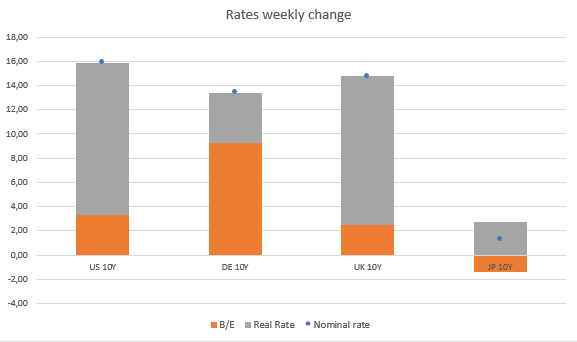

Remaining on rates we can see that the week increase is 15bp and 12bp (with treasury now at 3.84% and bund at 2.47%, with US at the top of the YTD range while Germany 10y not yet. But it’s interesting to look at the driver of the movement with a different allocation of real rate vs breakeven, with market give more credit to FED with a restrictive rates environment for longer.

Going now to credit/spread market below I use the european HY CDS (XOVER) and the classical BTP-Bund. Despite the rise of terminal rate (hawkishness of central bank), credit diverged from rates in the last 2/3 months and following more rates volatility with MOVE (a measure of rates volatility across the curve) remained muted YTD, despite a bit of pressure recently.

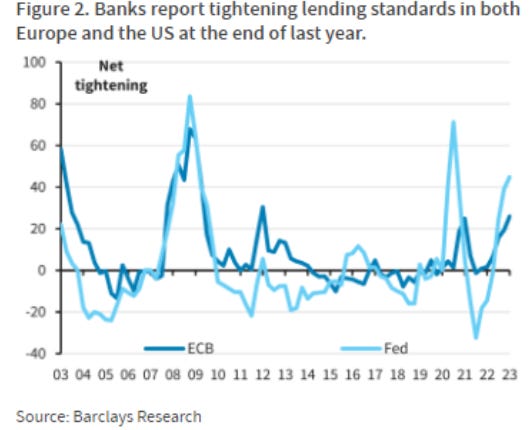

I like to use intermarket and internal drivers to gauge the potential direction of equity market too. Below a strong divergence between SXXP (in blue) and the credit market (here as a ratio between IG/Govt). European equity continued the uptrend, despite the higher terminal rate. Ok, equity could be more driven by the strong growth narrative at this point and less by rates, but credit is saying an other story. Credit (via the bank channel, where lending standards are now tight) drives growth and in the 90% of cases leads the equity market, so the probability trade-off is good to take a short position on it.

Finally some comments about commodities. The strong dollar, the rebound in inventories and the fear of less demand continued to impact energy assets while precious metals (Gold and Silver) were impacted by the higher terminal rate. Agriculture products remain supported by tensions in Ukraine, where fighting has intensified again.

MICRO:

On the micro/idiosyncratic camp, starting with underperformers:

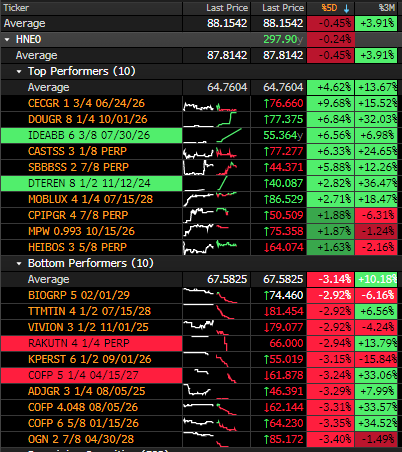

COFP (Casino): here nothing specif but just an adjustment after a strong past performance (looking at 3M returns);

OGN (Organon): bad reporting with revenue down 7% and EBITDA down 19%. Margin was squeezed by inventory write-down;

RAKUTN (Rakuten): perp down on downgrade fears after weak earning report due to slow improvement in mobile business.

The overpeformers were:

CECGR (Ceconomy): despite a weak/inline report with sales +3.1% and EBITDA -20% the bond and the equity performed well due to a Handelsblatt report affirming the company could become a takover target,

DOUGR (Douglas): up on strong sales growth in its 1Q results. Group sales growth were up 13.4% from October to December 2022.

It’s all for today. I hope you enjoyed my job/analysis. Feel free to forward it to friends/colleague and remember to subscribe to the newsletter.

great take, thank you!

Great summary of this weeks data!