Weekly Market Review - 17 Mar

Weekly Market Review - 17 Mar

A thread from macro to micro

Welcome back at the weekly recap, as usual at the end of the week. As always if you like my job/analysis please subscribe below and share it and I remember you that I am also on twitter at @Credit_Junk. And now let’s see what happened this week.

MACRO/NARRATIVE: Wanting to summarize everything that happened this week in a few themes, we come to 3 main themes:

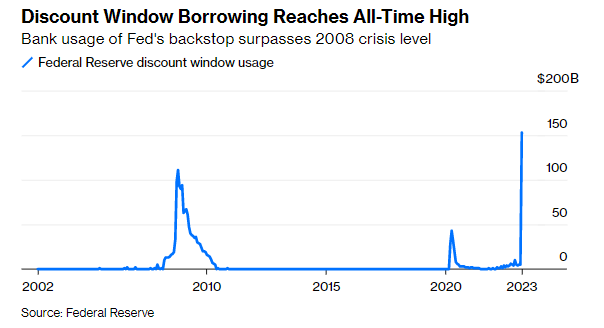

Financial stress in USA and EU banks: In the USA regulator acted between Sunday and Monday to resolve SVB to protect all depositors (after the failure of SVB and Signature Bank). FED approved a new bank term funding program with 1y loans without haircut and relaxed the usual discount window. At the end of the week banks borrowed a record 152$ bln from the various discount window (with only 11bln with the new program). Always remaining in the USA there was also a rescue package for First Republic with big banks which deposited 30bln in the bank. In Europe the focus is CS where the outflow of deposits continues to worry investors, despite the good capital level and the various liquidity ratio (as LCR). During the week SNB and FINMA (the swiss supervisory for financial market) committed to give CS enough liquidity if necessary, with the bank tapping 50bln and tendering short term debt to increase liquidity. For the moment these actions buy time, hoping that in the meantime the company could go ahead with their restructing process of the business.

I suggest you read this very complete article by John Authers who tells day after day what happened in the last two weeks.

USA Inflation: during the week we had the inflation data for February with headline up +0.4% MoM (expected at +0.4%) and +6% YoY (in line) while core rising +0.5% (stonger than expected at +0.4%) and +5.5% YoY. Services continue to remain high (especially driven by shelter and house rental prices that react with a lag) and persistent food inflation. What continue to worry is that sticky prices remains at elevated level.

ECB: has managed to keep the two aspects of inflation (and monetary policy) and financial stability separated. In fact looking at the higher than expected (and persistent) inflation decided to hike rates by 50bp. During the meeting they presented their economic forecast with lower headline inflation (due to falling energy prices) but high core in 2023 (but lower in 2024). The increasing wages offset the good effect of energy, but at the same time support consumers spending. The dovish element was that we have no more a forward guidance (no pre-committed hikes) but decisions will be only data dependent. On financial stability ECB said that they are well equipped, if needed, to provide liquidity to the system and that the “banking sector is resilient, with strong capital and liquidity positions”.

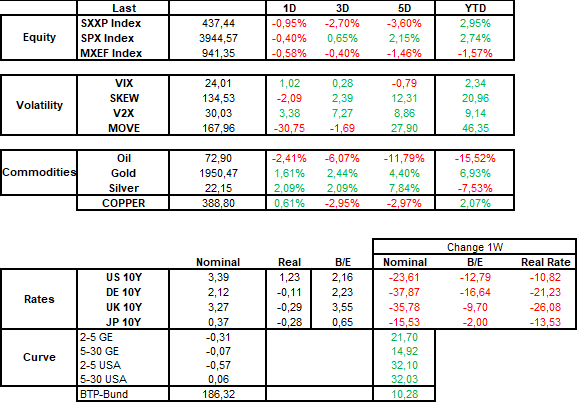

MARKETS: Below the market dashboard for the week.

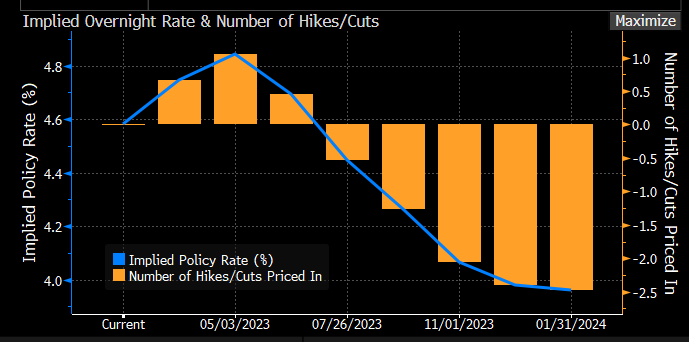

The reaction on the rates market was a fall of interest rates (US 10Y is now at 3.38% from a 4% of some weeks ago) while the 10Y Bund is slightly above the 2%). The movement was driven by a contraction of breakeven (following also the fall of oil and copper) but also of real rate, with STIR trader removing hikes from the OIS curves (market price only other 15bp of hikes for ECB and 70bp of cuts for FED within the end of the year). In the second chart the WIRP Bloomberg function for USA.

Curve steepened across the various tenor with market betting on the end of hiking cycle and, in same cases, the start of the cutting cycle. It’s not the flattening and inversion of the curve that indicates recession is near, but the steepening of it.

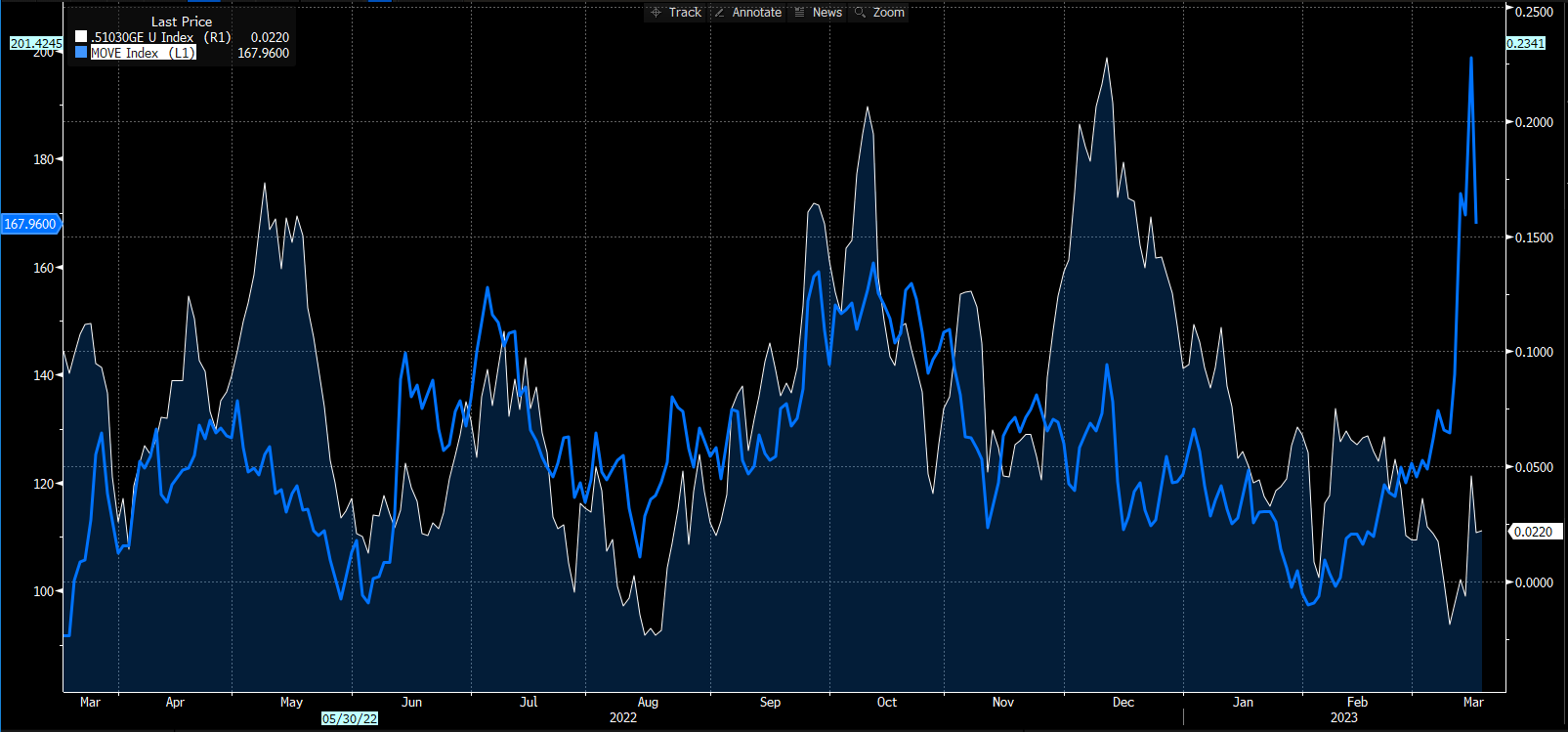

The European credit market suffered from increased volatility (both interest rate and equity - MOVE and VIX/V2X) with HY widening 70bp and IG widening 14bp in cash, while the movement was high looking at CDS and ETF spread based.

Remaining on risky assets, equity in US remained more stable this week, thanks to the stronger action of US regulators (as explained above) regarding liquidity. Europe financial tensions are more there despite some action by Swiss National Bank so SXXP close the week with a -4%.

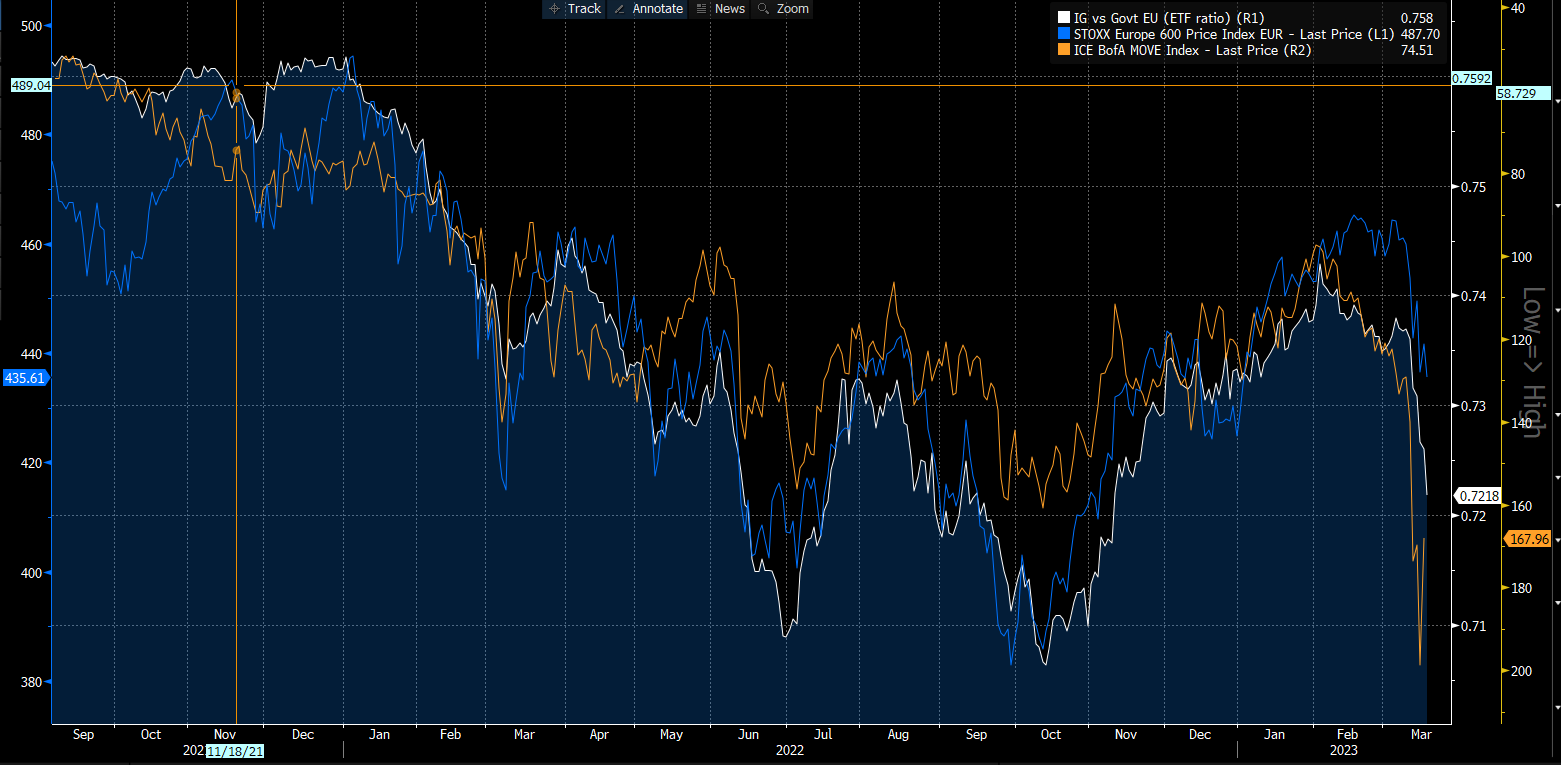

Using an intermarket approach. credit market predicted well the move down in the equity market (I love to say “Give credit to Credit”) with spread always leading the equity market. Credit (via the lending channel) is a leading proxy for growth, so we need to continue to monitor the bank lending survey and the various financial condtions.

Below I added this time the MOVE (rates volatility), obviously inverted, that usually moves together with credit market. This week rates volatility was driven up by the ECB action too, with ECB removing any forwarda guidance and passing to a data-driven approach.

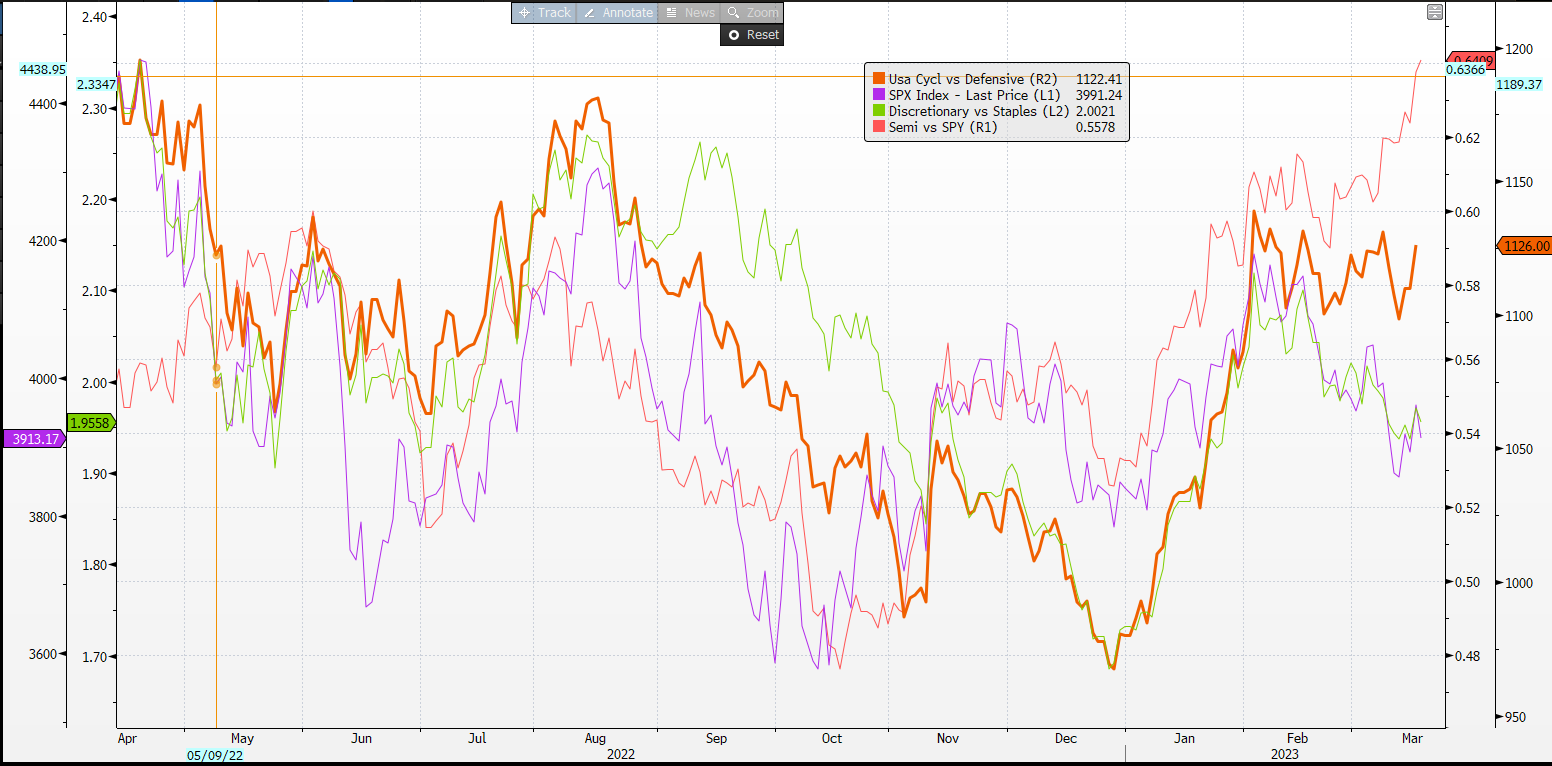

In the US the internal forces are mixed with Cyclicals vs Defensive returning up and a very strong Semiconductor sector, while discretionary remaind weak vs Staples.

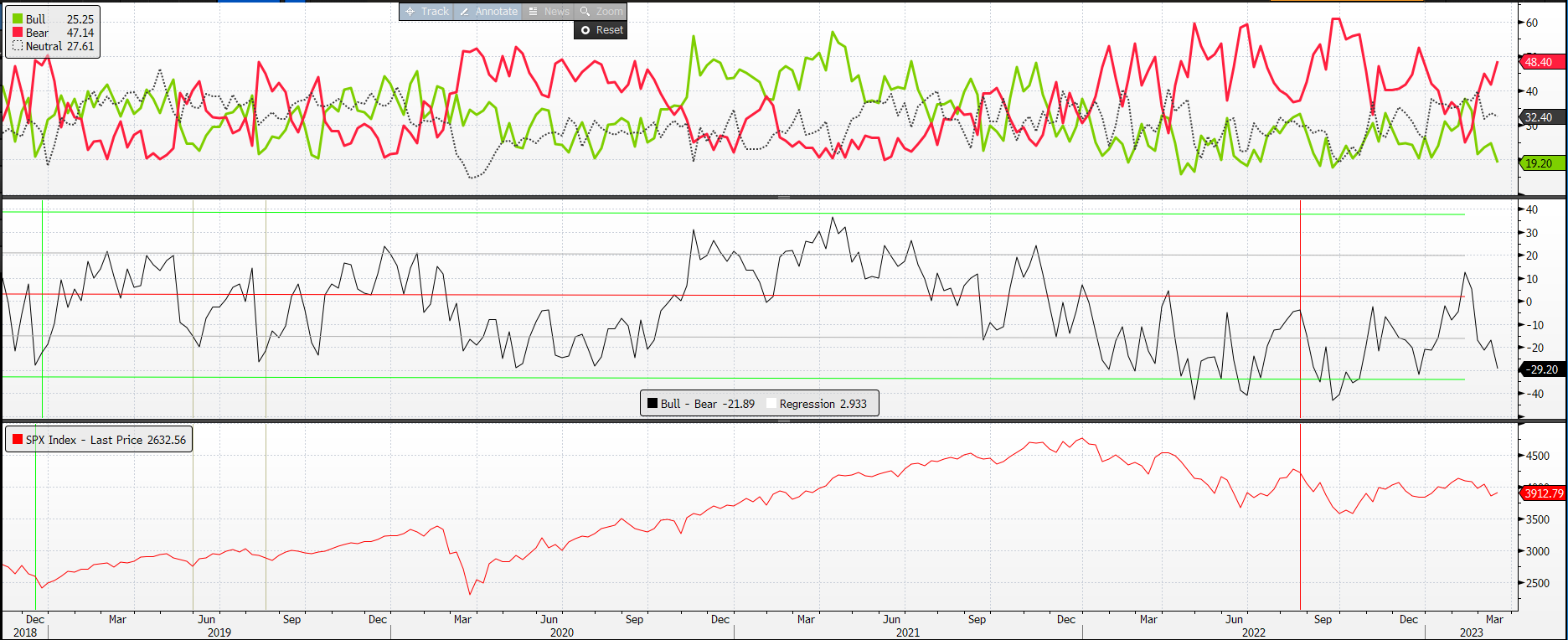

After this week (that we will remember for a long period of time) the bears are now well above the bulls, with the delta between the two now on a level that in the past indicated some possible rebound.

I want to conclude this macro part talking about commodities, and especially of gold. Contrary to the common narrative, gold has held up well to rising real rates, and now with the peak in dollar exceptionalism behind us it returned a good proxy for risk safe asset (together to JPY and CHF). With some positive fundamentals (like central banks buying as there is no tomorrow), the risk-aversion of the week drove the price above the high of the year.

MICRO:

We passed the reporting season. The winners of the week (in the EU) HY Index are almost all long-tenor, BB bonds as Inwit, Cellenx and TVOYFH (without a specific news).

COFP (Casino) was the worst performer of the week due to the weak profitability and the news of last week of “insider trading claims”. Today the company announced the sale of asset in Brazil for 780M.

TRADE of THE WEEK (Bonus): Below I want to introduce some trade idea I started. Below the Eur 5/10/30 fly. This fly is driven by the rates volatility (MOVE) and show that the 10y (the body) is rich vs the wings. I usually do this trade in a simple version with 50%/100/50% risk. If the volatility persist the body should underperform.

It’s all for today. I hope you enjoyed my job/analysis. Feel free to forward it to friends/colleague and remember to subscribe to the newsletter.