Weekly Market Review - 24 Feb

Weekly Market Review - 24 Feb

A thread from macro to micro

Welcome back at the weekly recap, as usual at the end of the week. As always if you like my job/analysis please subscribe below and share it and I remember you that I am also on twitter at @Credit_Junk. And now let’s see what happened this week.

MACRO/NARRATIVE:

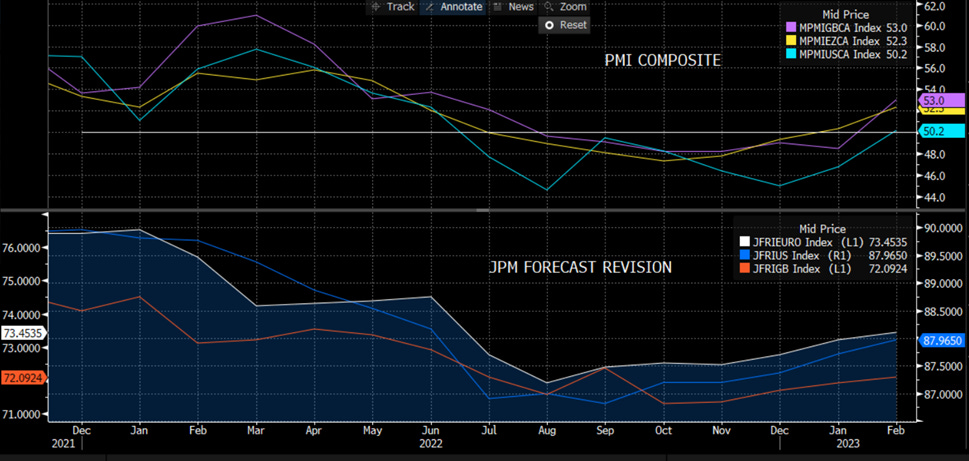

This week macro data reinforce the narrative of stronger than expected economy with the February composite PMI (flash version) for Eurozone, UK and US all back above the 50 theshold (the watershed between recovery and contraction) simultaneously. For all economises the rebound was driven by services sector, but there was also a return to growth for manufacturing sector. The fall in input cost and the sharp reduction of supply chain problems helped particularly the manufacturing sectors. The pressures on wages remain.

This improved growth is also behind the stickness of inflation, with core inflation in Eurozone revised up from 5.2% to 5.3% still to not confortable level, supporting the return of hawkish members of ECB reinforcing the need to more hikes beyond March.

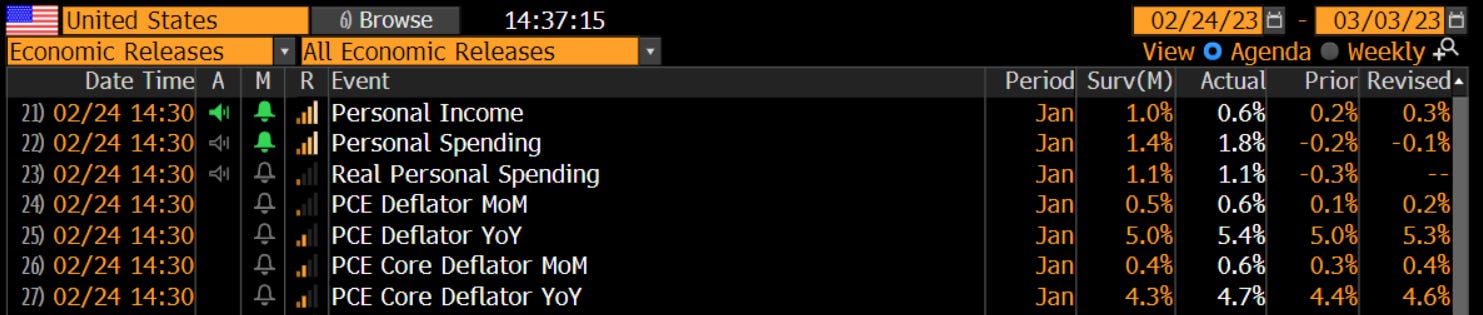

Also the PCE, the FED favorite inflation indicator surprised on the upside today, on both the headline and core measures. Consumer spending increased too, these together put pressure on FED to continue to hike, with a return of 50bp again as a possibility.

So the narrative is one of better growth and inflation more persistent and higher than what central banks want, forcing them to tight more (higher terminal rate) and to mantain it for a long period of time. Basically what is called “NO LAND NOW, HARD LANDING LATER”, with the impact of higher rates that in H2 of this year, or in 2024 will have their impact on the economy.

MARKETS:

The market reaction was rational with a inflation breakeven (below the 5y5y) for Eurozone grown by 25/50bp in one months. The market (knowing the reaction function of Central Banks) added hikes on the curve (below, in white, the difference between the 1th and the 5th Euribor contracts, Mar 23 vs Mar 24).

This is visibile also looking at terminal rates priced by the OIS curve for EUR and USD. In the panel above the July FED fund is priced at 5.38% (almost near the 5.5% vs the 5.1% estimated in December by the FED), while in the panel below the ECB deposit rate for September priced at 3.67% (almost 3.75%).

With higher terminal rate we had also a return of rates volatility (below in doorstep with dollar index) with 10Y treasury returning at 3.90% and bund 10y at 2.5%, reversing almost all positive YTD performance.

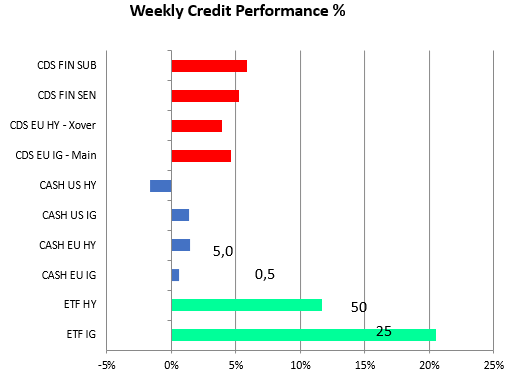

Credit was impacted too with ITRAX Main and XOVER (IG and HY) widening 5bp and 26bp. Cash index are quite on the paper, but the implied ETF spread suggest widening of 25bp and 50bp for IG and HY respectively.

Higher rates and widening credit, despite tight from an historical point of view (above the normalized spread, basically a Z-score), is equal to reducing liquidity environment and tighter financial conditions. Last week I suggested to look at credit for market direction, with my now famous sentence “Give credit to credit”, and I noted this bad divergence, affirming that in 90% of times credit leads equity market. The IG/Govt ratio (IBCX/IBCN) is a total return ratio. Now I updated and some correction happened but the gap is wide yet.

European credit market outperfomed SPX for different reason: better surprise index, more tilt to banks (that benefit of higher interest rate, or more from a steep curve) and from cheaper valuation after a 2022 driven by FED exceptionalism.

Now, after some weeks with equity not looking at terminal rates, now it seems they noticed, especially in the USA. An other global headwind is the fall in liquidity, especially driven by the strong dollar (below three metodh to calculate liquidity:

FED formula = Assets - RRP - TGA

Global M2 (converted in dollar) in white

CB assets (converted in dollar) in blue

To sum-up the risks for risky assets are due to higher rates for a long period of time (with impact of the first hikes yet to see), a weakening liquidity environment and a still weak manufacturing sector (with high level of inventories). Florian wrote a great article on yet. Read it!

MICRO: From a single name point of view:

HRGNO(Hurtigruten): secures refinancing and additional shareholder funding of EUR 80m ahead of reporting expected 1 March 23. The bond rebounded 4.5% this week;

TEVA: The U.S. Food and Drug Administration has approved Austedo XR, to Treat Tardive Dyskinesia. Posite reaction of the bonds

KPERST (Klockner Pentaplast), SDSELE (Signa), METAL (Metalcorp) dropped 5% without a specific reason if not illiquidity and distressed level.

It’s all for today. I hope you enjoyed my job/analysis. Feel free to forward it to friends/colleague and remember to subscribe to the newsletter.

Really enjoy these. Great work.

Great quote!