Weekly Market Review - 31 Mar

Weekly Market Review - 31 Mar

Welcome back at the weekly recap, as usual at the end of the week. As always if you like my job/analysis please subscribe below and share it and I remember you that I am also on twitter at @Credit_Junk. And now let’s see what happened this week.

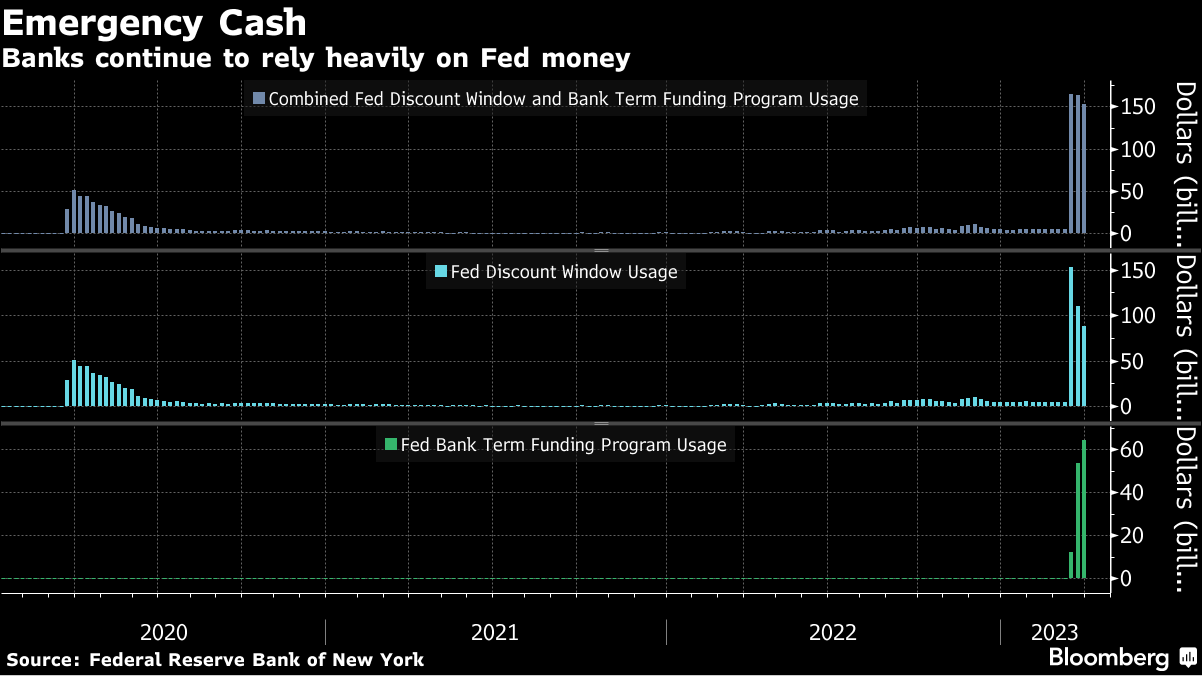

MACRO/NARRATIVE: This week was quite regarding news on financial stress (panic?) both in US and in EU and this is clarly the classical case for “No news, good news”. As showed in the following chart of Bloomberg the total borrowing from FED decreased to $152.6 bln this week. Looking more at details there was a decrease from $110 bln to $88,2 bln on the traditional “Discount window”, while there was an increase from $53.7 to $64.4 bln on the new BTFP program (with credit that can be extended for one year).

This allowed the sentiment to remain positive (and quite), with also the MOVE (the volatility of interest rates) to join the party of low volatilty in equity (Vix, VVIX, Vix curve, and TDEX).

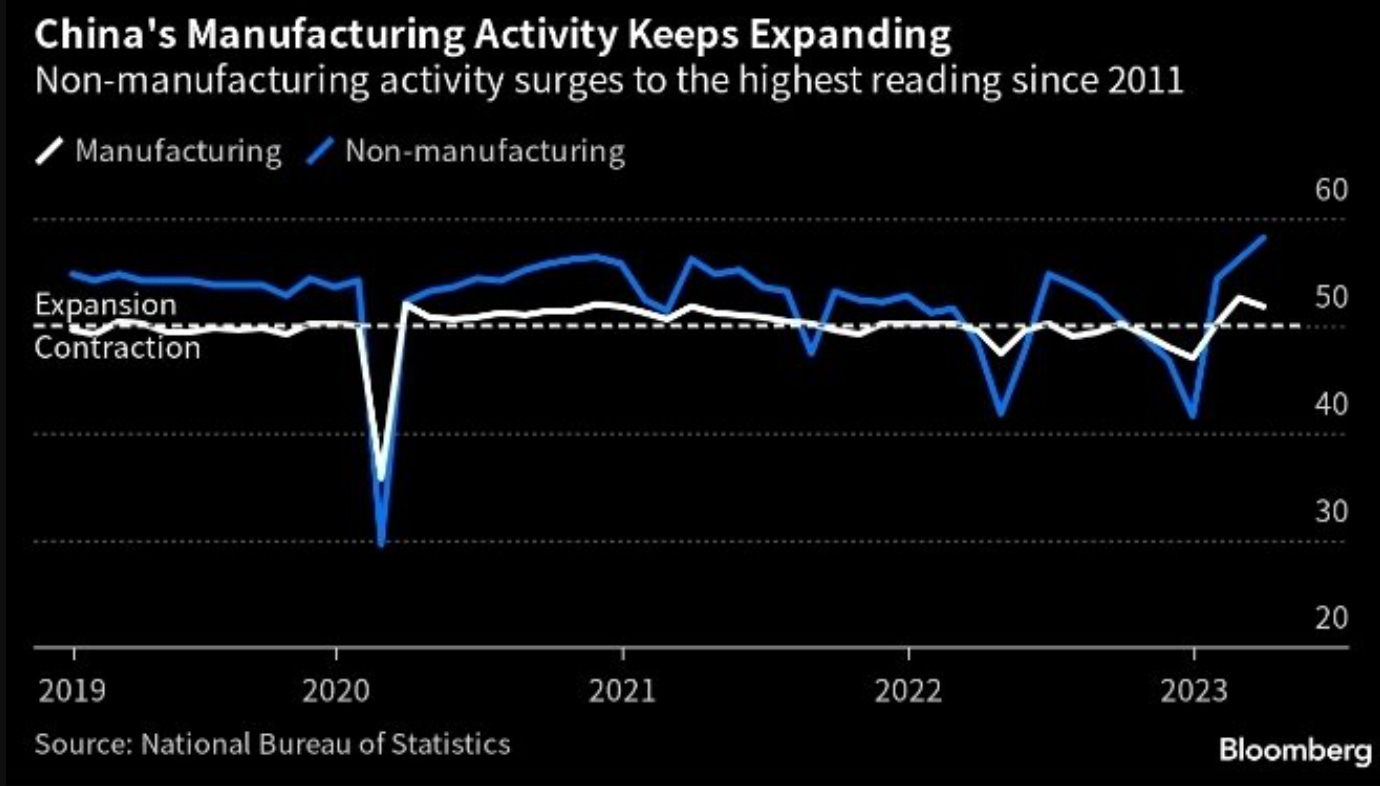

With banking concerns easing we were able to return to the usual business of fundamental data. Regarding growth we had the important data of PMI in China for March with manufacturing softening from 52.6 to 51.9 (above the theshold between contraction and expansion and better than expected), but the great surprise was on services increasing from 56.3 to 58.2 (expected at 55) confirming the good momentum after reopening with consumptions and investments well supported.

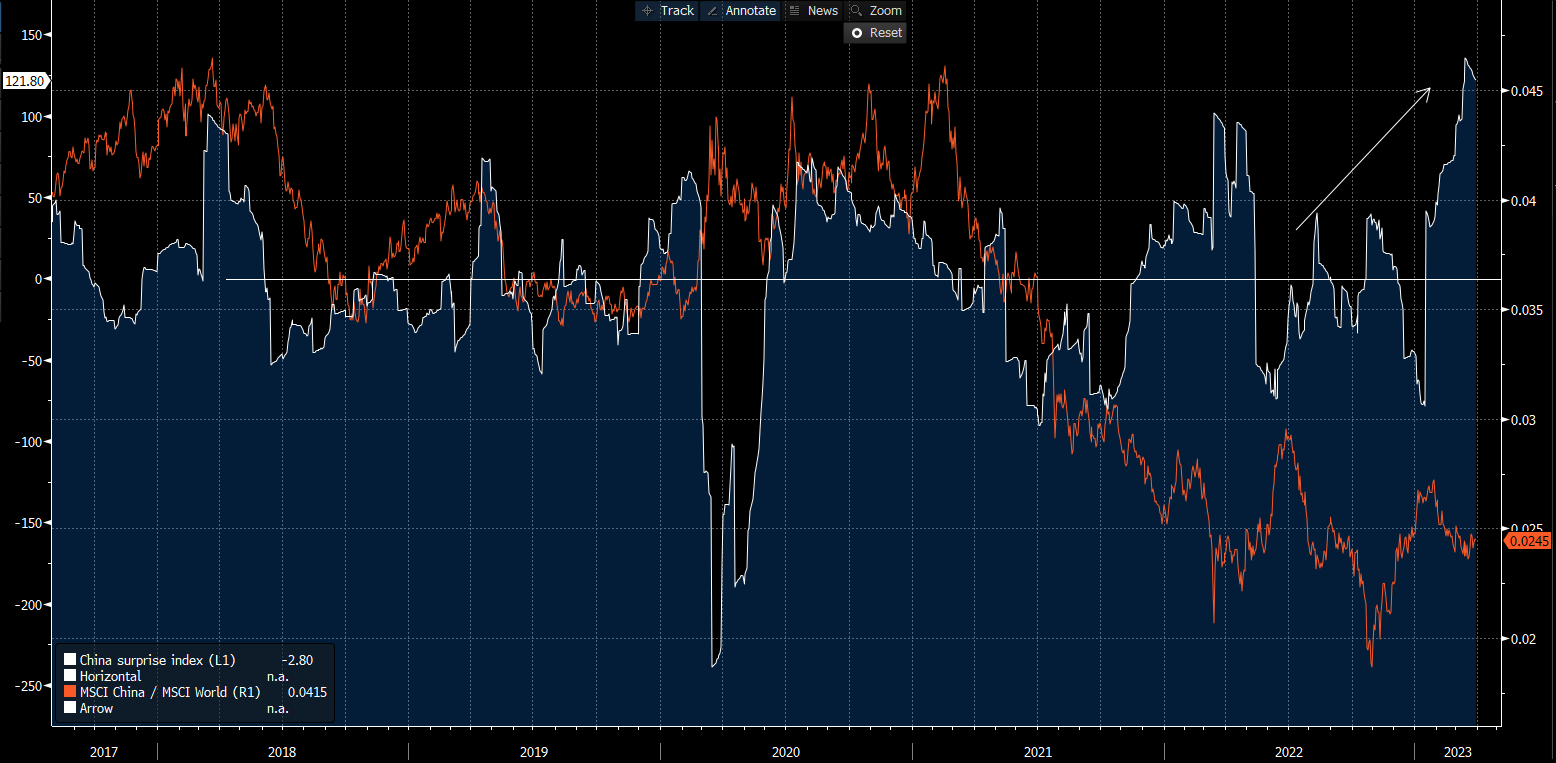

The good momentum on growth is confirmed also by the positive surprise index, now positive but not yet by the relative betweend MSCI China and the world.

Regarding inflation, today CPI for Eurozone headline fell from 8.5% to 6.9% (lower than expected) with an increase of 0.9% MoM but core inflation rose from 5.6% to 5.6% of February. Looking at the details, the energy component passed from 13.7% to -0.9%, with the energy base effect explaining all the headline fall. But food continued to increase, despite a fall of agriculture commodities and services trend continue to remain up. With wages in eurozone tilted to the upside this component will continue to put pressure on the inflation indicator in the euro area, and on the ECB.

Always for inflation indicator in the US we had the PCE deflator falling from 5.4% to 5% and the Core (the Fed's preferred measure of inflation) decreasing from 4.7% to 4.6% (both slightly below estimates). The momentum (using a 3M annualized change) is now positive again and also annualizing the MoM data, this remains well above the FED target (0.3% * 12 = 3.60%).

MARKETS:

BONDS: positive sentiment, reduced volatility, better growth data and sticky inflation allowed market to put more hikes on the short-term curve, despite well below the past peak. 10Y USA and GER increased 15bp and 20bp respectively driven both by higher real rates and also higher breakeven (only for euro area).

The correlation between stocks (risky assets) and bond (below TY1 - treasury futures) flipped to negative in March (the old “new normal” of the deflationionary period started after 1998). Curve returned to flat (with more hikes again in the front-end) while spreads (govies and corporates) are well supported by the fall of the MOVE (rates volatility).

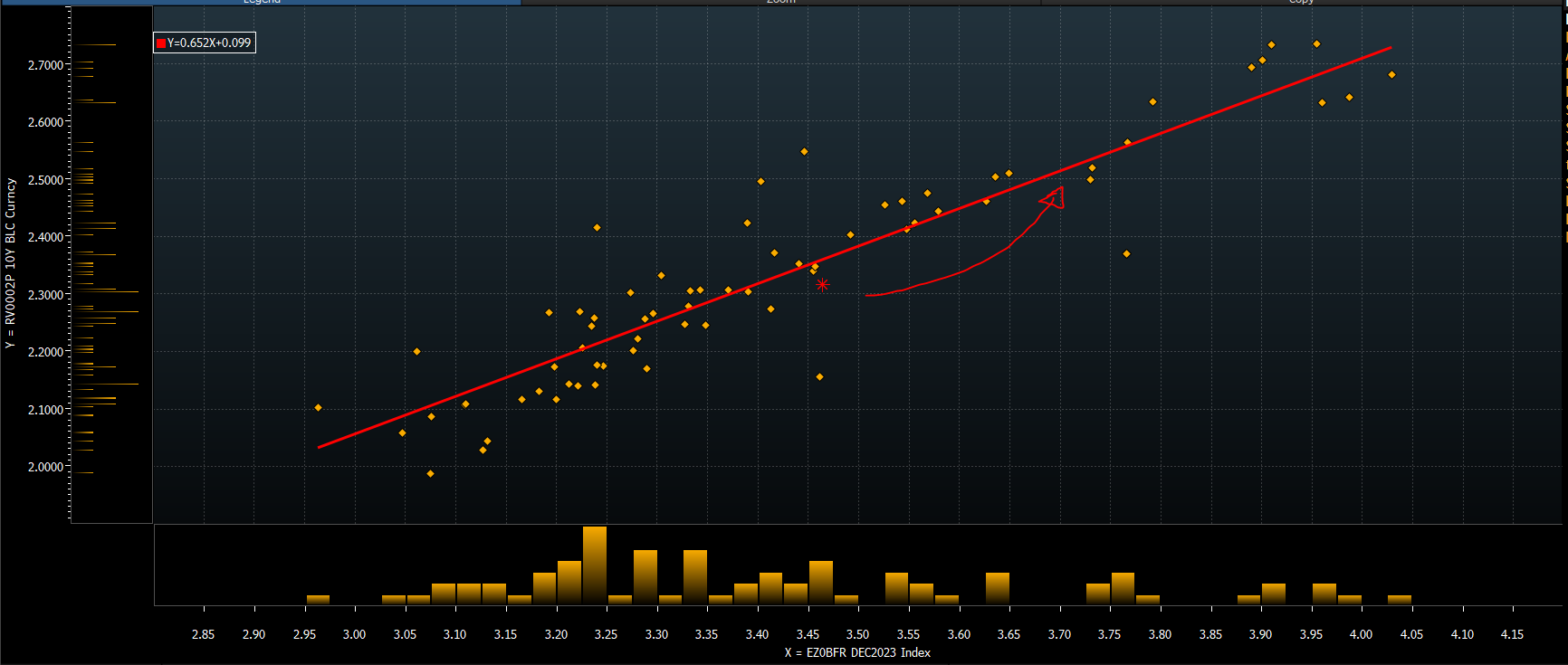

Given the stickness of inflation (especially in the euro area) and the quite newsflow from banking sectors, relaxing financial conditions, ECB could continue to hike. Market now prices “only” others 50bp more but if an other one is added (other 25bp) the bund fair value is near 2.5%. I consider it a good level to add duration again.

CREDIT: the spread component performed well, as all other risky assets. Both the Citi Macro Risk sentiment and the Citi S/t macro risk sentiment returned to a zone of risk aversion below average (risk appetite above neutral).

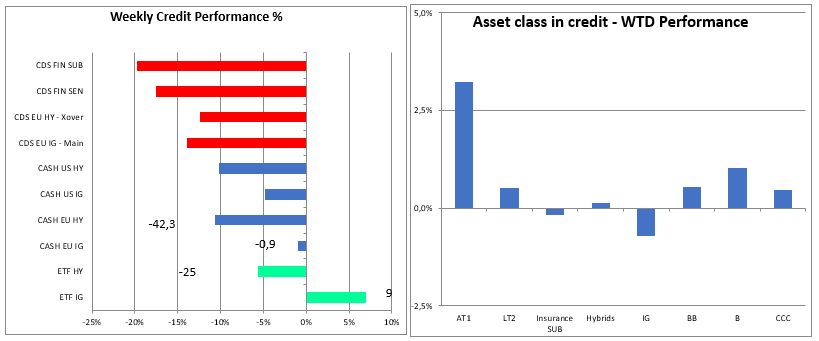

HY cash spread tightened 42bp, the implied spread of the HY ETF tightened 25bp, while XOVER CDS outperformed tightening 50bp. IG cash spread was almost flat, while ETF i-spread (implied spread) widended being more a duration proxy. Regarding total return the AT1 is the most positive asset class.

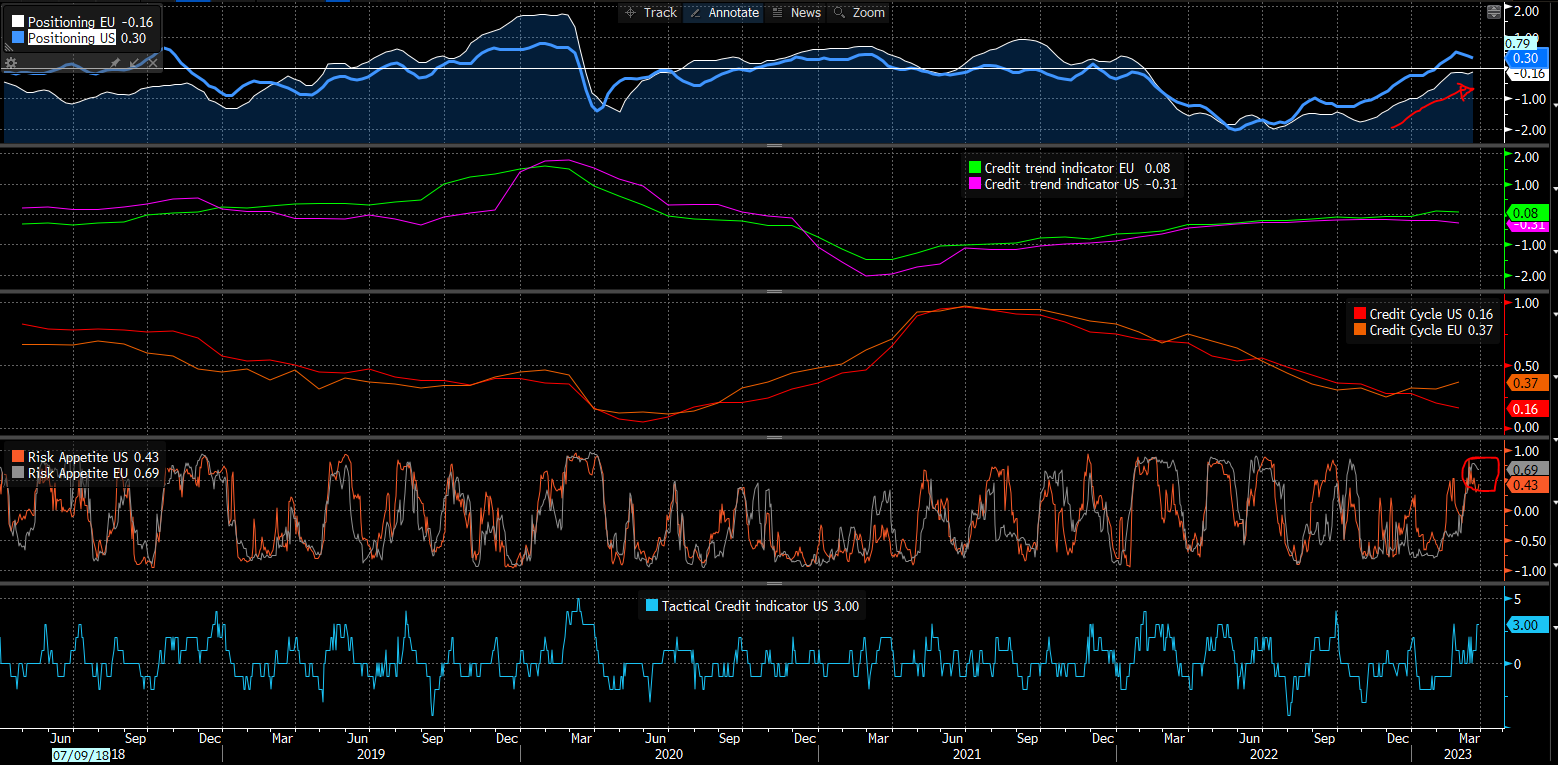

Looking at some credit specific sentiment/positioning indicators below some BNP index. Positioning is now neutral and slightly positive for US, while risk appetite is at high level.

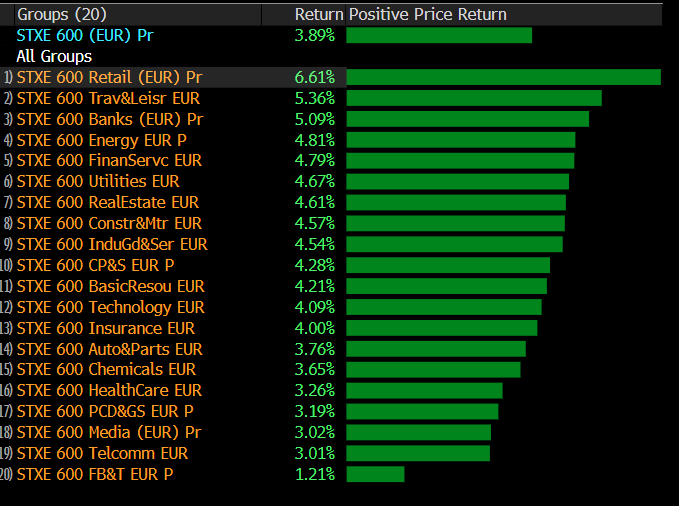

EQUITY: Equity performance is positive this week, with SXXP up 3.89% and SPX 2.59%. The sectors with the best performance are the most cyclical (below data for EU but it’s similar for US if not for technological, more important there) and the banks (rebouncing after weeks of weakness).

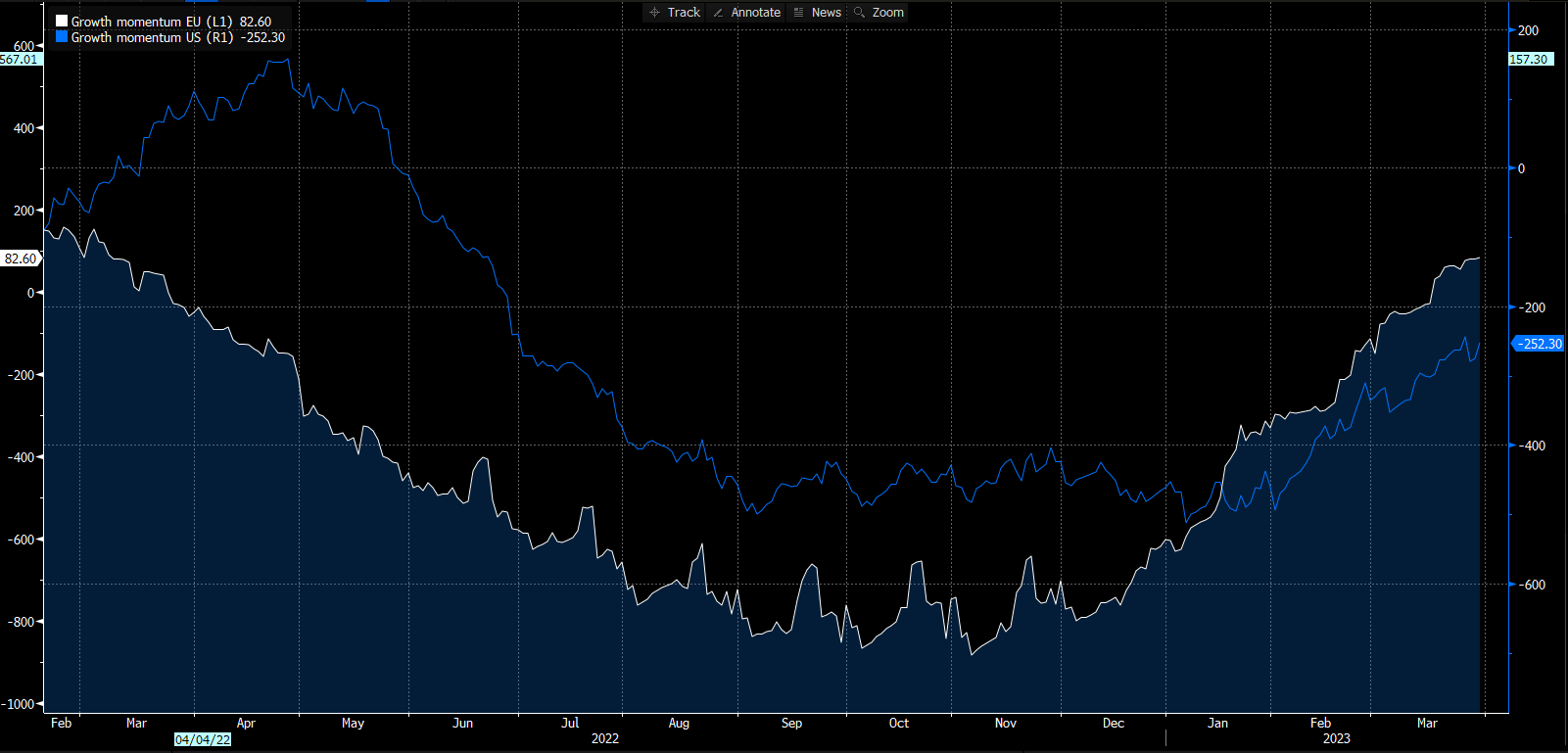

The fundamentals, at the margin, have better momentum (below the chart for US and EU) but also technicals are improving and supportive for the moment. Let’s look at some of these.

The intermaket information from the credit market confirm the support for the bullish momentum in equity. Below the IG/Govt ratio for EU bonds and HY/IG ratio (here the market now thinks that growth will be better than just some weeks ago) are in line with the rebound in SXXP. The pendulum between inflation and growth continue to move from one side to the other.

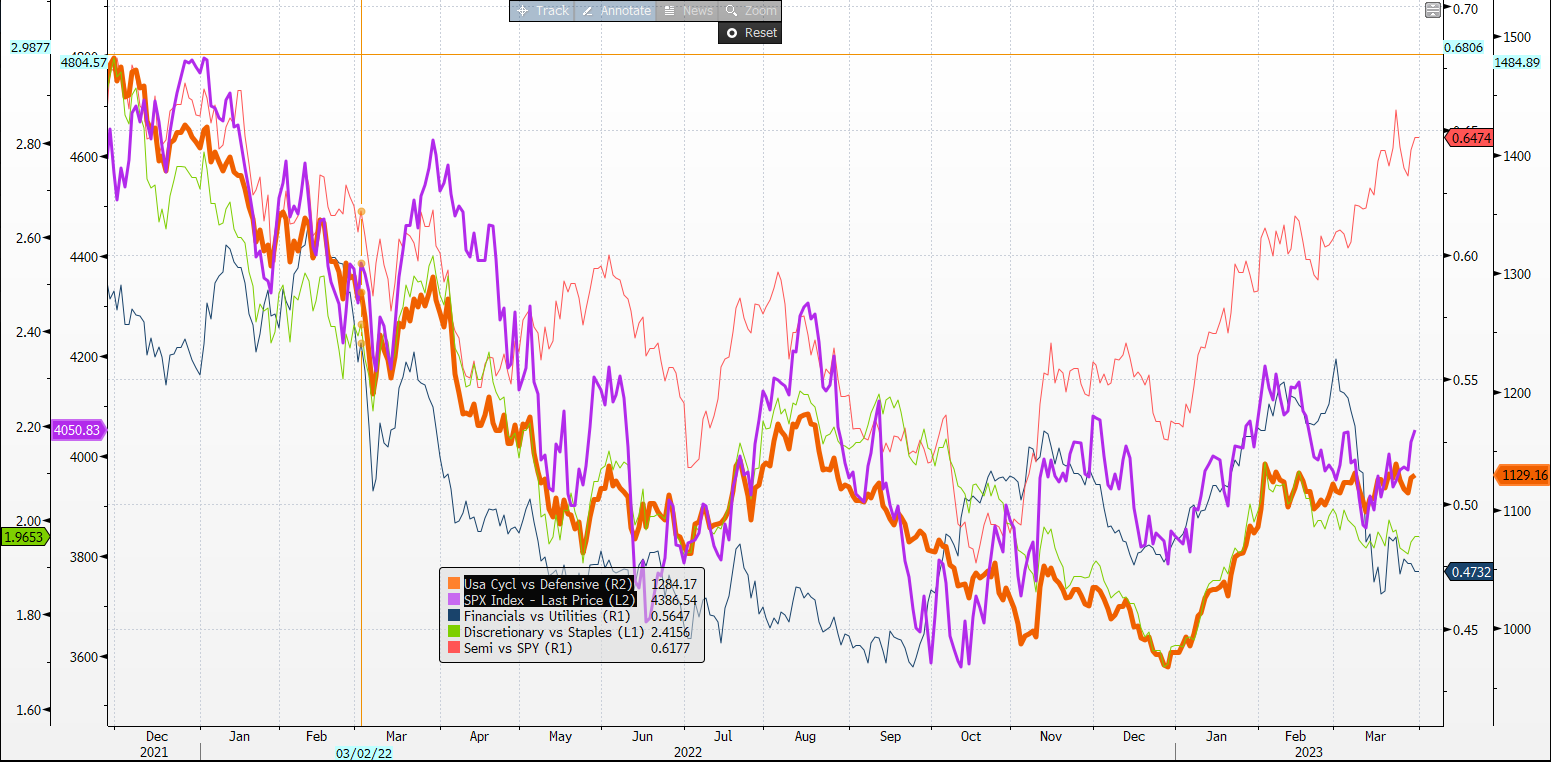

Passing now to the USA, the internal of the market information it’s anything but negative. All the cyclical/defensive, discretionary/staples are positive/neutral while financial/utilities is now more stable (confirming for now “only a liquidity event” of some specific bank subsectors”).

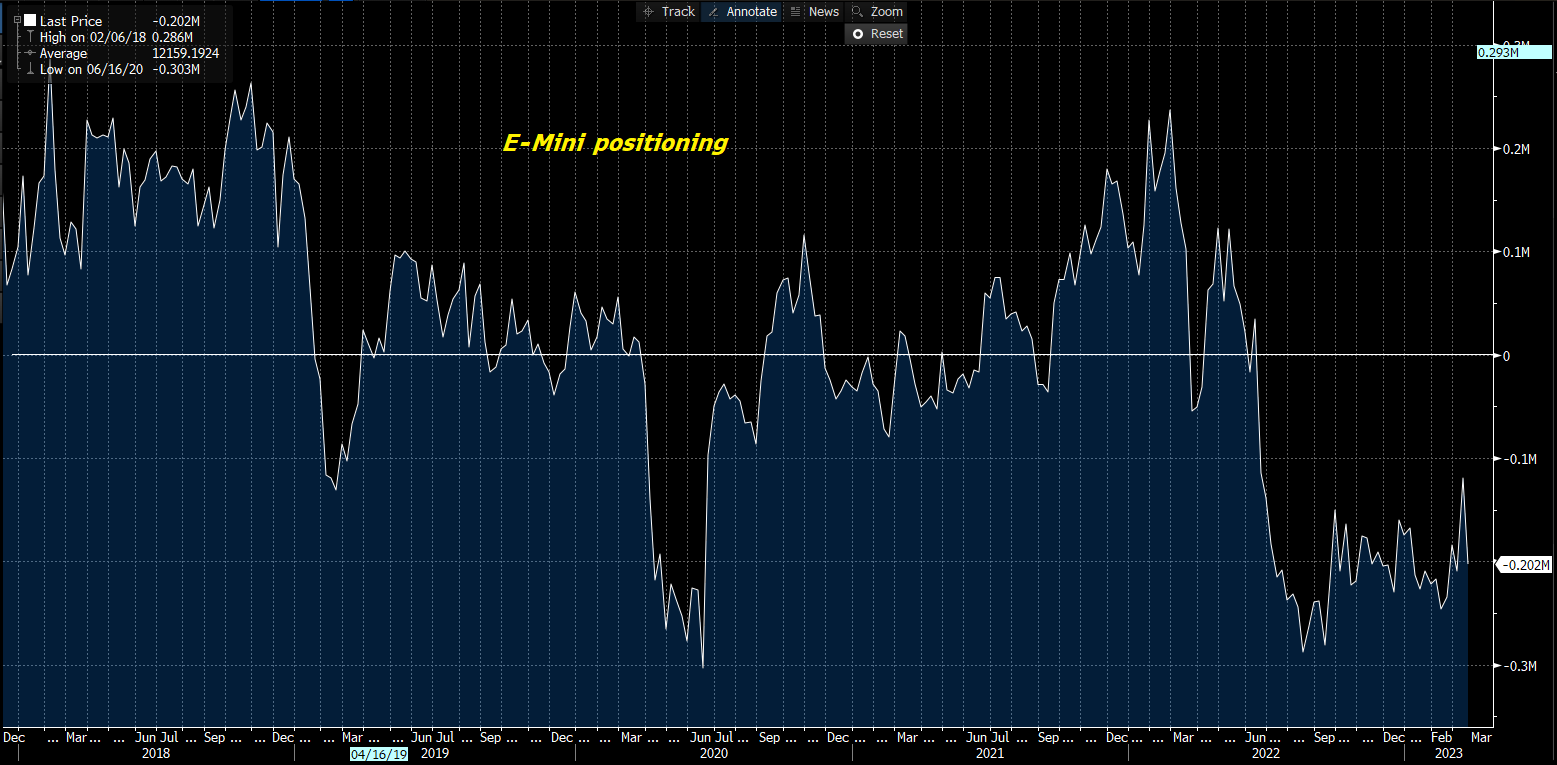

Sentiments/Positioning indicators are supportive too. Below the AAII Bull-Bear indicator is between the -1/-2 s.d. with a high level of bears while positining on future remain below average.

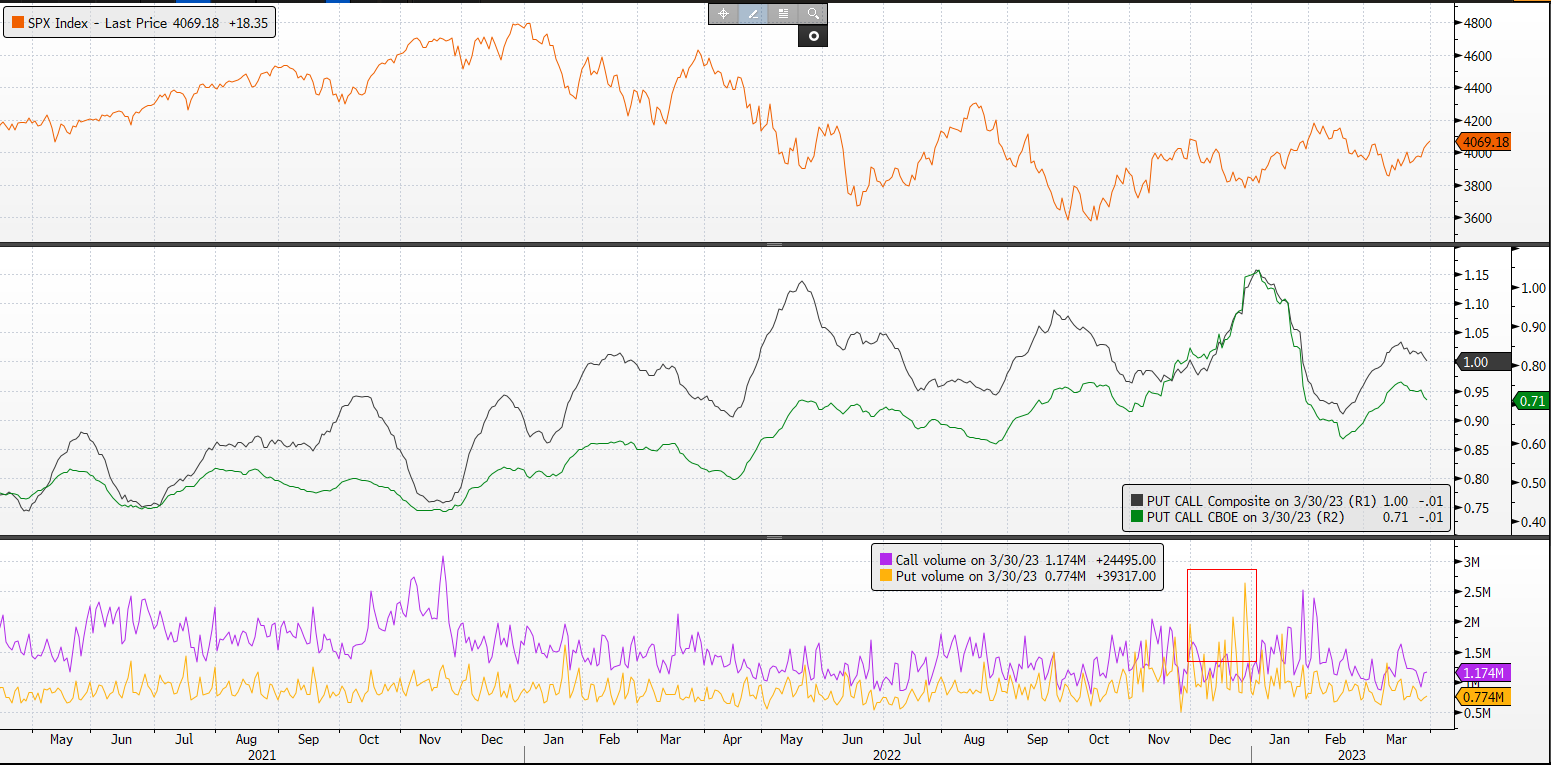

Some excess of confidence could be read looking at skew, with 3M normalized skew now around 0, with now less people hedging from downside. The put/call ratio is declining and the call volume remains above that one of put.

COMMODITIES: Just some words regarding commodities, and especially the oil. After some pressure and some liquidation on futures market, some positive news on growth and positive sentiment gave oil a good return this week (+9% for WTI and +6.5% for Brent). Inventories data remained low, but in line with seasonality, for crude while tight for gasoline and diesel. Some negative news come for supply with 400k bpd of Iraq oil exports are now stopped for a legal claim between Kurdistan and Iraq.

MICRO: Some newflow regarding single name during this week:

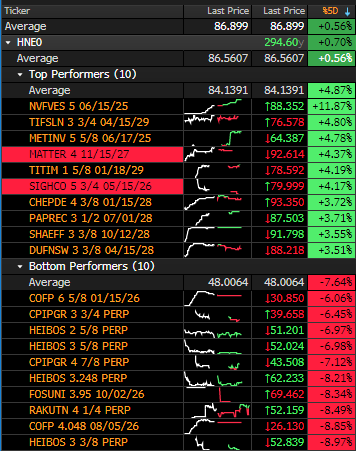

NVFVES (Novafives, Caa1/B-): company reported a good set of results for Q4 2022 above market expectations. Company confirmed 2023 guidance too. FY 2022 revenue growth rose 18% while EBITDA by 20%, with margin increasing from 6% to 6.2%. FCF remained positive and almost double vs 2021, with a strong deleveraging (from 6.8x to 4.9x). Bond positive performance.

SIGHCO (Sigma Holdco, Caa2/CCC): good report by the company, with improved FCF generation and deleverage. Bonds up 3/4 pts.

SHAEFF (Schaeffler, Baa3/BB+): the company was upgrade to IG by Moody’s this week due to solid operating performance.

NFLX (Netflix, Baa3/BBB): Upgrade to IG by Moody’s, now in line with S&P. Now the bonds could pass in some IG benchark.

COFP (Casino, Caa2/CCC+): the bond continued to underperform after last week downgrade and QUATRIM tender offer, despite the company announcing success of the operations.

For today it’s all. If you liked reading it and want to support my job, please share this piece to friends and colleague and subscribe to the newsletter using the link below.

Have a great weekend,

Credit_Junk

Love these weekly summaries. Thanks!

Your blogs are more and more comprehensive and better from month to month. Keep it up