Weekly Market Review - Dec 02

Weekly Market Review - Dec 02

A thread from macro to micro

Welcome back at the weekly recap, as usual at the end of the week. As always if you like my job/analysis please subscribe below and share it and I remember you that I am also on twitter at @Credit_Junk. And now let’s see what happened this week.

MACRO/NARRATIVE: wanting to sum up the week in a few words these would be:

China: the week started with an other wave of covid cases and socialt unrests in different part of the county with new lockdown across different cities. The unrests (all political regime are afraid of losing consensus) together to the fact that a lot of local authority have no more money to test all people and from China started to come a 180° turnaround on 0-covid policy. Maybe they realized that with omicron the strategy is not achievable but some cities started to remove lockdown, the national security system boosted vaccination for older peoples and it was introduce a quarantine period at home. These confirm my view that the country could reopen in the first half of 2023 thanks also to the launch of their Mrna vaccine (now in phase 3) using this as a propaganda tool. —> reopening narrative

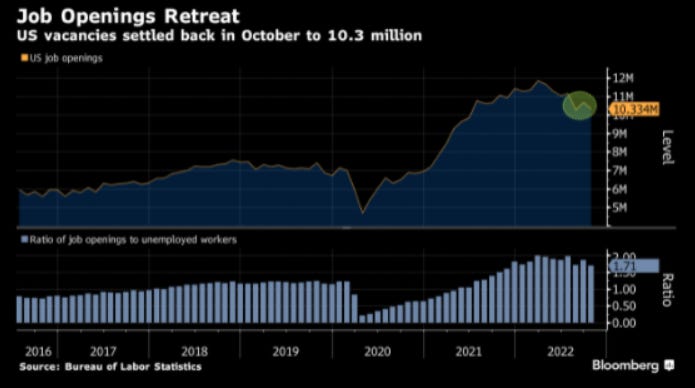

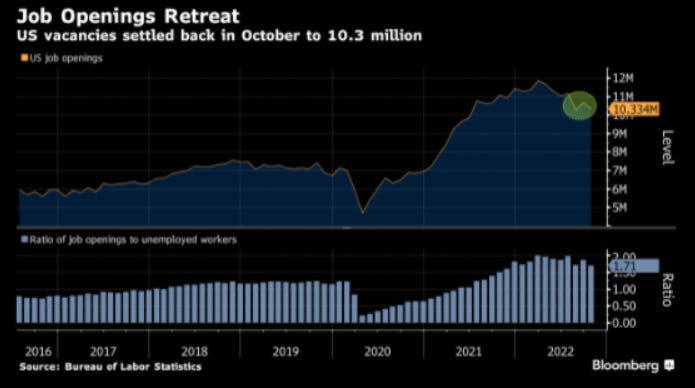

FED/POWELL: Different speakers (Bullard) continued to sustain that FED will need to do more than less and Thursday on a speech Powell confirmed that there is more jobs to do (with terminal rate higher then initially forecasted) while at the same time considering lag and cumulative tightening some reduction on the rhythm of hike is considered (passing so from 75 to 25bp). The macro data published for the week was weak, looking at forward looking indicators (*US NOVEMBER ISM MANUFACTURING INDEX FALLS TO 49; EST. 49.7) and confirmed a weakening in the macro momentum while JOLT showed a job market still tight with job opening reducing and opening/unemployed falling to 1.7x (still far from pre-covid level).

This tightness is confirmed also from the today payoll (+263K new jobs, unemployment down from 6.8% to 6.7% and hourly average earning +0.6% vs expectation of +0.3%). After the data FED terminal rate (priced in the OIS swap) returned up to 4.95%.

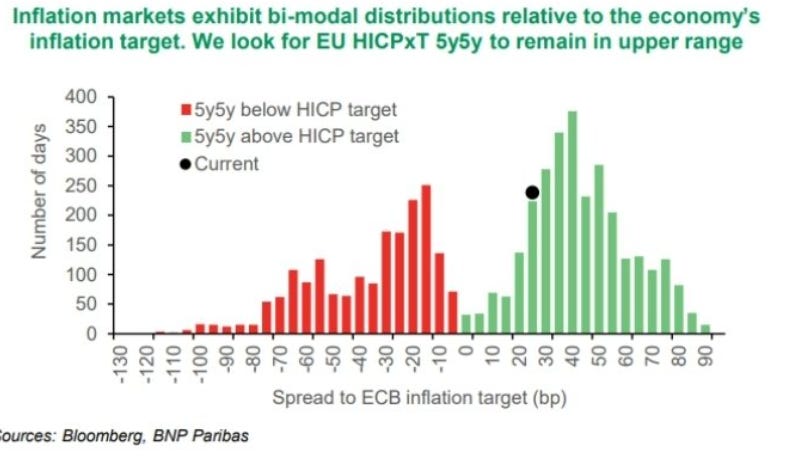

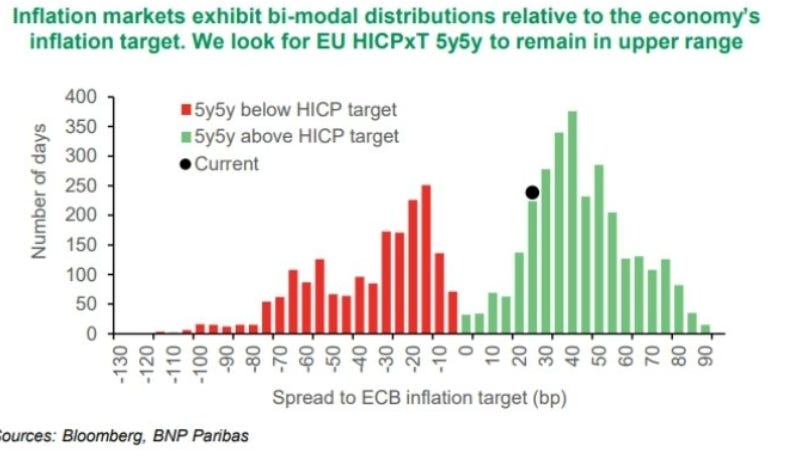

INFLATION PEAK, INFLATION PEAK?: CPI estimates for November slowed down from 10.6% to 10% (expected 10.4%), while the core (ex food/energy) remained stable at 5%. The country breakdown showed a strong fall in the energy component in Germany and while this is for sure a good thing (together to the peak recached in US CPI produced a “Inflation past peak narrative”) I think core inflation will remain high for months. What will be more important is how fast and what will be the final inflation level. How you can see from a research of BNP, market can think only in white or black so the below bi-modal distribution of inflation. Now market price an inflation returing near target at the end of 2023.

Given this above I returned to buy inflation protection, buy it when you don’t need it and when others don’t want it.

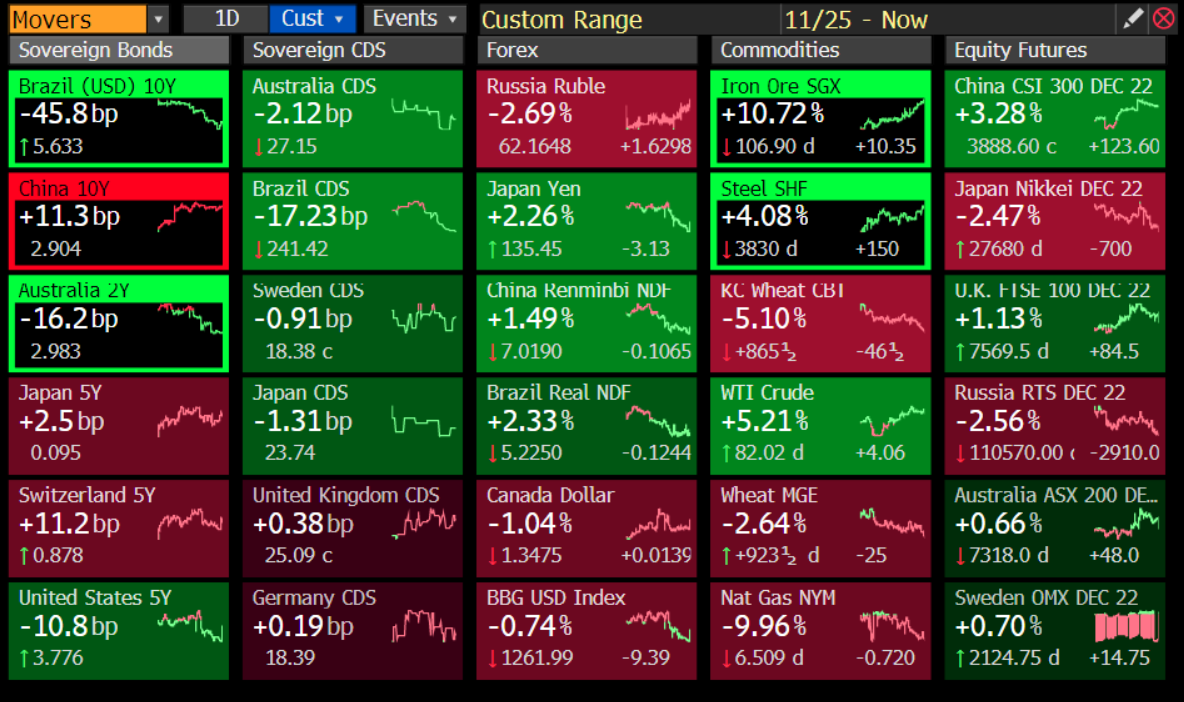

MARKETS: To have a better idea of global macro moves across market I like to look at this function on Bloomberg (GMM - global macro moves). You can see the big move across various asset class.

Given the newsflow/narrative above clearly on the “equity” market the winner is China, with a wave of momentum/trend buyers, while due to the rebound in JPY (will return later on this) Nikkei falled -2.47%.

Remaining on the “China reopening trade” the industrial metal commodities complex rebounded strongly (Iron Ore +10%, Steel +4%) together with oil (+5.2%) with hopes of a return of demand.

On DM equity market below I look at sentiment/positioning indicators. The AAII Bull-Bear index short a return near a neutral level, bouncing from the high pessimism level of end september (in the chart the SPX at the bottom).

Passing now on the “internal forces” inside the market aka called “breadht” the cyclical vs defensive (but also other similar indicators like staples/discretionary, etc) showed a divergence versus the general market direction.

Finishing on the technical picture for SPX index we can see that index arrived at 200 day moving average but with a weakening in the momentum (below I use MACD). Going forward we need a change in fundamentals to go higher but it’s not probable given the resilient job market will force FED to go ahead reducing global liquidity.

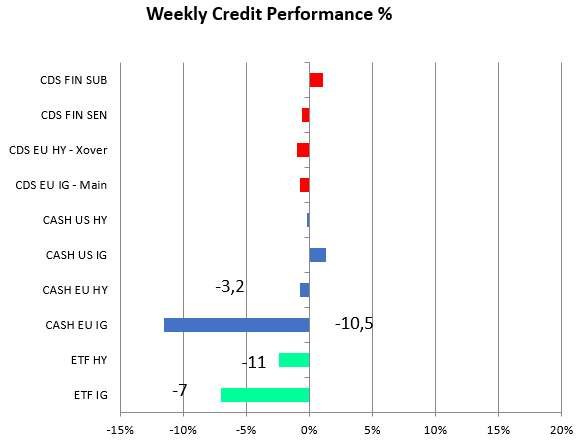

Passing now on “credit markets” we can see that considering only spreads (because total return is very positive for all asset classes given the move in rates) IG benefited more than HY (tightening 10bp vs 3bp for HY). Here the duration and the increasing growth risk could have made the difference.

I want to use the same framework here, looking at positioning (below the BNP indicators) normalizing and going near -1sd, and in the second chart again an internal breadth indicator (I show you the divergence between CCC-B and ITRAXX HY CDS). Basically the weakest sectors and names (CCC continue to underperform the single B rated names). Remember: internal, yield curve and credit markets are the main indicator to track.

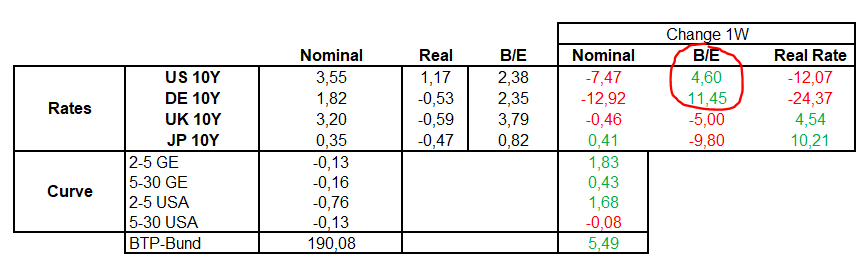

Passing now on “rates market” nominal rates continued their downtrend this week, after the also lower inflation print in Eurozone that confirmed the “we passed the inflation peak narrative”. But inside the govies market breakeven returned to increase with a stronger run of the real rate market.

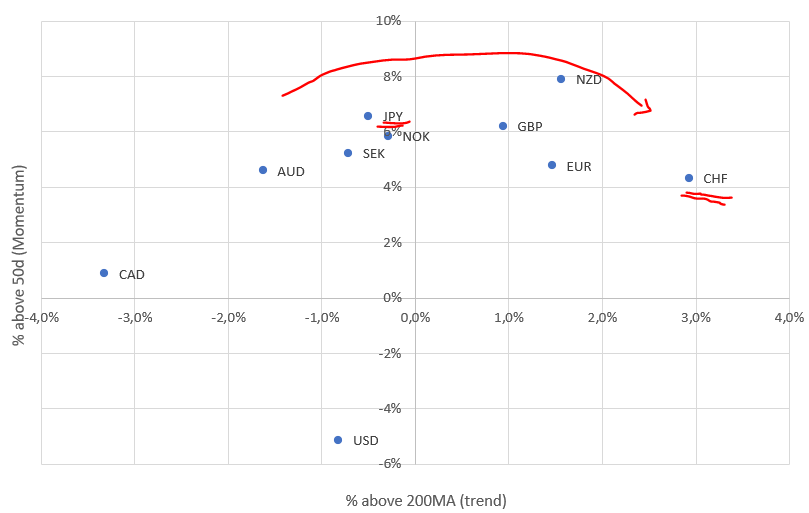

Closing on “FX”, despite I am not on the fast disinflation camp, I could accept that we could be near the end of hiking cycle of the FED maybe 1q23 (after that they will remain on hold for a some months). This reduced the positive pressure on dollar (US ecceptionalism) benefiting others safe haven currencies like CHF and JPY (this one not suffering more from the decoupling of central bank strategies). Below a clock with trend and momentum (I finded the idea from a Citi research I think).

MICRO:

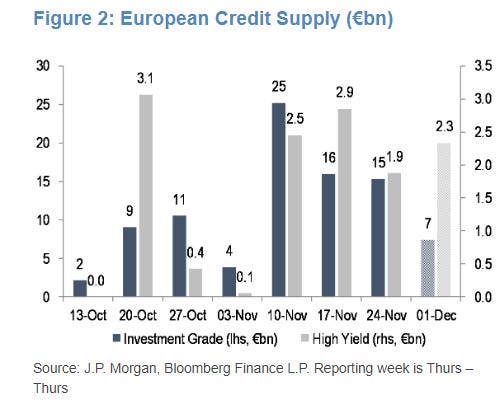

Differently from the other times I look at flow into IG and HY funds. As said before the higher risk free yield attracted varios flow from investors and asset allocators on IG, more insulated (vs HY) from the risks of a global and european recession.

It’s not a surprise, so, to view a new wave of supply going into year end. Despite, or maybe thanks in this case, to a fall in yield (calming investors on the future directions of rates) supply was well received, thanks also to the attractive new issue premiums.

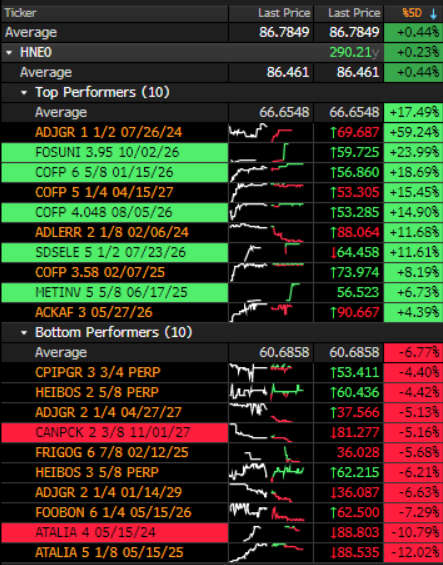

And finally the single name score. The winners are name usually associated with distress (ADLER, COFP - Casino, METINV, etc) so I will comment only the list of losers:

ATALIA: the company posted very weak Q3 results, with EBITDA in France, the core region, down 22.3%. Leverage increased to 7.9x. Atalia is under an M&A accord with CD&R that did an offer acquire Atalian’s shares. The company conditionally called the bond at 16/12/2022 but after the weak results companies agreed to extend the period to exercise the put option. Probably it’s only a problem of “price tag” and the bond could be called now mid Febrary, it’s the most rational end of the story (CD&R has a credit line opened for the acquisition) but domestical pressure is a risk here.

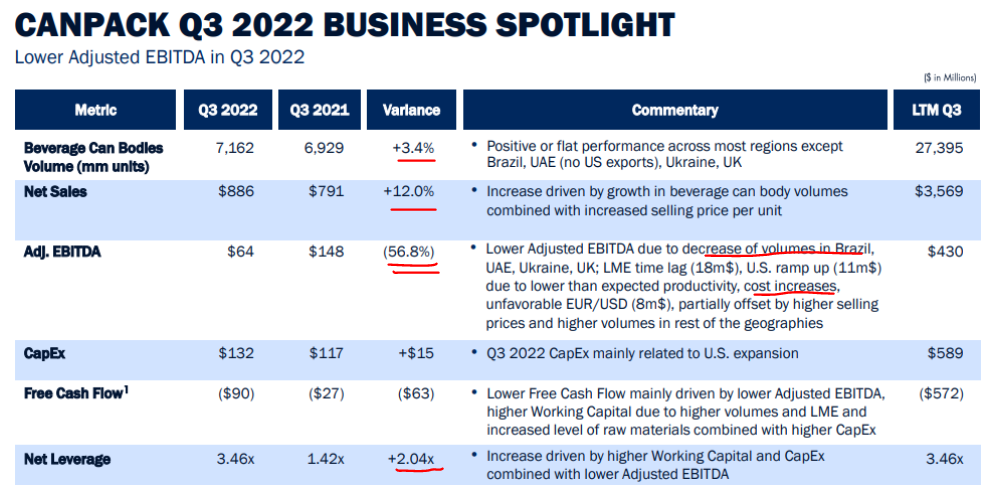

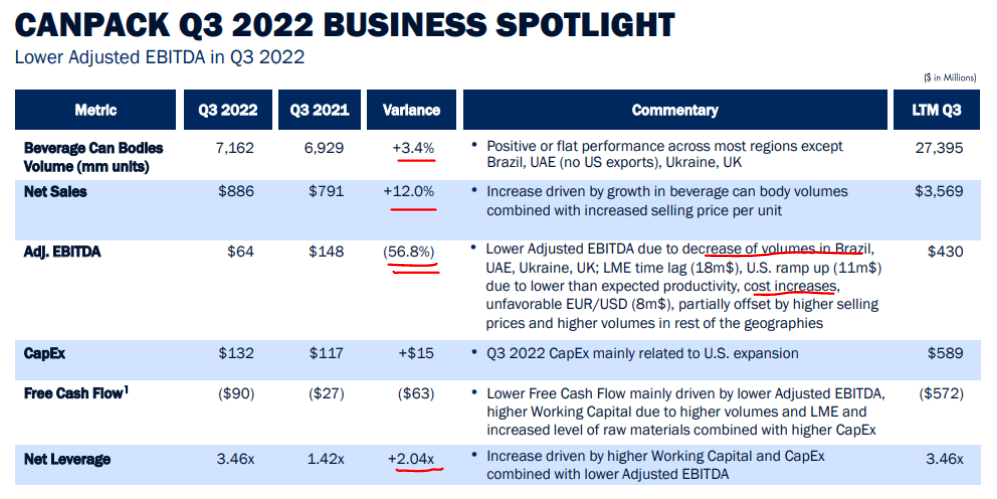

CANPCK (Canpack): is a metal can producers in Poland. Clearly with an increase in costs the margin impact was high. Strange that we did’t see it yet on big companies. Overall, volume high with high net sales but low volume in Brasil and high cost put pressure on EBITDA margin.

It’s all for today. I hope you enjoyed my job/analysis. Feel free to forward it to friends/colleague and remember to subscribe to the newsletter.