Weekly Market Review - Jan 13

Weekly Market Review - Jan 13

A thread from macro to micro

Welcome back Welcome back after this long Christmas break. I had a lot of vacation time to use and HR advised me to do so. In this first piece of the year I’ll recap as usual what happened in the week but I’ll also look back at some market indicator from a more long term point of view to have a better view of the direction going forward. As always if you like my job/analysis please subscribe below and share it and I remember you that I am also on twitter at @Credit_Junk. And now let’s see what happened this week.

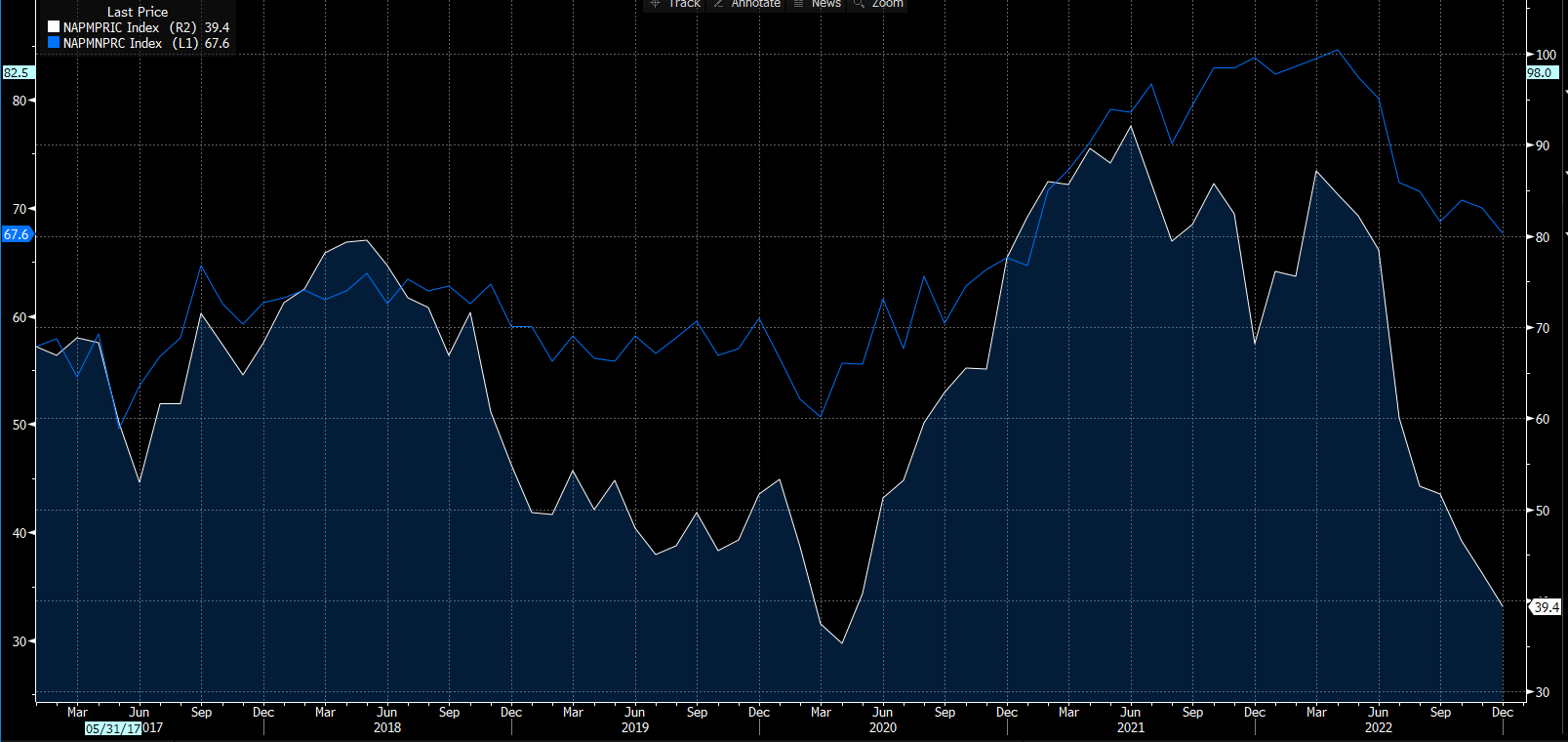

MACRO/NARRATIVE: focus of the week was again on the battle between growth and inflation. While for years the "D word” (Deflation) scared all investors and central banker (and the only driver of performance for market was only the growth), 2022 was the year in which inflation took center stage again. Newflow and economic data were positive in the USA, with employment remaining strong and price pressure from leading indicators (ISM manufacturing and services price paid published last week ) continuing to decline.

It’s for that that the US CPI for December this week was so important:

CPI headline declined from YoY from 7.1% to 6.5%

CPI ex food and energy declined from 6% to 5.7%

US CPI -0.1% mom; core +0.3% mom

Both printed in line with estimates but it is the sixth month in a raw of declining, with a continuation of the trend of falling energy and food (where FED has less control) and in core goods (after a spike due to Covid).

In the meantime the core services component continued to drift higher, with the usual rent of shelter but also the hospital and health related services and transportations.

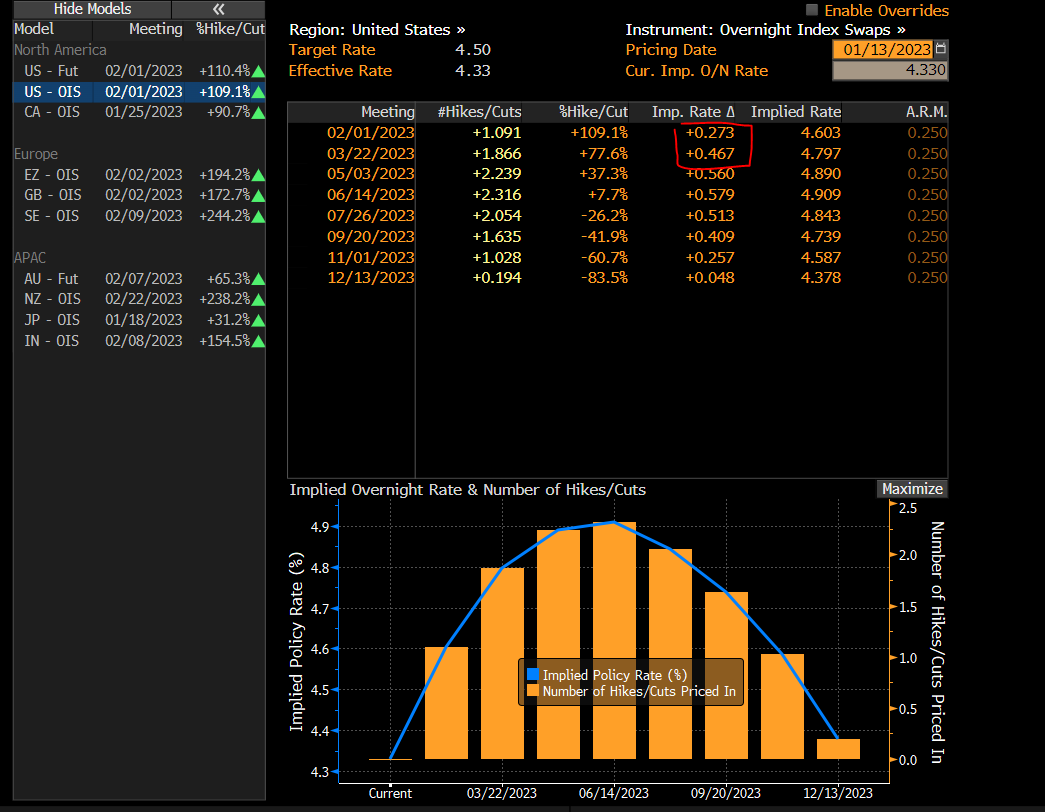

This lower inflation print gave green light to bet on a downshift of rate hike expectation, with only 25 bp in February and one more in March always of 25bp.

On the political front this week is interesting to look at German government to call for a new instrument (and a joint issuance program) to help Eurozone to compete against United States and their Climate act to support green investing. This helped the sentiment on euro government bond (especially BTP-Bund).

MARKETS: As said before this the first piece of the year so let’s look at changes YTD to have a better outlook.

Let’s start with the rates market. Market continued to betting a softening inflation outlook and is rapidly returing to the bottom of December both in Eurozone (fucsia below) and in US (green). There is also a strong divergence in surprise index with better economic data in eurozone driving (and a ECB more hawkish) driving a narrowing of the UST/Bund spread.

Remaining on fixed income but passing at spread BTP-bund is returing near their FV of 175bp.

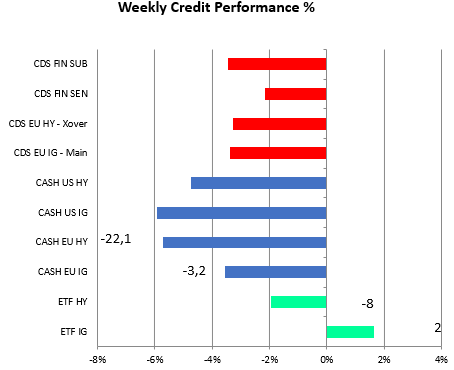

Passing at credit the fall in rates (with also that one of volatility) boosted the search for carry and HY and IG both tightened (-22 and -3 respectively).

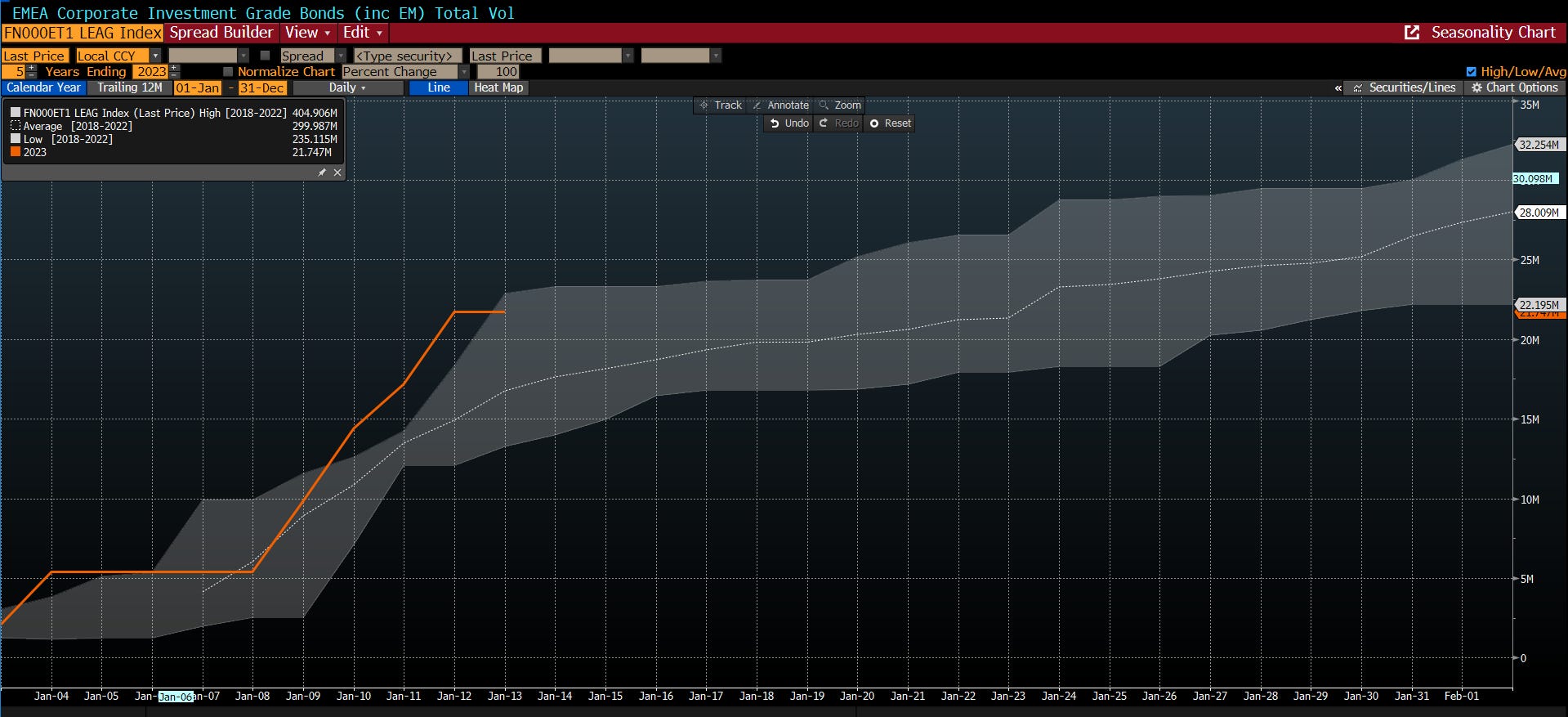

IG underperformed, despite being more related to duration, amid the high level of supply. A lot of deal (considering seasonality) were announced, especially in the financial sector. Going into next week we will enter into the blackout period of the reporting season.

From an intermarket point of view the two ETF ratio I follow (IG/Govt and HY/IG) to have a better undestanding of the credit direction (credit is the driver of growth) had a impressive start of the year, confirming the direction of the overally HY market (in orange the Ishares HY) and of the equity market (below in blue the SXXP european index).

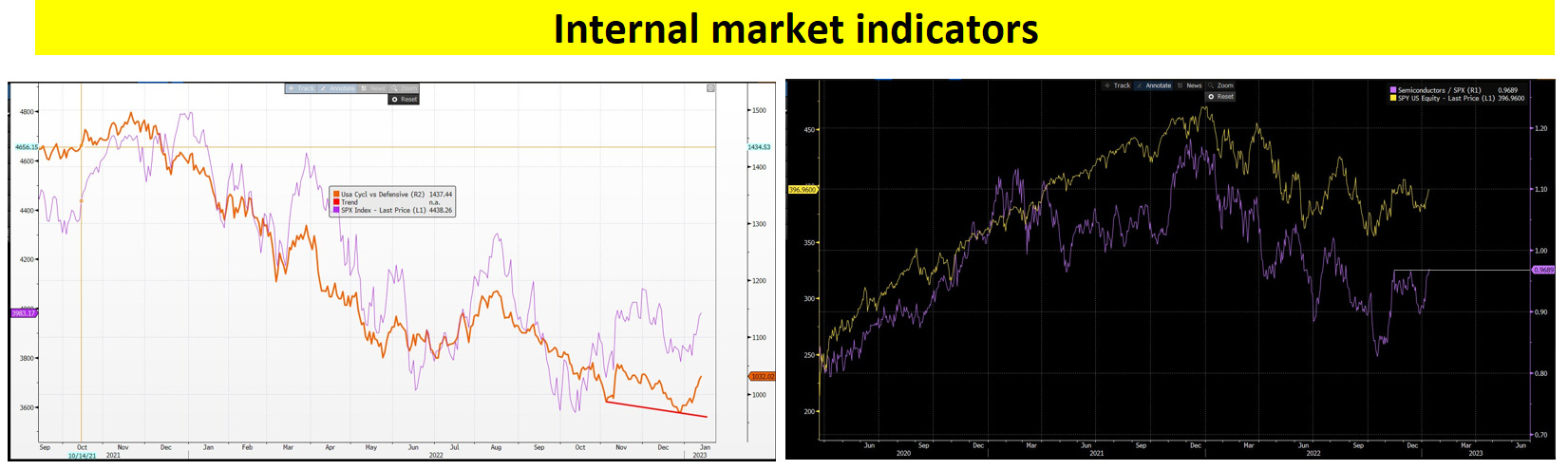

Remaining on the equity market (but now on US SPX) below two internal indicators confirm the better economic data and the bounce in equity. On the left the cyclicals vs defensive, on the right the Semi/SPX. Also liquidity was supporting, with TGA balancing the shirinking in FED Assets reduction.

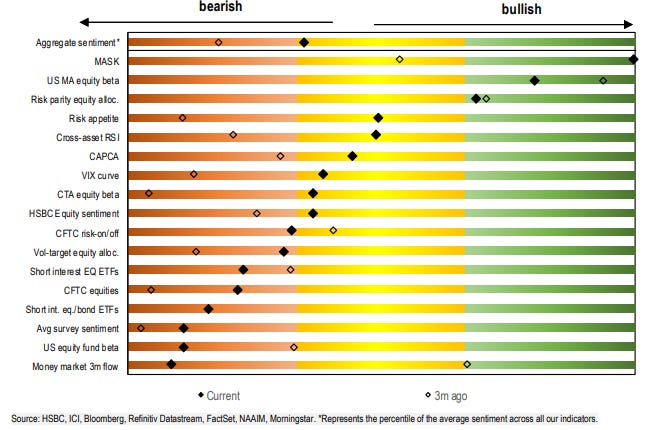

To sum up equity was supported by a trifecta of factors: fundamentals (better macro and lower inflation), lower rates (and better liquidity environment) but also from sentiment/positioning (that using the HSBC composite indicator) remain also slightly bearish.

MICRO:

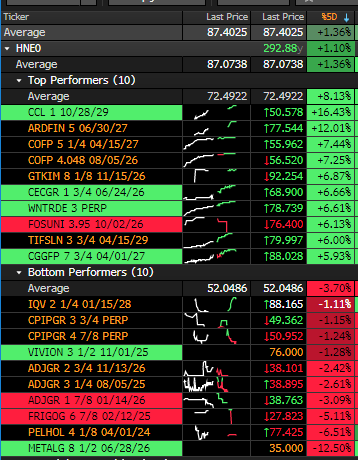

In the HY market the single name performance not seems related to single name news but beta related. Despite this:

CCL (Carnival) and others travel-related names was supported by optimism on FED reducing tightening and by China reopening;

ARDFIN (Ardagh Finance) will report on February 23, 2023 the Q4 2022 results

PELHOLD (Adler Pelzer): here the clock is ticking on the bond refinancing. Company is offering money to investors to stay invested trying to amend some details of the bond prospectus.

It’s all for today. I hope you enjoyed my job/analysis. Feel free to forward it to friends/colleague and remember to subscribe to the newsletter.

Thanks always informative as I’m not a credit specialist!

Thanks for the write up!