Weekly Market Review - Jan 27

Weekly Market Review - Jan 27

A thread from macro to micro

Welcome back at the weekly recap, as usual at the end of the week. As always if you like my job/analysis please subscribe below and share it and I remember you that I am also on twitter at @Credit_Junk. And now let’s see what happened this week.

MACRO/NARRATIVE: This week the preliminary PMI for US and Eurozone confirmed a better than feared growth momentum (despite the surprise index continue to favour the Eurozone).

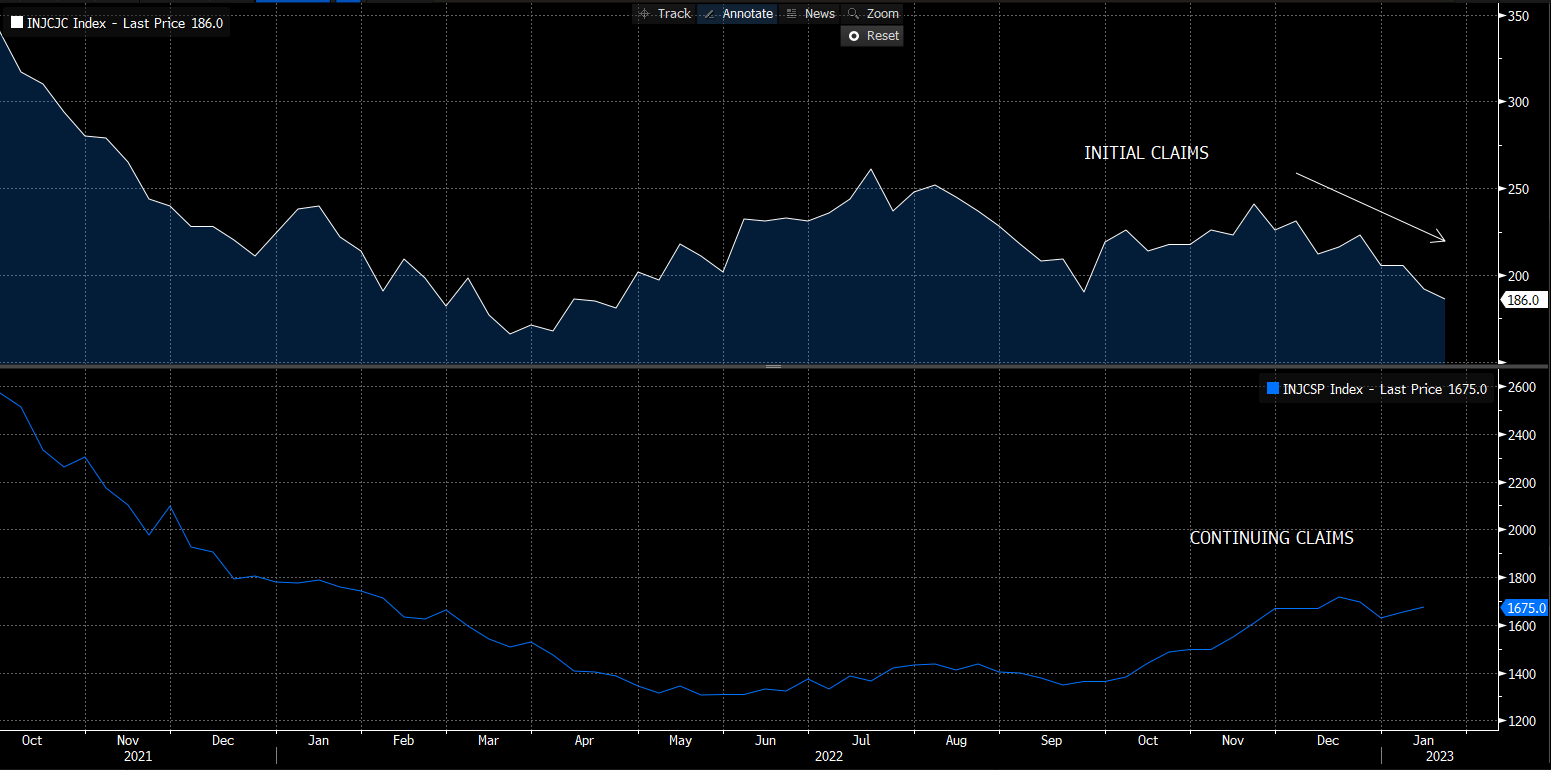

Also the US GDP for 4Q was a double check for it, given an increase of 2.9% annualized for 4Q after a gain of 3.2% for 3Q. The main contributors were consumptions (despite being less than expected and inventories). Despite being a laggard indicator, job market continue to remain strong (and always tight) with initial claims continuing to fall. I add at the consideration the big numbers of layoff we are seeing in the tech sector. After years of easy money (and easy financial conditions) is it possible that the high rates environment will do a cleanup of some zombies companies? We will see.

To sum-up the data of the week (and the market think it too) are that one of a “new goldilock” scenario (“a not too hot not too cold economy”) consdering the peak in inflation we saw in the United States too. Going into next week, where we will have both ECB and FED, this could support FED decision to do an other dowhshift, hiking “only” 25bp and waiting to evaluate better the impact of their past decision on the economy. The ECB will probably hike by 50bp signaling a similar move for March after the strong verbal interventions of many ECB speakers in the past two weeks claiming against a premature slowdown.

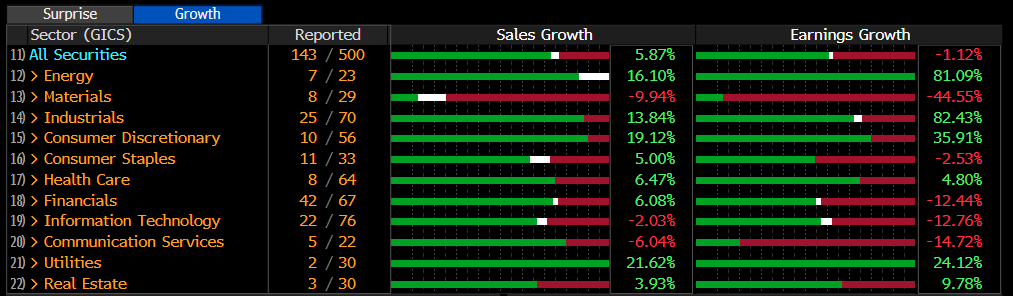

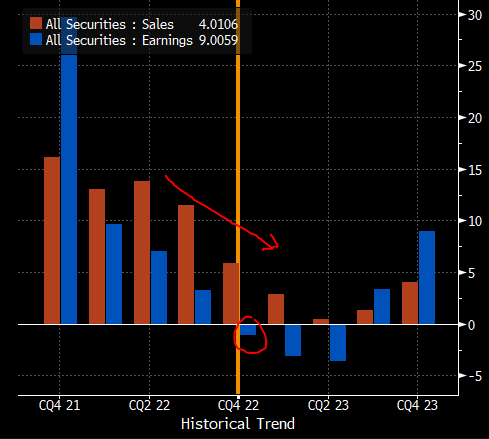

Spending some words on repeorting season (below for SPX), while expectations were revised lower, sales growth continue to remain positive but declining while earning growth for the quarter is negative, with the impact of high cost starting to impacting it.

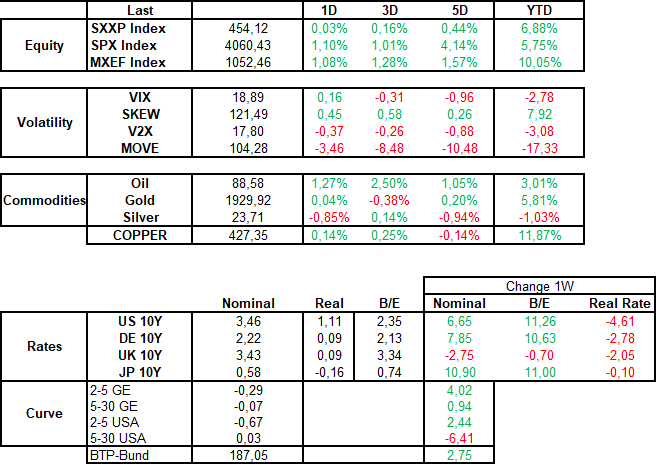

MARKETS: Below the movement of the week of the main asset classes. Thank to a better growth environment in the battle between “hard landing” and “soft landing” equity market it was the last to win for the week with a good performance for S&P (+4%) and EMSCI EM (+1.5%).

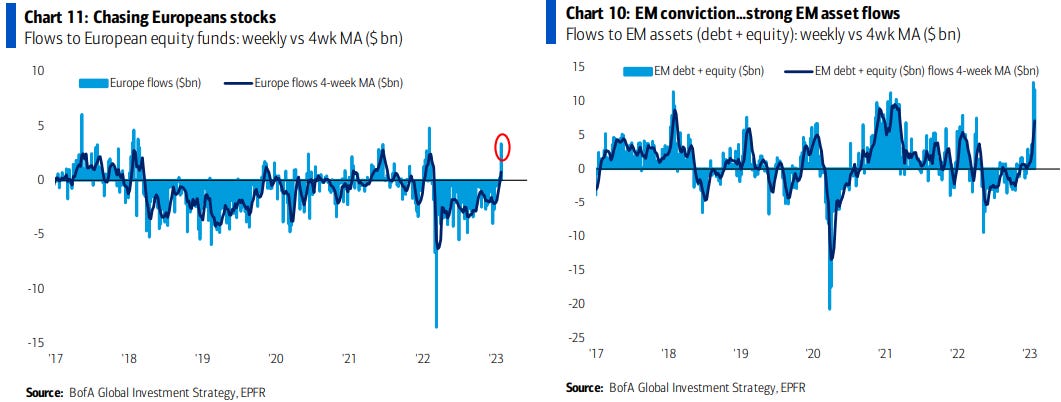

European stocks (SXXP) is almost flat this week. I associate this to a more crowded positioning after the better surprise index we talked in the past week (lower gas prices helped to avoid a recession here) and the better YTD performance. Also the EM benefiting of China reopening is a consensus trade but here valuations are more interesting and the road ahead is a lot (despite will be a bumby road).

China and better data in USA helped also energy market this week with oil up +1% but especially the products market (gasoline, diesel and jet fuel). Below a small thread with some interesting fundamentals charts of the sectors.

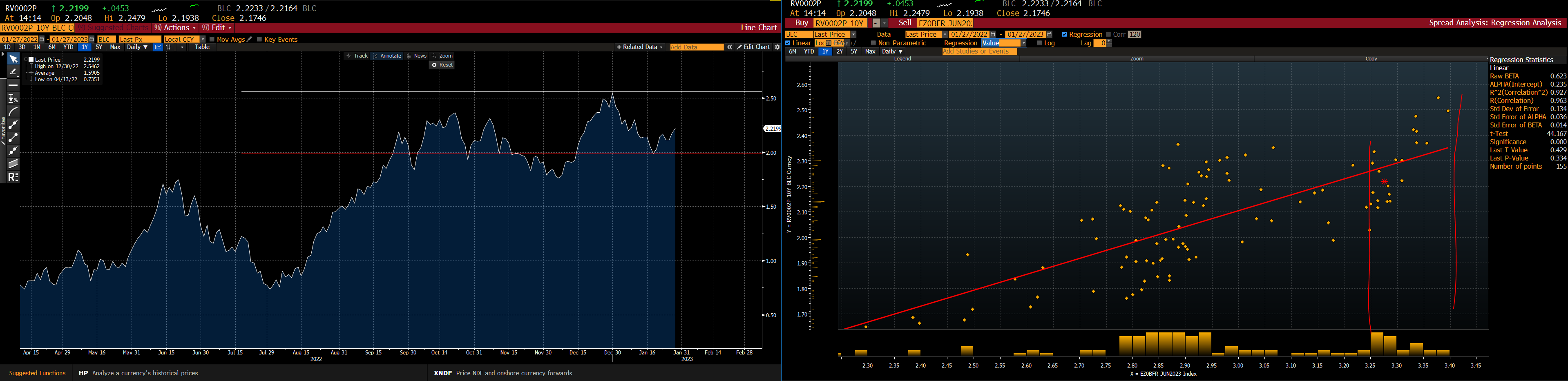

In the fixed income space nominal rates we had some profit taking on bonds with rates increasing in USA and EU. Market entered the year too short of bonds in front of the rally we saw. Now positioning is more neutral going into a central banks week. Looking at 10y Ger bund, and taking a terminal rate between 3.25/3.50% valuation suggests a rates between 2.20% and 2.50%.

This week the MOVE (volatility of bonds and rates) continued to compress favoring the carry trade, and especially in credit markets. HY tightened 11bp while IG of 7bp (outperforming HY beta adjusted). Given the low duration, in a week of higher rates, the total return for HY was higher than for IG (below the green light with the ratio between the two). Like equity also other the IG/Govt ratio stalled. Let’s look at this for divergences vs equity and HY ETF.

But from a valuation point of view not all market price growth risk in the same way. Below why here I prefer IG to HY (euro bonds). IG price at 75% percentile of the last 10y, HY near 50%. So HY is 300bp far from the past peak in spread related to past recessions.

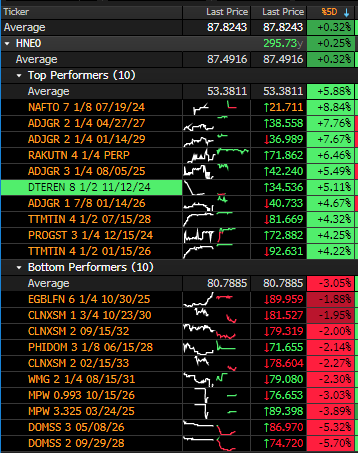

MICRO: Reporting season in Europe (despite lagging that one in USA) is starting to impact HY market, but also other some topics too:

DOMSS (Dometic) is a global provider of products for outdoor and residential in Food&Beverage, climate and power & control. An example of product is a mini fridge for outdoor (RV or boats). Results for 4Q missed expectations with revenue -11% (vs -7.8% consensus) impacted by weak demand and EBITDA declining -24%. A more positive WC (due to declinig demand) helped to arrive at a positive FCF;

MPW (Medical Properties) bonds (and stocks) dropped on short report by Viceroy (“Medical Properties’ assets are “massively overstated” as a result of unprofitable transactions with its tenants, Perring’s Viceroy Research said in a report Thursday.”)

TTMTIN (Jaguar) reported on the week, with decent results. Revenue 3Q +28% YoY thanks to better model mix, EBITDA margin at 11% (down 10bp YoY but up sequentially +160bp QoQ. FCF positive to undwind of working capital and solid liquidity 5.4bln (3.6bln £ in cash).

It’s all for today. I hope you enjoyed my job/analysis. Feel free to forward it to friends/colleague and remember to subscribe to the newsletter.

great take, thank you!

I have the feeling credit markets will be a lot more boring in '23. Carry trading will certainly be the name of the game.

We will get more information next week after FOMC and ECB and if they turn out to be non-events then we have to adjust to the new environment.