Weekly Market Review - Nov 04

Weekly Market Review - Nov 04

A thread from macro to micro

Welcome back at the weekly recap, as usual at the end of the week. As always if you like my job/analysis please subscribe below and share it and I remember you that I am also on twitter at @Credit_Junk. And now let’s see what happened this week.

MACRO/NARRATIVE: market focus this week was again on two central banks after ECB last week. This week we had:

FED: they raised rates for 4th consecutive times by 75bp to 4% and said that could be appropriate to slow the pace of increases to 50bp/70bp at meeting (this is the dovish part of the statement). Together they said the they need to continue hike rates ahead of previous anticipated and to mantain rates in restrictive territory for a period to slow down inflations (this is the hawkish part of the statement with terminal rate returing again near 5%). So it’s premature to stop but forward guidance need to consider cumulative tightening and lags.

Today we had also the payroll data for US, a measure overwatched for us job market that remain very tight. There was 261k new jobs created (higher than expected). Hourly earnings yoy decreased but were in line while unemployment increased to 3.7% from 3.5% but in part for a effect on partecipation rate. So if there is an other strong inflation print next week, with this job market (ok it is a laggish indicator) FED could go for an other 75bp also in December.

And finally we had also the BOE, always remaining on central banks. After the volatility we had on GBP and gilt BOE decided to hike 75bp as the market expected (while 1 month ago they surprised rising less than expected) to fight inflation. But the dovish surprise arrived when they said that they will not raise as market expect otherwise a recession will be for sure in England.

MARKETS:

RATES: With central banks meeting it’s not a surprise to see rates rising. In US the 10y rose 11bp while in Germany the 10y rose 15bp. Both movements were driven by rising real rates, with a focus on higher terminal rates. So not exactly a pivot for rates. Curve continue to flatten, driven by the short term part of the curve (the typical bear flattening) while BTP-bund widened 7bp (there is a great directionality of the spreads);

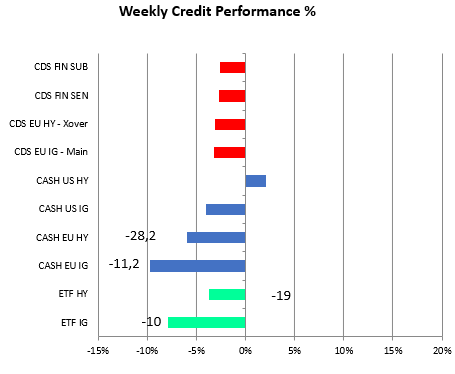

CREDIT: the weekly performance of spread product was very strong, despite a high level of rates. HY and IG tightened 28 and 11bp, with an outperformance of investment grade. This could be a confirmation of a market starting to look beyond the terminal rate with a decrease in rates volatility (MOVE index). Credit is driven both by the level and the direction of rates but also volatility is a great indicator for carry strategies. Below my hipotesis for a fall in MOVE (It’s a mini thread of 2 pieces).

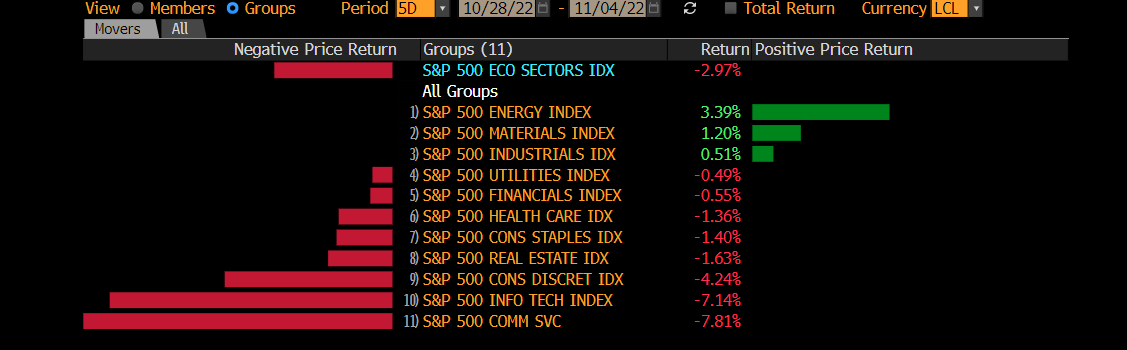

EQUITY: here we can apply the same concept of credit, it’s a lot technical but we have a fall in volatility associated with increasing of equity market. Also the Vix curve is very compressed. So we have the paradox of low positioning via futures and low sentiment (that helped the rebound too) and long call position via short term call option. A funny game, until it works. Looking internal of the market the leading sectors are again energy and materials (an alarm bell from a sector rotation point of view, these in facts are sectors that benefit from high inflation).

From a techincals point of view there is some softening of momentum (lower MACD) after FED that confiermed implicity their intention to have a tightening in financial condition, this means lower equity market. Despite this SPX is down 2% this week while SXXP is up 1.9%.

Finally some comments on FX (where GBP was the underperformer after a dovish tilt by BOE and the problems that remains) and Commodities. Here we have soft commodities flying (with Cotton +21%, Sugar and Cocoa +6% for both) while energy and metals rebounded for rumours of China exiting 0-covid policy and, expecially for oil products like gasoline (+8% this week) and Diesel (+1%) for a very low level of inventories and lack of refining capacity.

MICRO:

On single name some more words on winners and losers.

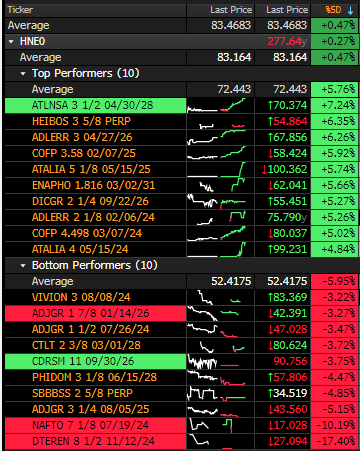

ATLNSA (Antolin): I have not particular news but in a risk on environment low cash price with high beta could outperform, if you have some better news let me know;

ATALIA: announcment of call on the 2025 bond at mid november, positive for the context and the name

COFP (Casino) after the report last week they announced tender offer for short term bonds

It’s all for today. I hope you enjoyed my job/analysis. Feel free to forward it to friends/colleague and remember to subscribe to the newsletter.

Once again, thanks for the analysis always a useful resource. What is the relationship of CDX, cash and ETFs and how do they intertwine and move credit spreads?