Weekly Market Review - Nov 11

Weekly Market Review - Nov 11

A thread from macro to micro

Welcome back at the weekly recap, as usual at the end of the week. As always if you like my job/analysis please subscribe below and share it and I remember you that I am also on twitter at @Credit_Junk. And now let’s see what happened this week.

MACRO/NARRATIVE: A lot happened this week and volatility of the market reflected this:

The week started with rumours about a imminent China exit for “0-covid policy”. While denied immediately from national authority. While numbers of cases are rising again in the country (especially in some provinces like Bejing and Ganzgzhou this week a Covid comitee decided to:

Cuts quarantine period for inbound travelers to 8 days from 10 days;

Cuts quarantine period for close contacts to 8 days from 10 days;

Accelerate vaccination (prepare for reopen)

Accelerate Covid medicine inventory (prepare for reopen)

These news, together to the fact that Chinese Mrna vaccine is in stage-3 for approval, let me think that despite reopening is not imminent, something could happen in 1Q 23.

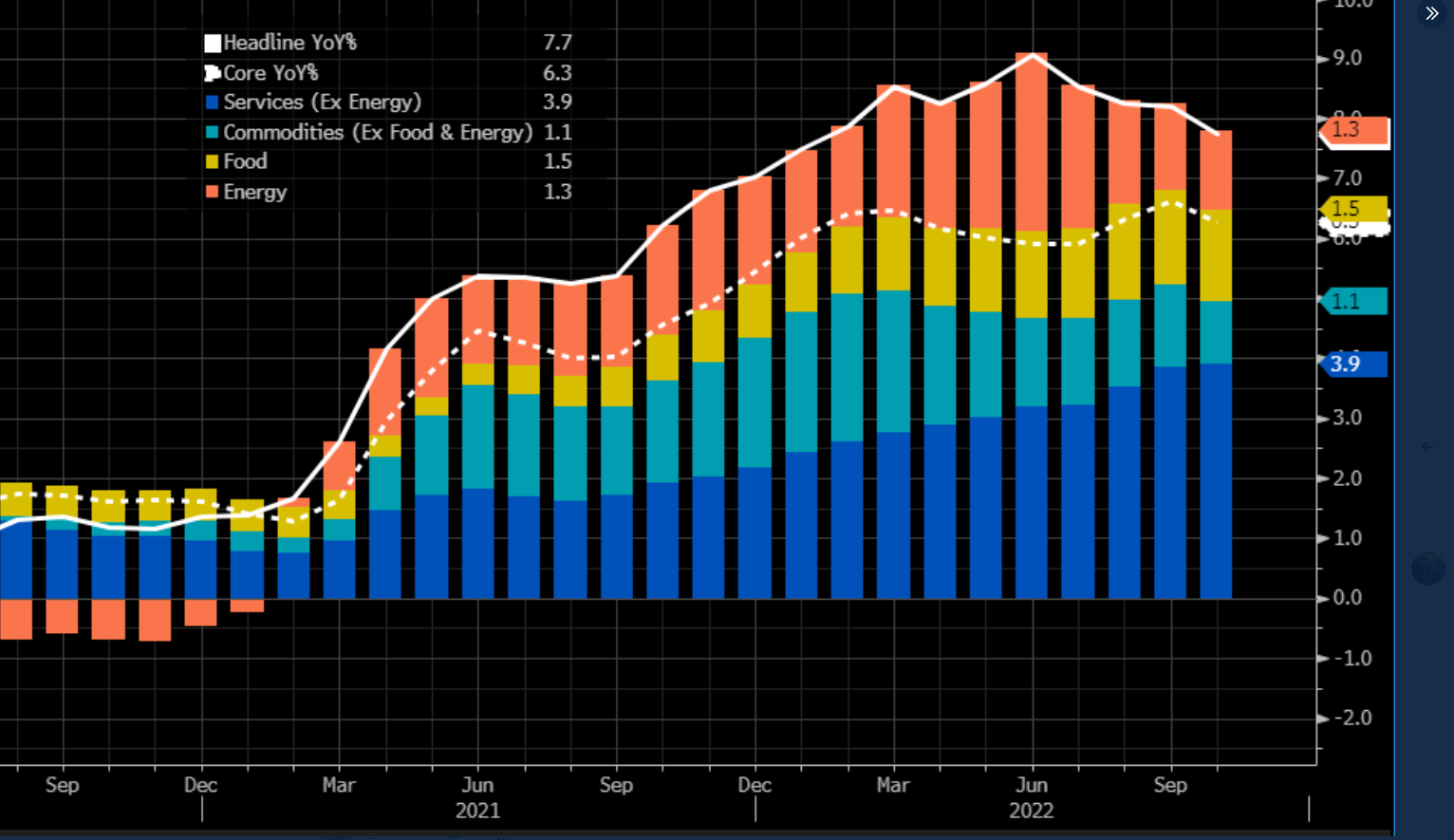

The other market focus of the week, in addition to the “crypto crash” related to FTX.com exchange, is the inflation data for October in USA with the CPI surprising on the downside. Looking at YoY data CPI headline decreased from 8.2% to 7.7% (below expectation of 7.9%). Also core data decreased from 6.6% to 6.3% (below expectation for 6.5%). The usually trend of slowing in goods and energy continued, while for this month it seems we had also a top in services components.

Passing now at the monthly change we had:

US OCT. CONSUMER PRICES INCREASE 0.4% M/M; EST. 0.6%

*US OCT. CORE CONSUMER PRICES RISE 0.3% M/M; EST. 0.5%

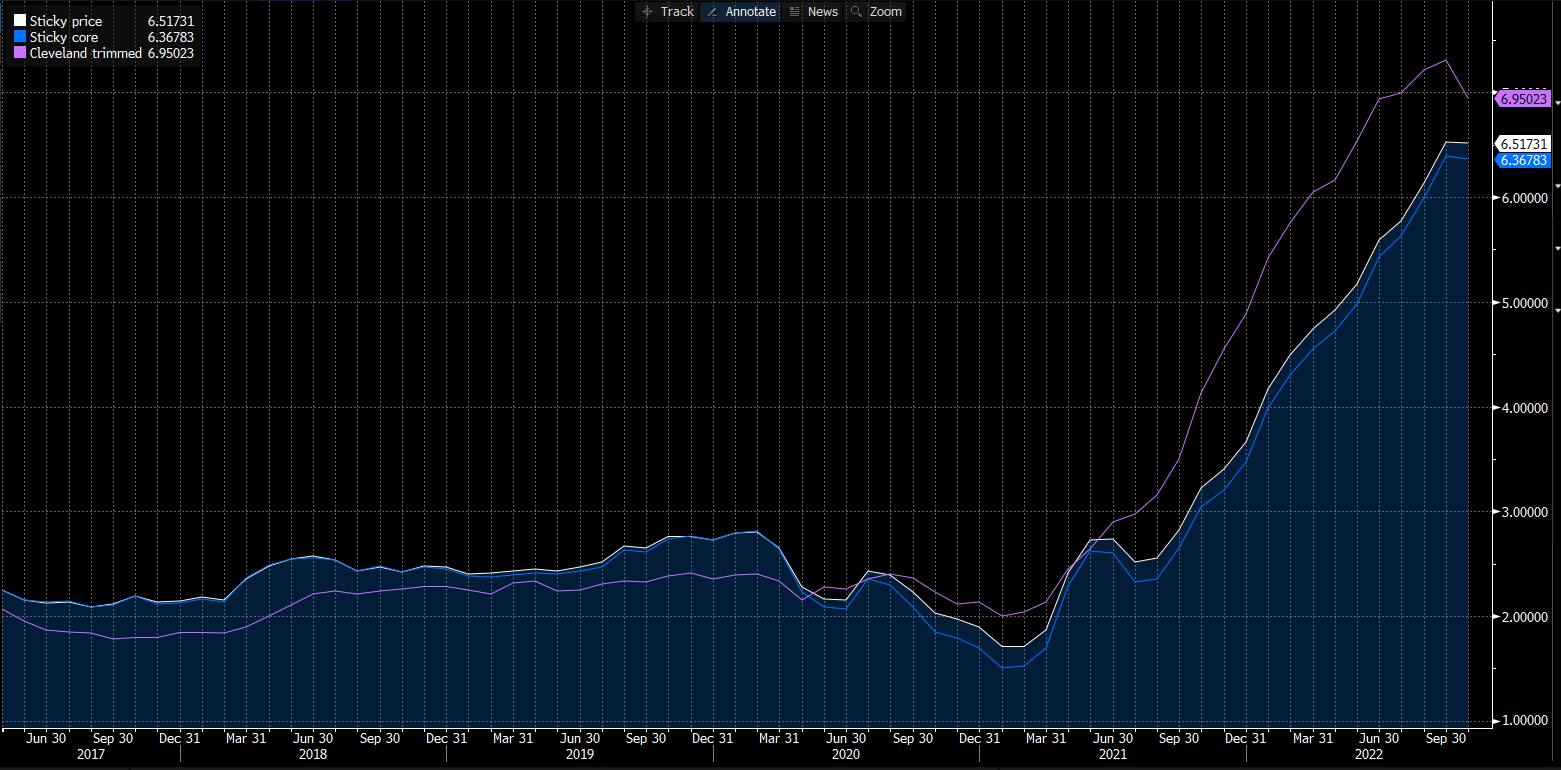

with a negative contribution for transportation, apparel, and medical care services. Also Shelter, in green, declined in contribution term. An important fact is that the sticky part of inflation stopped to rise and the Cleveland trimmed inflation (that excludes the biggest outliers in either direction from the index’s components, and takes the average of the rest) declined slighlty. Both indicators are usefull for measure the underlying inflation.

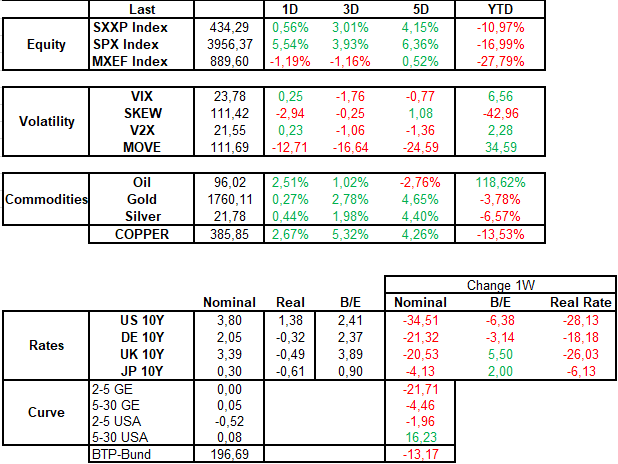

MARKETS: Below a screenshot of what happened this week in global markets. Looking at price action in the market and at the newsflow of the week it’s natural to start talking about rates markets.

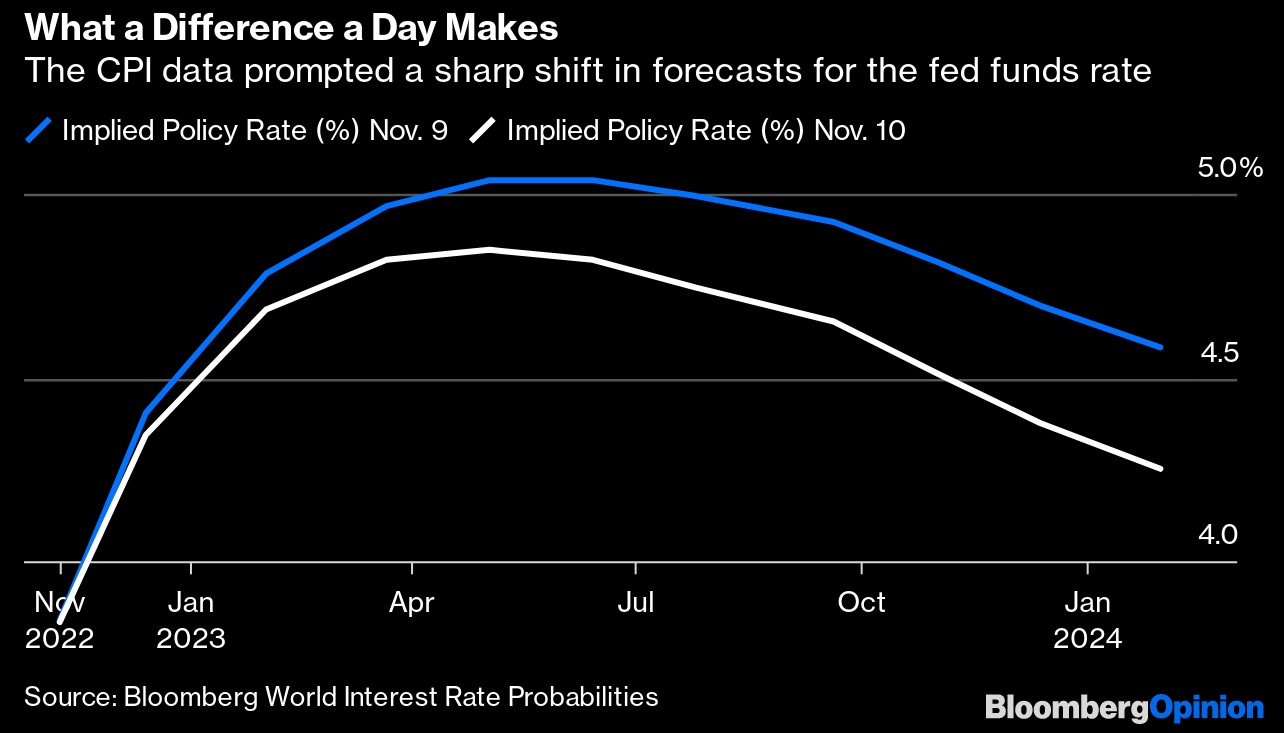

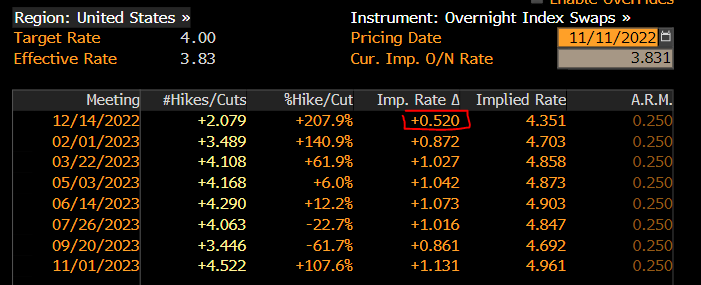

In RATES the impulse for global market started clearly from the USA, after this lower than expected CPI print. Market repriced immediately the future path for FED rates given for sure a hike in December of only 50bp (Powell said it is appropriate to slow down the pace of increses) but looking also by the curve (below from a piece of @johnauthers) the market repriced down also the terminal rate (now below the 5%) that is exactly the opposite of what Powell said (“a higher than previous anticipated terminal rate”). All the govies curve shifted down (-30bp the 10y USA, -20bp the 10y Germany) with a bull flattening move of the curve. Only the 5-10 USA curve steepened (usally it’s the first part of the curve to steep, 2-3 months before the last hike). BTP-bund spread tightened, given the directionality of the spread at rates. My view? Rates tightened too much in Europe. A 10y below 2% in Germany is too tight considering we have not seen the high in inflation in Europe. For govies spread (BTP-Bund, OAT-bund, etc) I have a negative view given the ready to start QT.

In CREDIT spread had a monster reaction with HY tightening 41bp while IG 3bp. XOVER (the HY CDS) broke the 500bp level. In term of total return all asset classes had a positive return with a rebound of at least 1%.

A big driver for the performance of spreads and credit was the tightening in MOVE (the vix for bonds). My hipothesis is that we reached a consensus for inflation, with lower dispersion and lower uncertaintly (below I calculated the higher - the lower estimates for core inflation, this track very well the MOVE.

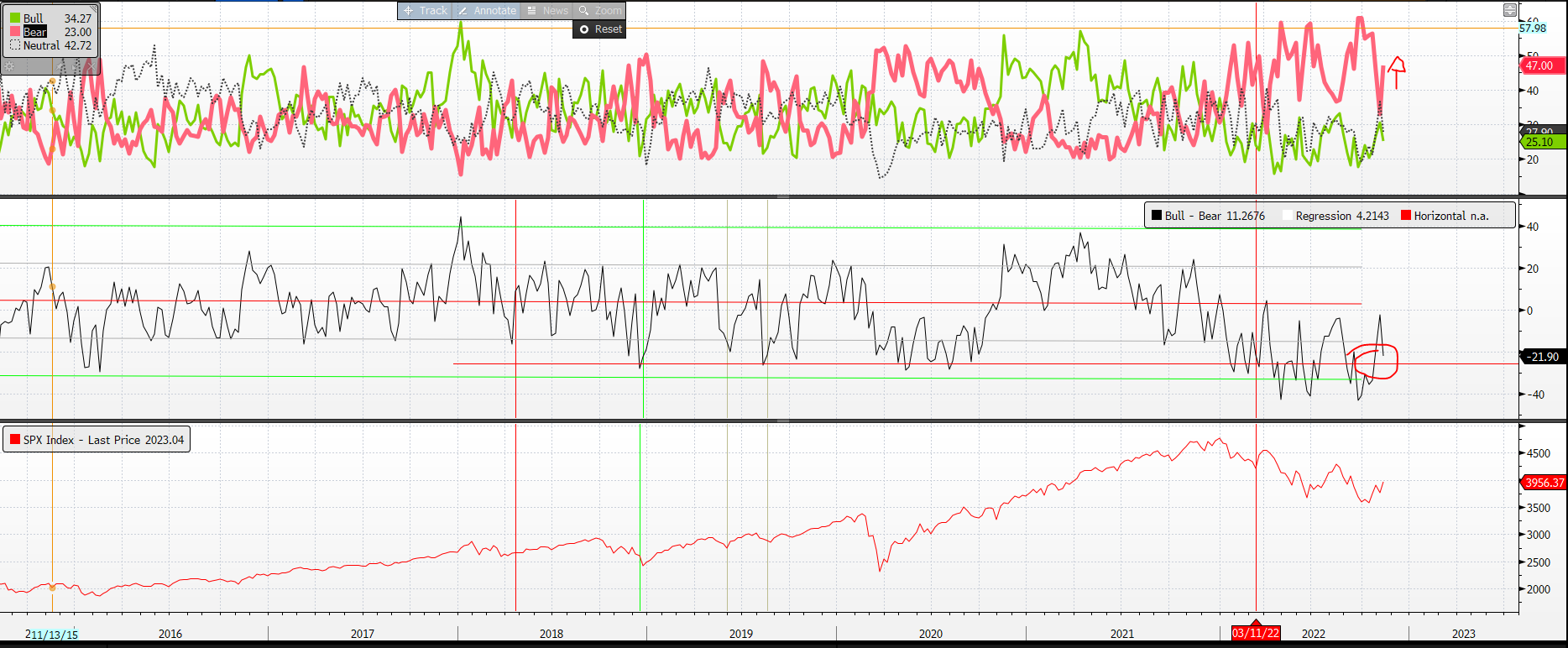

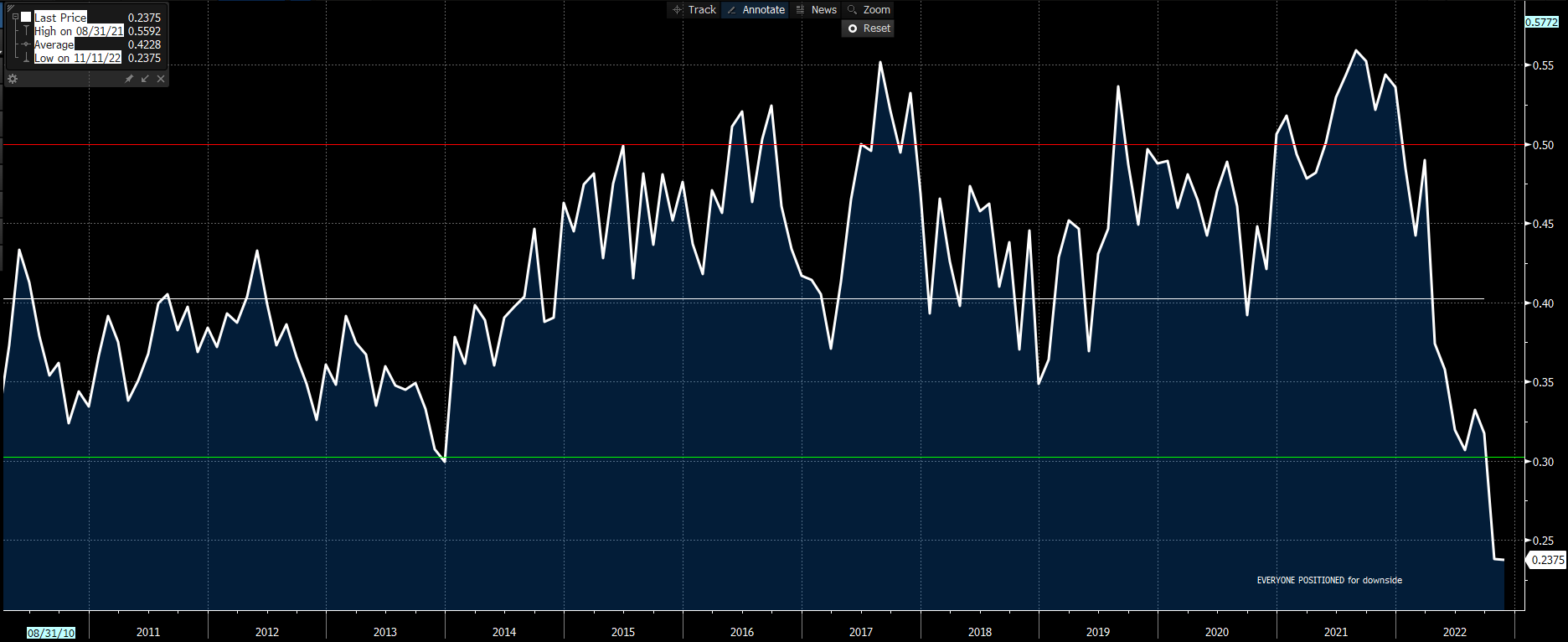

Passing now on EQUITY SPX and SXXP closed up 4-6%. The technicals of the market are supportive for this rebound to continue with a weak sentiment (AAII Bear - AAII bull remain low) and everyone positioned for a downside (below the 3M skew put-call).

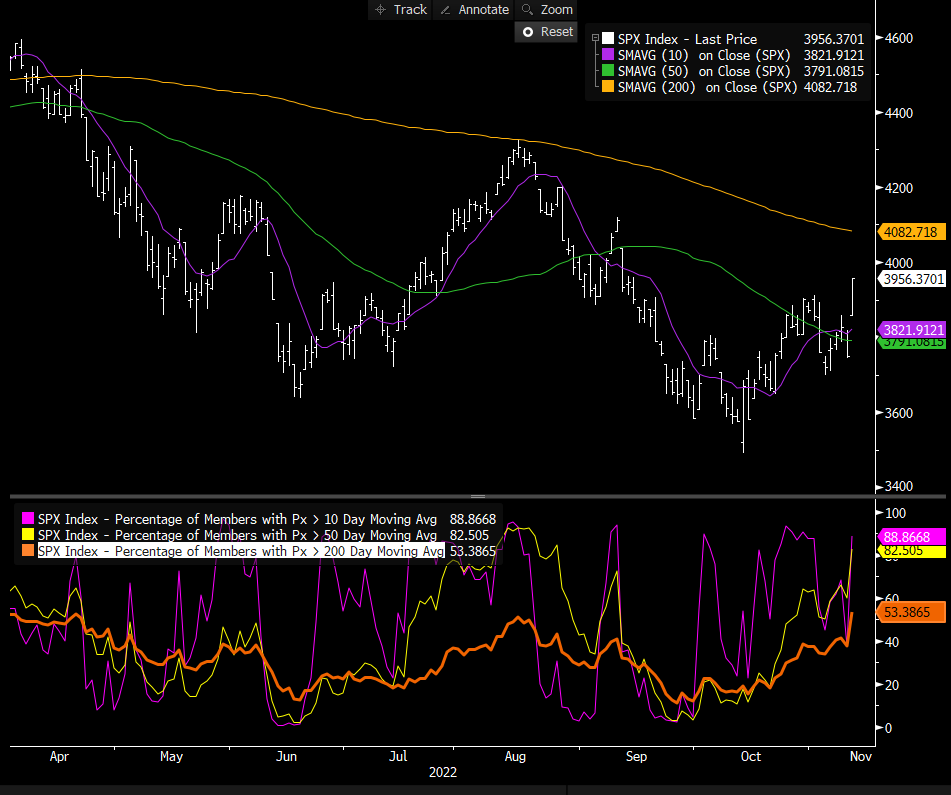

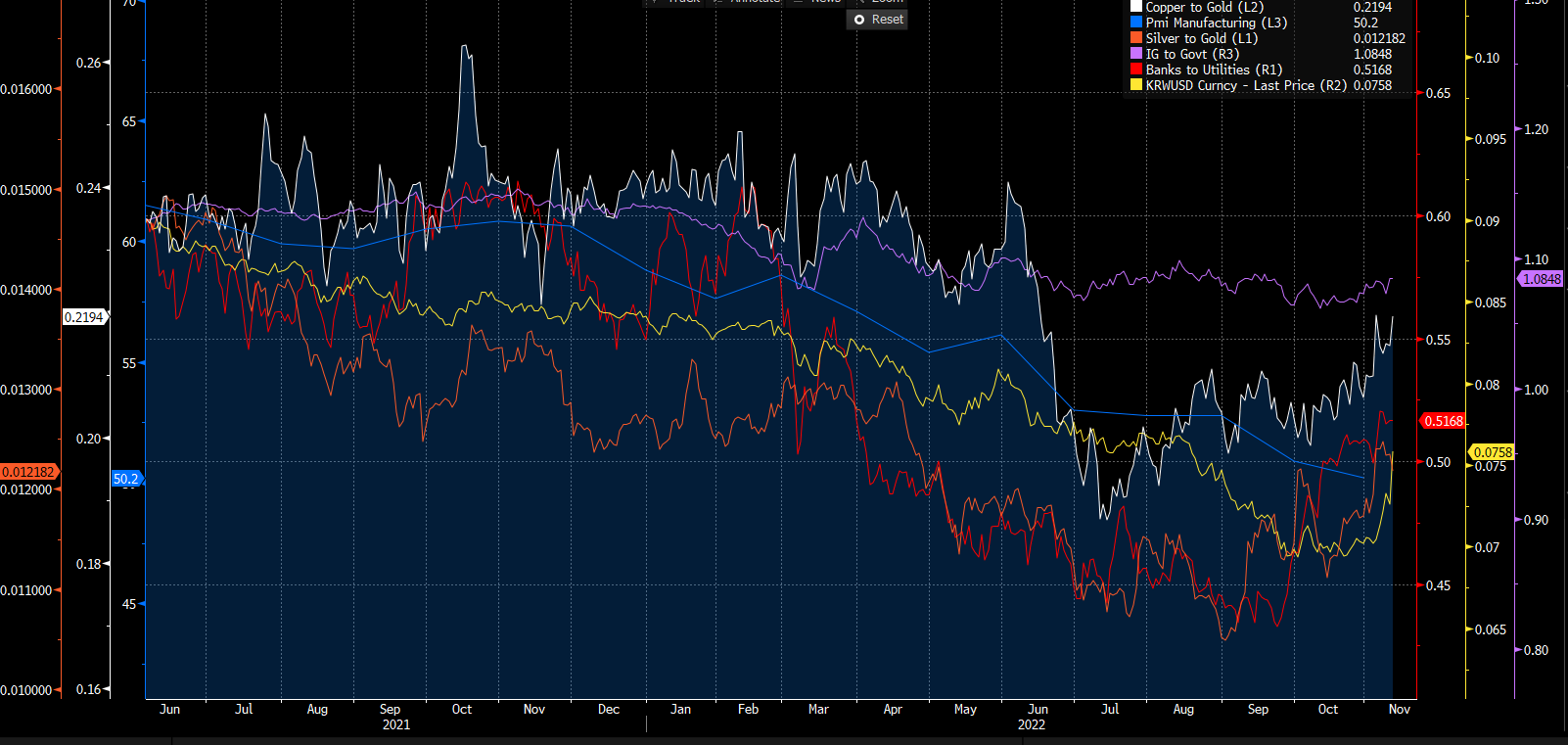

Also the breadht is supportive with the percentage of members inside S&P above 50 e 200 moving average both rising and cyclical outperforming defensive both in USA and EU. The internal foces of the market is one of the best economist on the planet.

I finish with a intermarket view. Let’s start with commodites. Both copper to gold and silver to gold (two cyclical ratio) are going up, and also banks to utilities in equity. In FX world Korean won ( a proxy for global growth) exploded higher, thanks also to a general weakening of dollar, after this lower CPI print).

MICRO:

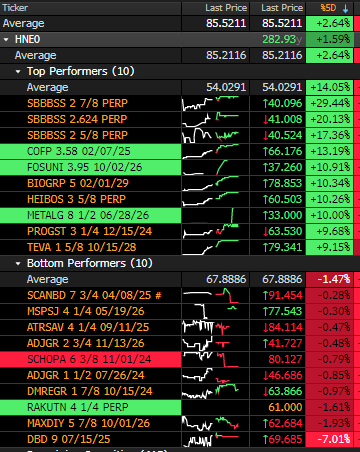

As seen above the week was very positive for risky assets. Clearly the high beta sectors and names benefit of it but let’s look at some idiosyncratic events.

SBBBSS (SAMHÄLLSBYGGNADSBOLAGET I NORDEN AB) announced a tender offer on hybrids and senior notes

COFP (CASINO): bought back €67m of Quatrim 2024 senior secured notes

DBD (DIEBOLD NIXDORF) reported Q3 earnings below consensus and price was down -7%. Sales declined -15.4% yoy to 810M $ while adj. EBITDA fell 26.4%.

It’s all for today. I hope you enjoyed my job/analysis. Feel free to forward it to friends/colleague and remember to subscribe to the newsletter.