Weekly Market Review - Nov 18

Weekly Market Review - Nov 18

A thread from macro to micro

Welcome back at the weekly recap, as usual at the end of the week. As always if you like my job/analysis please subscribe below and share it and I remember you that I am also on twitter at @Credit_Junk. And now let’s see what happened this week.

MACRO/NARRATIVE: This week we did not have a long list of headline, we did not have a long list of central banks meeting so it was a light week where only fundamentals data and central banker speech moved the market. Let’s see the most important:

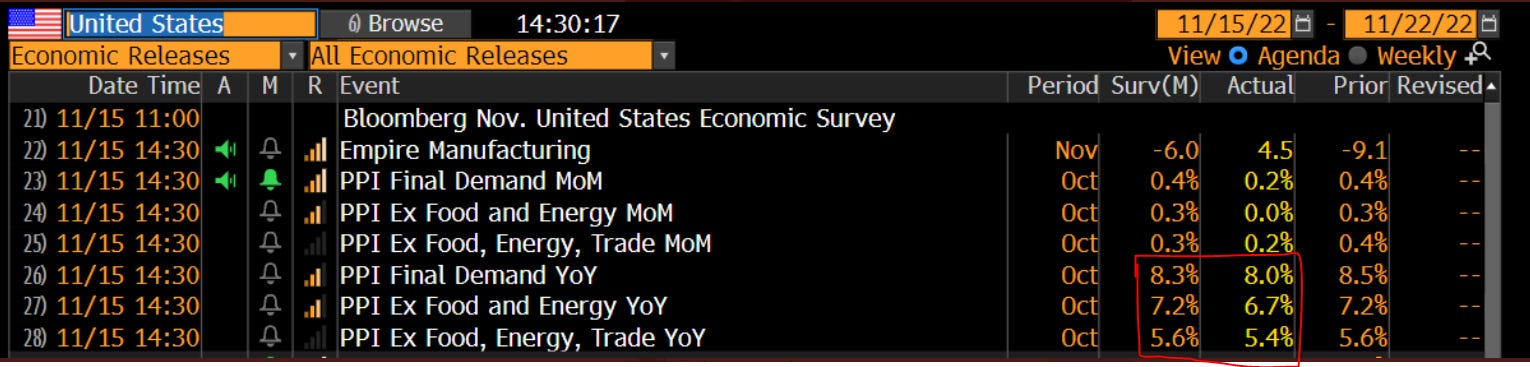

PPI (Producer Price Index) in USA was the most important given the focus on inflation. The data for October printed lower than September (but also lower than estimates), in line with the fall in CPI.

We had an increase in Goods (entirely in food and energy) but on Services we had a fall in trade and trasportations, that is good for next prints of CPI;

While we had this data confirming the possible peak in inflation (and market started to remove some hikes from the curve) several FED governors returned to talk about the fact that a pause in hike cycle is off-table (Daly) and that the true terminal rate could be at least between 5-7% using some adjusted Taylor rules (Bullard);

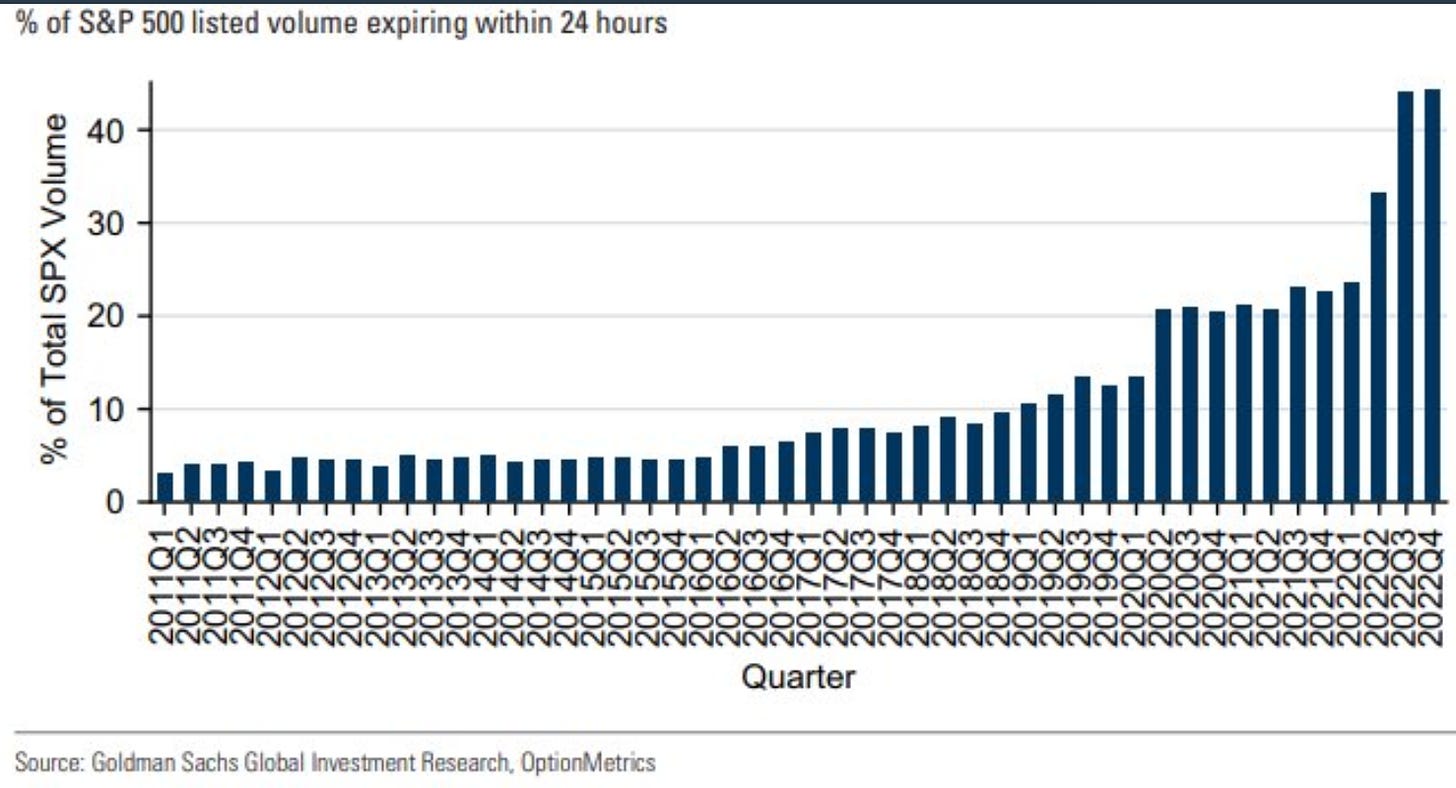

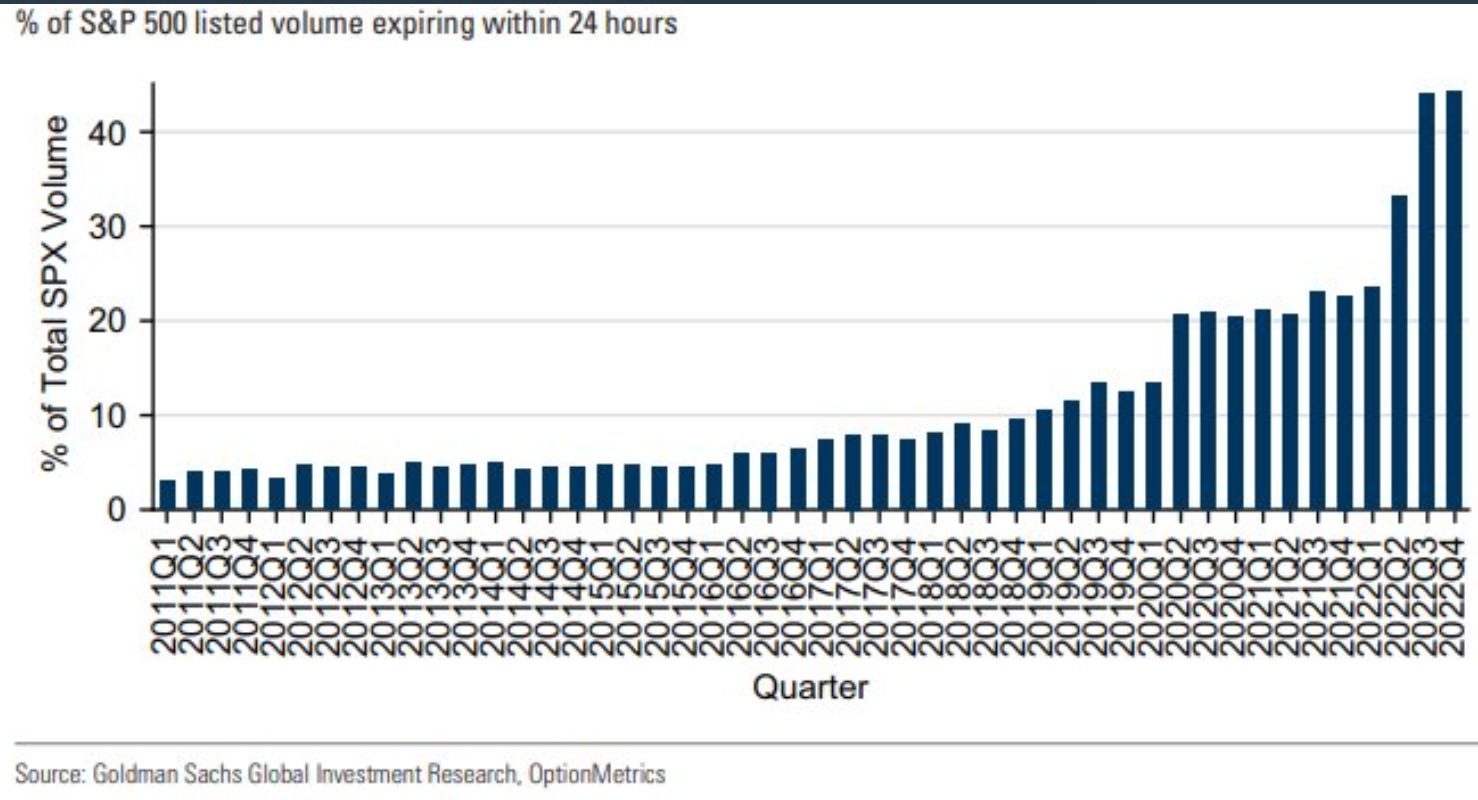

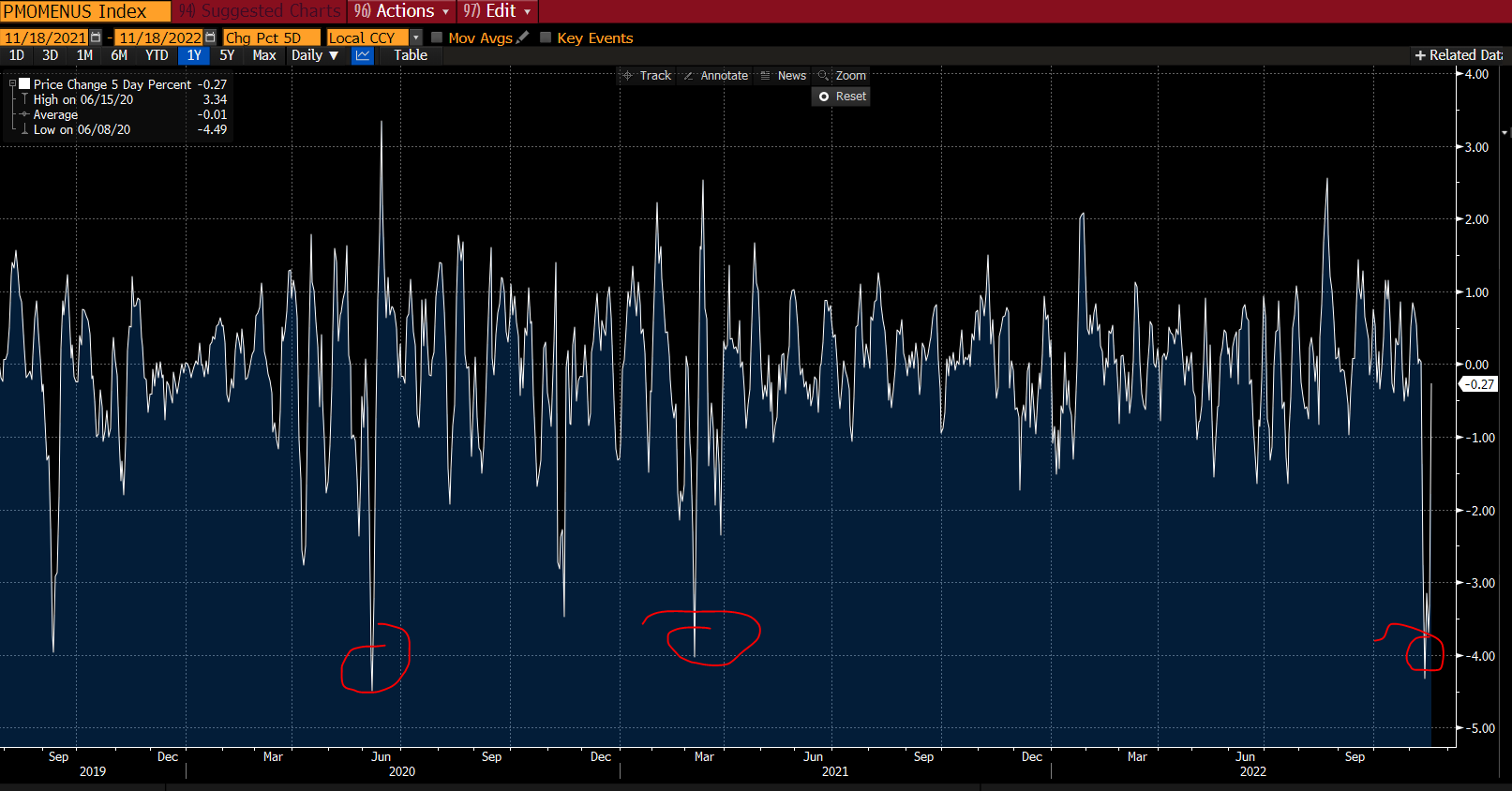

Today is also an OPEX (option expiry day). As showed from the analysis below of @MenthorQpro and given the fact that the share of short term options (also expiring in 24h) is at a record level we could see some volatility as we lose gamma and we are near the zero gamma level on SPX.

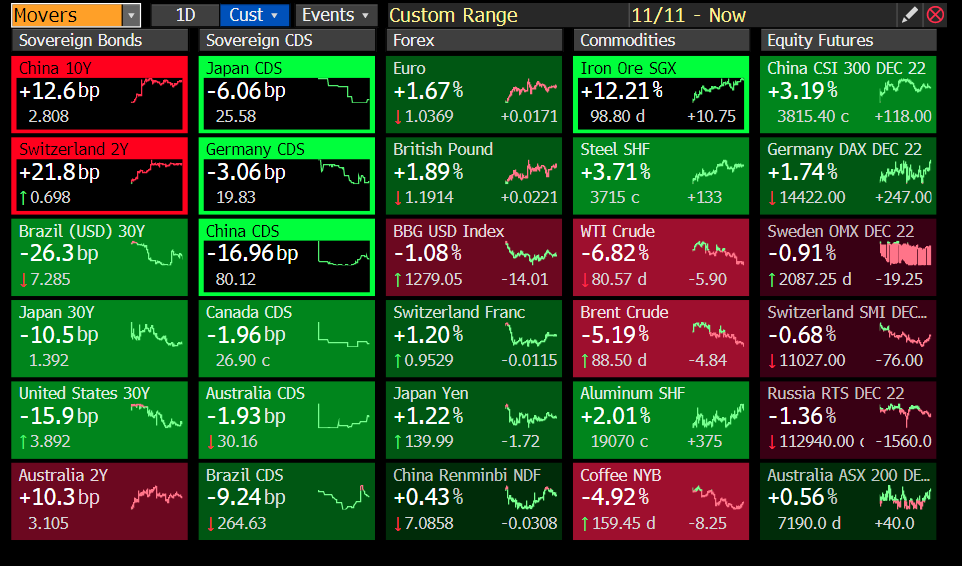

MARKETS: Here the classic “global macro movers” table. It was not a big week for equity in general (SXXP +0.10%, SPX -0.25%) after the strong rebound of last week. China, Germany and Australia continued the strong momentum thanks to positive newflow of reopening from 0-covid policy.

To analyze the price action of this week I’ll return back to this playbook (source bloomberg), basically in 3 acts. We could have passed the peak (at least in USA) in inflation, usually this happens with high rates impacting growth (aka recession). Central banks could reduce the grip temporary, but will arrive the 3th act with a strong return of inflation. We are now in higher inflation regime given the reduction in globalization and the reshoring of profuctions.

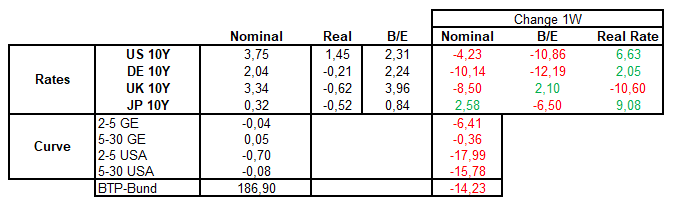

So as always the first reaction is clearly on RATES MARKET with 10y USA at 3.75% and 10y Germany at 2%. After CPI we saw a fall in breakeven (implied inflation) with market removing some rates hike from the curve and a general flattening of the curve (it was a bull flattening).

Below in the US OIS curve (with 1M change) we can see that terminal rate is lower than 5% at the moment (4.90%) but on the long term, after a pause of several months some cuts are priced. Here market is focused on this “pivot vs no pivot” narrative, but the most important thing is how long rates above neutral and what is the impact on real economy.

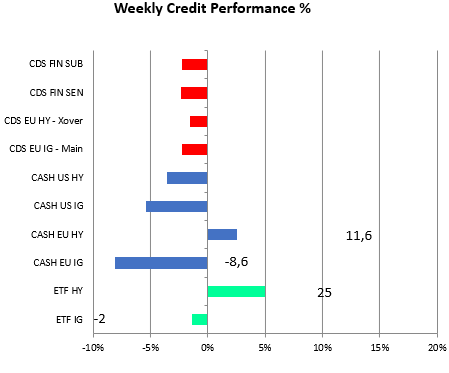

This is visible in CREDIT MARKET were despite an increase in supply of new bonds, IG outperfomed (tightening 8bp) vs HY (widening 11bp). The same is true for ETF. The move in CDS is slightly different but is more technical in nature.

So while market remain focused on central banks and terminal rates (after the last year movement driven by this and by duration) the next stage (2th ACT) could be driven finally by a return of fundamentals (macroeconomic and microeconomics), with the impact of restrictive monetary policy impacting GDP growth, job market and credit sectors. So for the next months I continue to like IG vs HY (with an expected convergence of the the HY/IG ratio total return) near the other cyclical indicators, with a preference for A vs BBB in IG, and of BB vs B/CCC in HY.

EQUITY, as other markets (IG/Govt, HY) or internal of the market indicators (Cyclical vs Defensive, RTY vs SPX) rebounded for almost a month. Bear market rally (this continue to be my hypotesis) could be strong 10/15% at least and driven by short covering. Some confirmation of this (I looked at this in a BBG piece again) is visible looking at “pure momentum”. The Bloomberg index (you find in FTW - factor to watch) is long winners and short loosers but recently lost 4-5% on a weekly basis, an indicator of buyers of loosers (a classical short covering event).

Passing now on FX a move in act 2 (lower inflation due to lower growth) mean that one of the drivers of a strong dollar (1 - rates) loses importance, and with the hopes of China reopening also the second one (2 - relative growth vs row). For this reason DXY (dollar index corrected down) and going forward the trend could continue. To be honest I don’t exclude tactical trading agains this trend (now I am short EURUSD after this spike). The same concept of relative driver apply to COMMODITIES where industrial metal rebounded while oil dived below 90$ due to weak global demand.

MICRO:

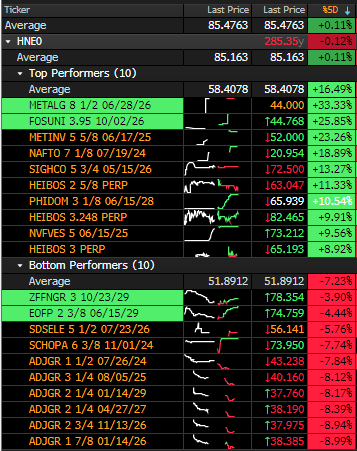

The price action this week is distorted a lot from geopolitical newflow as we have METALG, METINV and NAFTO (3 distressed Ukraine issuers) rebounding strongly following the newsflow on the war, and FOSUNI related to China real estate world after the plan in 16 points announced to boost real estate market (address liquidity of developers and to loose down payment requirements). While:

SIGHCO (Sigma Holdco) jumped on reported stronger earning from passing price increases to customers;

NVFVES (Fives) up on strong Q3 2022 results and encouraging 2023 outlook;

ADJGR (ADLER) on BAFIN spokesman confirming new finding on the company

It’s all for today. I hope you enjoyed my job/analysis. Feel free to forward it to friends/colleague and remember to subscribe to the newsletter.

Also really like your 3 stage analogy on inflation - the double dip is presumably what Powell has nightmares about relating to repeating Burns’ mistake

I never realized cash credit could be so different from ETF perf, why do you think this is?