Weekly Market Review - Oct 28

Weekly Market Review - Oct 28

A thread from macro to micro

Welcome back at the weekly recap, as usual at the end of the week. As always if you like my job/analysis please subscribe below and share it and I remember you that I am also on twitter at @Credit_Junk. And now let’s see what happened this week.

MACRO/NARRATIVE: the narrative of the week is without doubt about central banks starting to pivot or to correctly saying it “market hoping for a pivot”:

after a dovish RBA (Australia Central Bank), Wednesday “Bank of Canada” used a similar approach, tightening only 50bp vs expectation for a 75bp hike;

at the Thursday “ECB meeting” central bank raised rates again 75bp to 1.5% for the deposit rate but the wording sounded more dovish than in the past (“made substantial progress in withdrawing monetary policy accomodation”, removing frontloading words without a specific time frame “to raise interest rates further”) and with a great focus also on growth risk for the eurozone, balancing the hawk focusing only on inflation risks. Some members confirmed that the neutral rate is near 2% so some other increase are needed to go in restrictive territory, but there is no need of an other 75bp (ECB will be data dependent).

The dovish tilt of the ECB was reinforced too by no discussion on QT, delayed at the december meeting, while to reduce distortions on the repo market and the risk-free arbitrage for the banks ECB modified the term of T-LTRO 3 (where banks financed themself at 0%).

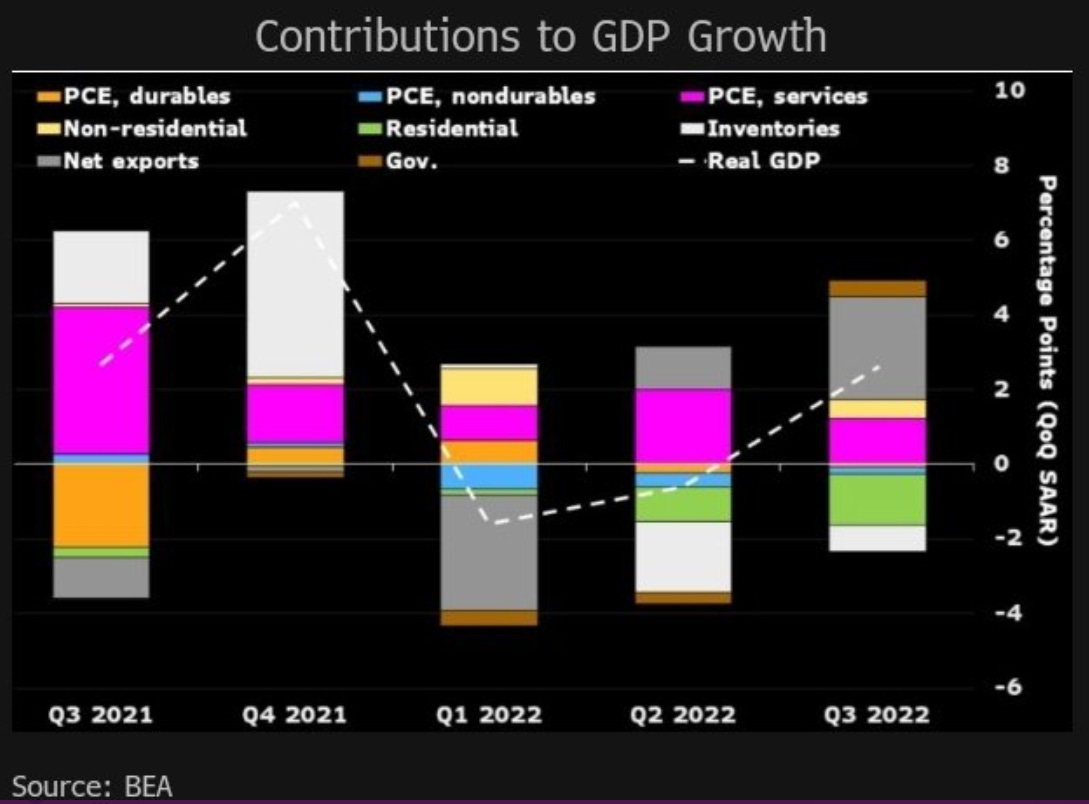

From an economic data release point of view we had 3Q USA GDP (growing 2.6% QoQ after 2 weak quarter) but the breakdown shows the good support only from net export, while personal consumptions services was weaker, impacted by the high level of inflation.

In Europe the “pivotistas” took a cold shower today with the publication of the inflation data for October

France October harmonized CPI rises 7.1% Y/Y; est. +6.5%

Germany October harmonized CPI rises 11,6% Y/Y; est. +10.9%

Italy October harmonized CPI rises 12.,% Y/Y; est. 9.9%

In Italy there was a big impact on energy/gas bills (adjusted from October) while in France energy component increased due to refinery strikes, but the common drivers (food and energy continued to remain high for all countries).

MARKETS:

Given the “pivot” narrative or the “hiking in smaller increments” narrative is no a surprise to see interest rates lower this week with US 10y back near 4%, GER 10y back near 2% and Gilt 10y near 3.5%. Japanese rates remained isolated from all this volatility given the BOJ ultra dovish policy.

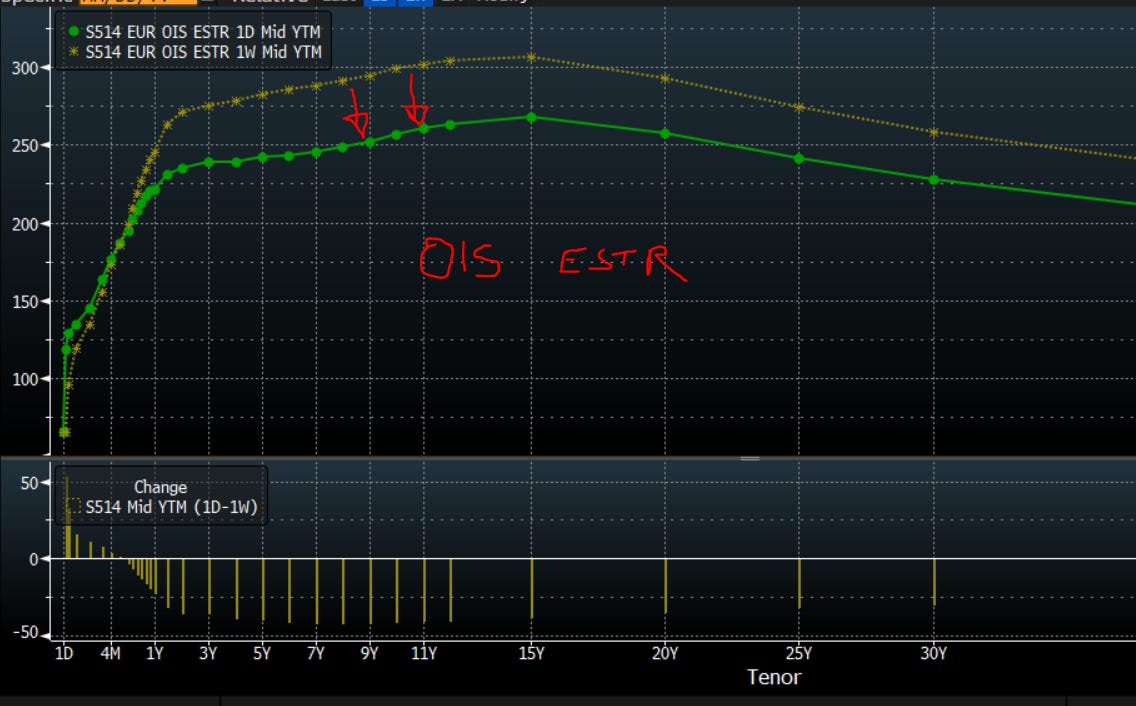

Market repriced the terminal rates lower both in US and EU (below the OIS ESTR pricing implied ECB rates). In Europe the terminal rate passed from 3.25% to 2.70% at mid 2023. Curve, especially in Europe, bull flattened with lower real rates (less hawkish central banks), while breakeven inflation returned to increase for the same reason and for the strong performance of oil and oil products.

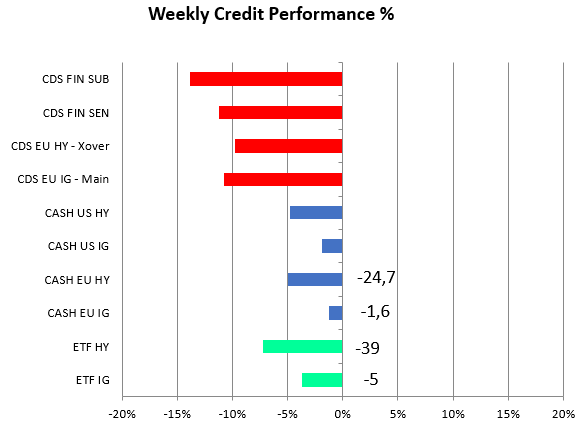

Credit performed well this week with solid tightening in spread term (especially in HY and HY ETF) while CDS index were less impacted by the bad data on inflation and performed better this week.

From an intermarket analysis this week both IG/Govt ratio and HY/IG ratio (both calculated using ETF, confirmed the positive move. It’s not a surprise for risky asset to perform well if interest rates (especially the real rates) are lower.

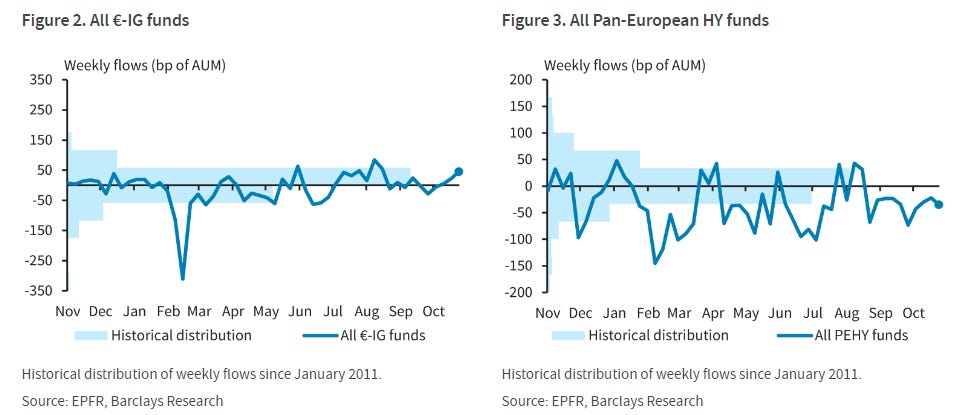

Going forward I continue to skeptical on a pivot of central bank, at the end of the day a reduction in hiking increments (from 75 to 50 and 25bp thereafter) is what was priced yet on ESTR Ois curve in Europe. But valuation on IG could start to be attractive (especially for the interest rate part) while given the economic situation I continue to prefer IG to HY. Flows into mutual funds are supportive for this scenario too (below the continued outflow from HY funds).

On commodities energy futures had a strong week with oil (WTI and Brent) up 3% thanks to strong exports data from USA, but especially strong was the week for gasoline and diesel (up 13% and 16%) where we have a low refinery capacity and low level of inventories for gasoline and distillates (for diesel 25 days of inventories). The risks of shortage are very high!!

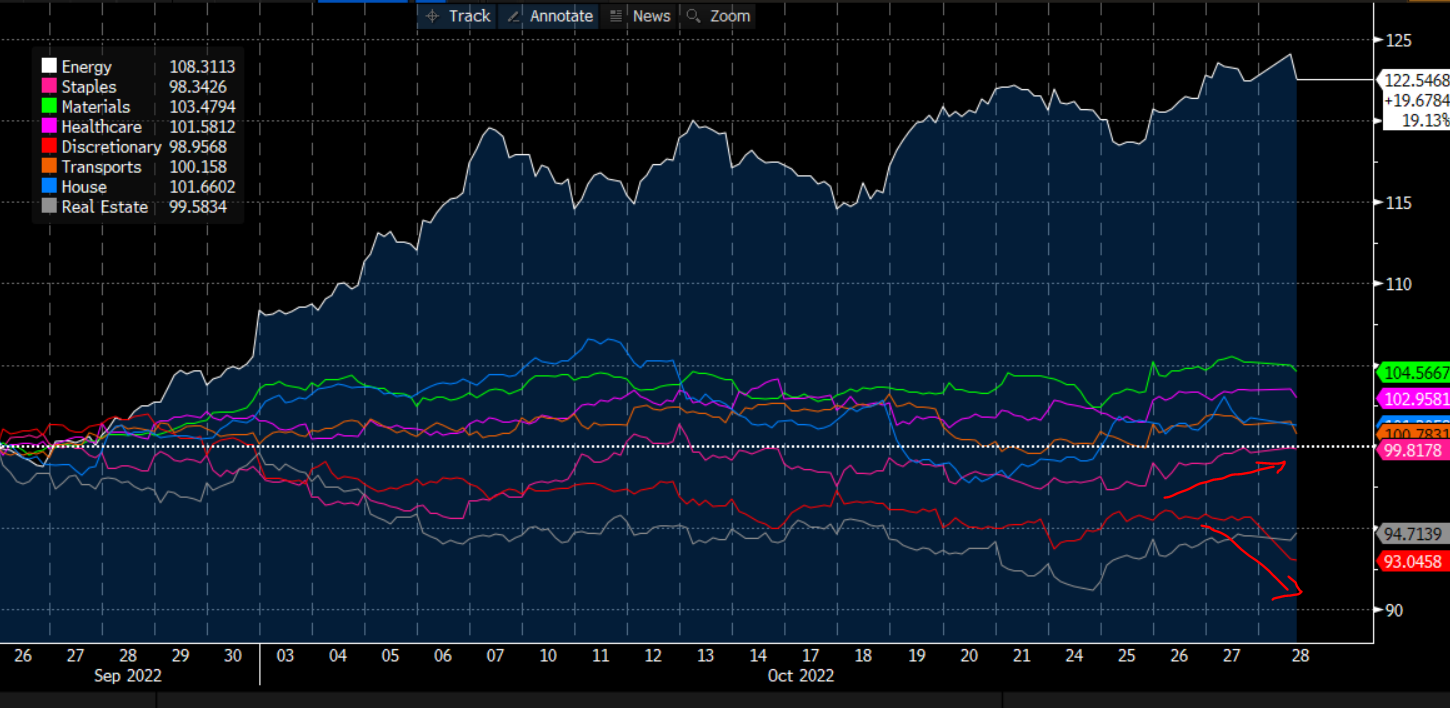

Finally on equity SPX and SXXP are up 2/3% this week. I return to look market internally. We can see in USA an outperformance of energy, while materials (leading together with energy at the beginning of the year are less important now). We can see a recent rebound of staples and healthcare while a strong downtrend on consumers discretionary (an late cycle indicator for market). Real estate rebounded this week thanks to the low level of rates.

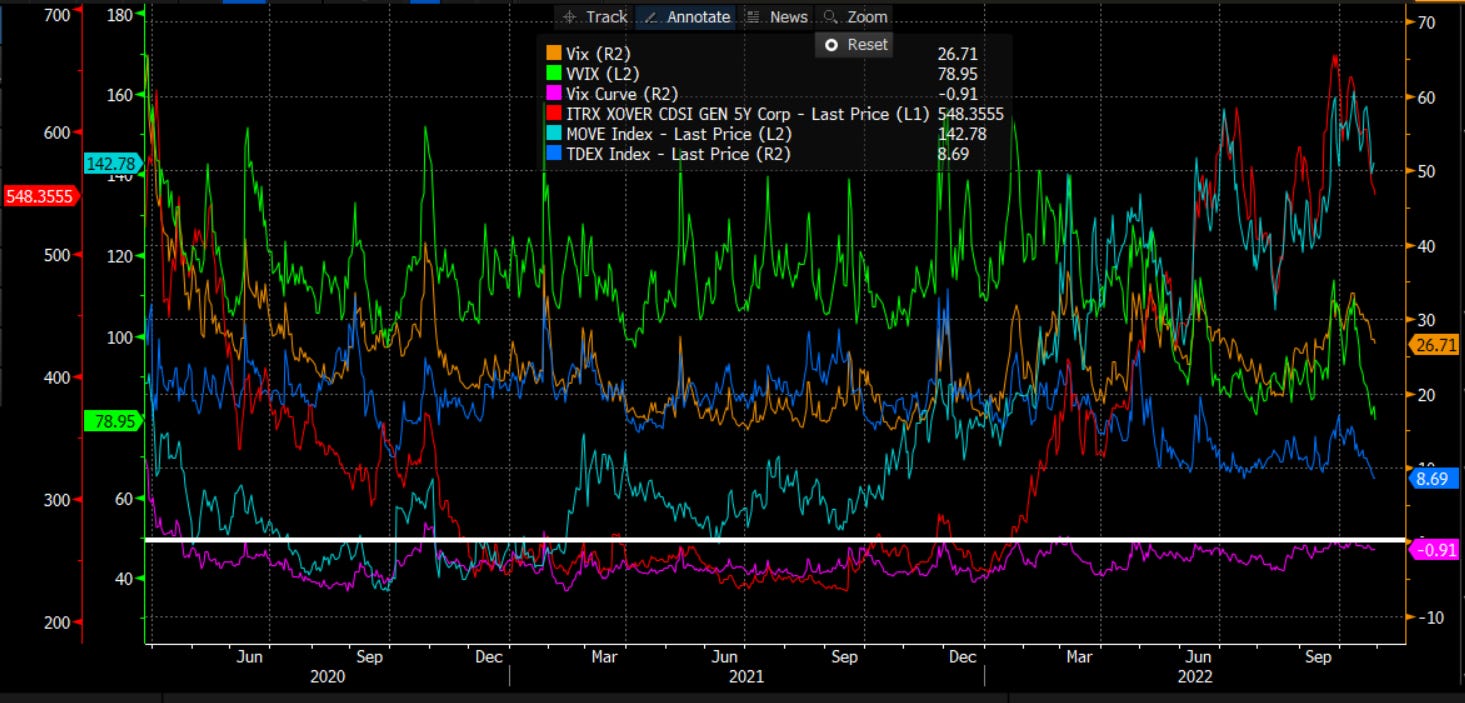

Vola mix chart (where I track volatility for rates, credit and equity) showed MOVE (rates vola) topping, while all indicators of volatility in equity (Vix, Vvix, Vix curve and Tdex) remain quite. Vix falled this week with the rally in equity as usually while sentiment/positioning indicators remain very weak.

I want to conclude this part looking at my market regime chart. I use 2 couples of macro indicators (PMI and CPI, Surprise growth and inflation) both continue to remain in stagflation quadrant. Almost market indicators (rates, equity and oil) returned too there after some volatility in the past weeks. So the path of last resistance is for energy commodities to go up and equity to go down (at least until a true bottom in bonds). On this, narrative (and central banks) started to look at growth risks so I am less confident to take a big outright bet on bonds. Clearly the next step is a shift on deflation. Signals and market are on the edge between these two regimes.

MICRO:

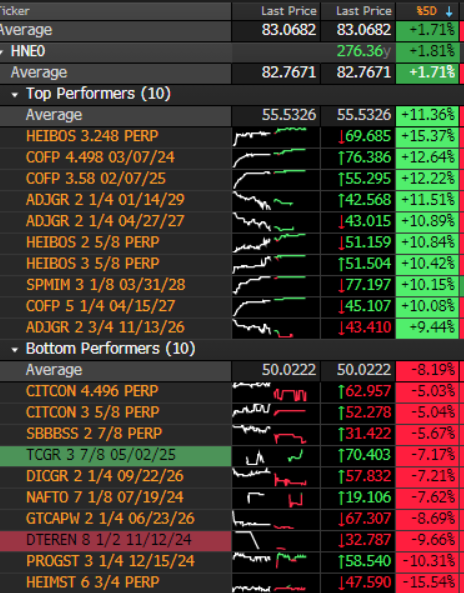

COFP (CASINO): reported 3Q with mixed operating results but decreasing debt. Liquidity remain tight but a tender offer for the 23 bonds and the possibile selling of part of its stake in Assai calmed the market

TCGR moved down to 70 without real news but with some funds looking to reduce exposure

AFFP (Air France) good Q322 (Q321): revenues €8.1bn (+78% vs €4.6bn) and +€503m vs 3Q19, EBITDA €1,677m (vs €794m). Leverage down from 2.2x to 1.6 and strong liquidity.

It’s all for today. I hope you enjoyed my job/analysis. Feel free to forward it to friends/colleague and remember to subscribe to the newsletter.

great take as always, thank you!